As the European market navigates through a landscape marked by rising energy costs and inflationary pressures, the STOXX Europe 600 Index has shown resilience with a notable increase of 3.92% amid hopes for a swift resolution to Middle East tensions. In this environment, identifying small-cap stocks that are potentially undervalued can be particularly appealing, especially when insider activity suggests confidence in their future prospects.

|

Name |

PE |

PS |

Discount to Fair Value |

Value Rating |

|---|---|---|---|---|

|

CellaVision |

23.8x |

4.8x |

41.58% |

★★★★★☆ |

|

Eurocell |

11.9x |

0.3x |

44.92% |

★★★★★☆ |

|

A.G. BARR |

15.4x |

1.7x |

48.57% |

★★★★★☆ |

|

Lemonsoft Oyj |

19.2x |

3.0x |

44.04% |

★★★★★☆ |

|

everplay group |

7.0x |

2.2x |

7.69% |

★★★★★☆ |

|

Embracer Group |

2.8x |

0.6x |

35.23% |

★★★★★☆ |

|

Bilia |

15.2x |

0.3x |

19.39% |

★★★★☆☆ |

|

Morgan Advanced Materials |

NA |

0.6x |

41.43% |

★★★★☆☆ |

|

ABL Group |

NA |

0.4x |

-41.33% |

★★★☆☆☆ |

|

Young’s Brewery |

44.0x |

1.0x |

35.77% |

★★★☆☆☆ |

Let’s uncover some gems from our specialized screener.

Simply Wall St Value Rating: ★★★★★☆

Overview: A.G. BARR is a UK-based company primarily engaged in the production and distribution of soft drinks, with additional operations in cocktail solutions and other segments, holding a market cap of approximately £0.55 billion.

Operations: A.G. BARR generates significant revenue from its Soft Drinks segment, contributing £382 million, and also earns from Cocktail Solutions with £35.8 million. The company’s gross profit margin has shown fluctuations, reaching 40.54% in the latest period reported.

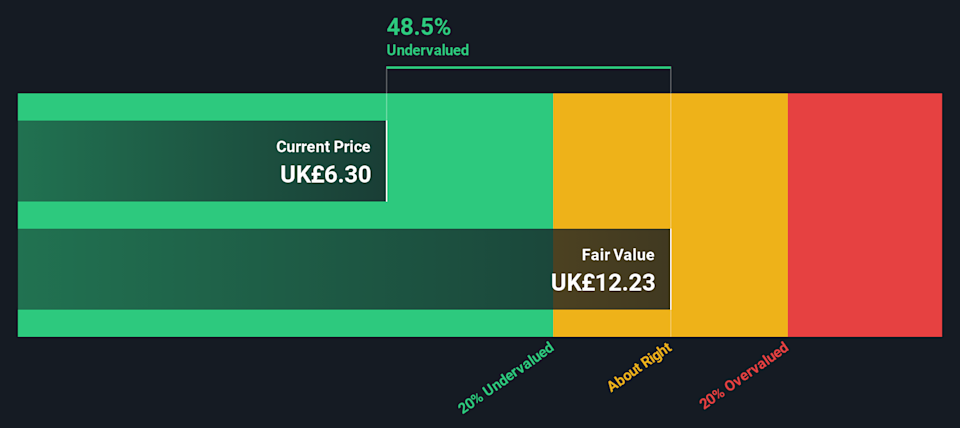

PE: 15.4x

A.G. BARR, a notable player in the European market, recently reported sales of £437.3 million for the year ending January 2026, up from £420.4 million the previous year, reflecting solid growth potential. Despite relying on external borrowing for funding, insider confidence is evident with recent share purchases indicating optimism about future prospects. The company has increased its dividend to 18.71p per share and launched a rebranded IRN-BRU ‘ZERO’, aiming to capture growing low-calorie beverage demand across the UK.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Genuit Group specializes in providing water management, climate management, and sustainable building solutions, with a market cap of approximately £1.02 billion.

Operations: Genuit Group’s revenue is primarily derived from its three main segments: Water Management Solutions, Climate Management Solutions, and Sustainable Building Solutions. The company has experienced fluctuations in its gross profit margin, reaching 44.48% in the latter part of 2024. Operating expenses include significant allocations to sales and marketing as well as general and administrative functions.