There has been a decoupling of expectations within overall financial conditions, with the equity markets surging on the promise of productivity gains while the bond market factors in an increased risk of economic and financial imbalances.

Our RSM US Financial Conditions Index sits at one half of one standard deviation above neutral, which implies that financial conditions remain a modest tailwind for the overall economy.

But there are risks to the outlook, including rising inflation and four economic and financial imbalances that could change the economic trajectory:

- A sustained increase in fiscal deficits.

- The potential of an unsustainable surge in nonresidential investment.

- An overconcentration of technology firms inside equity markets.

- An overconcentration of spending among upper-end households.

Get Joe Brusuelas’s Market Minute commentary every morning. Subscribe now.

In practical terms, these risks are part of what has become the K-shaped economy, where those with higher incomes and greater wealth are benefiting while those at the lower end of the spectrum struggle to make ends meet.

Add in the yet-to-be-determined harm of an energy shock on inflation and household spending and it becomes easier to understand why the current economy is so unloved by those with lower incomes.

On the surface, things seem stable. The economy in the first quarter grew by 2.7% on a yearly basis, with estimates of robust growth continuing into the second quarter.

We expect the economy to grow at a near-trend pace this year of 1.7% with only a 30% probability of a recession over the next 12 months.

Should the current talks between Washington and Tehran prove fruitful, we would expect to raise our forecast for growth this year.

Equity market gains remain robust, driven by a near-record increase in profits while a delayed response by the fixed-income market to the supply shock has resulted in an overall modest level of support for the economy via financial conditions.

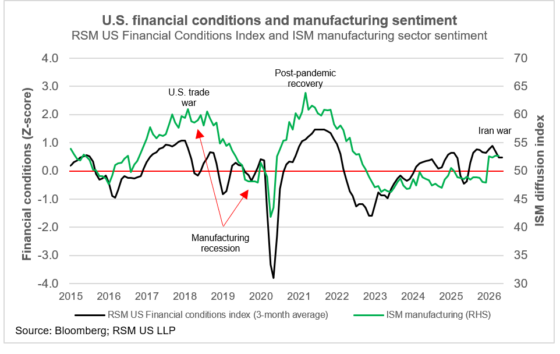

Sentiment vs. risk

There has long been a relationship between business sentiment and the overall level of risk priced into financial assets.

Such a relationship can be seen in the co-movement of the ISM survey of sentiment in the manufacturing sector and our RSM US Financial Conditions Index, which is a composite of risk priced into the equity, bond and money markets.

And this is where the imbalances come into play. Should there be an increase in financial risk—as evidenced in rising Treasury yields— the day-to-day cost of doing business would increase as would the cost of long-term business investment.

Since the start of the war in Iran, 2-year Treasury bond yields have increased by as much as 75 basis points in anticipation of a monetary policy response to inflation while real yields have risen by 82 basis points.

In terms of longer-term investments, 5-year and 10-year Treasury yields have increased by similar amounts before receding, nevertheless increasing the cost of capital.

Indeed one of the more interesting phenomena of recent weeks is that financial conditions remain positive and equity markets continue to float higher even as the cost of capital and the risk of inflation increase.

Still, the stock market has been seemingly impervious to recent externalities of tariffs and an energy shock, moderating the overall increased level of risk in the financial markets.

The takeaway

The direction of growth coupled with a mild financial tailwind will continue to support an extension of the current economic expansion despite the risks outlined here.

While the money markets and the bond markets are more cautious because of inflation pressures, the equity markets are buoyed by prospects of increased productivity coming out of the surge in nonresidential investment.

For now, despite the four imbalances, the flood of cash into the economy because of rising earnings, profits and risk taking in the tech sector is likely to result in sustained growth.