Discovering Hidden Opportunities in Middle Eastern Stocks

Uncategorized

Discovering Hidden Opportunities in Middle Eastern Stocks

08 mins

The Middle Eastern stock markets have recently experienced a rally, driven by the U.S.-Iran ceasefire agreement, which has eased regional tensions and led to significant gains in Gulf equities. As investors navigate these dynamic conditions, identifying stocks with strong fundamentals and growth potential becomes crucial for uncovering hidden opportunities in this evolving landscape.

Name

Debt To Equity

Revenue Growth

Earnings Growth

Health Rating

Analyst I.M.S. Investment Management Services

NA

33.12%

45.12%

★★★★★★

C. Mer Industries

70.13%

13.00%

68.68%

★★★★★★

Payton Industries

NA

1.92%

13.55%

★★★★★★

Terminal X Online

10.00%

13.43%

45.34%

★★★★★★

Saudi Azm for Communication and Information Technology

Let’s dive into some prime choices out of from the screener.

Simply Wall St Value Rating: ★★★★★☆

Overview: Amanat Holdings PJSC is an investment company focused on the education and healthcare sectors in the United Arab Emirates and internationally, with a market capitalization of AED3.28 billion.

Operations: Amanat Holdings PJSC generates revenue primarily from its investments in the education sector, contributing AED528 million, and the healthcare sector, adding AED404 million.

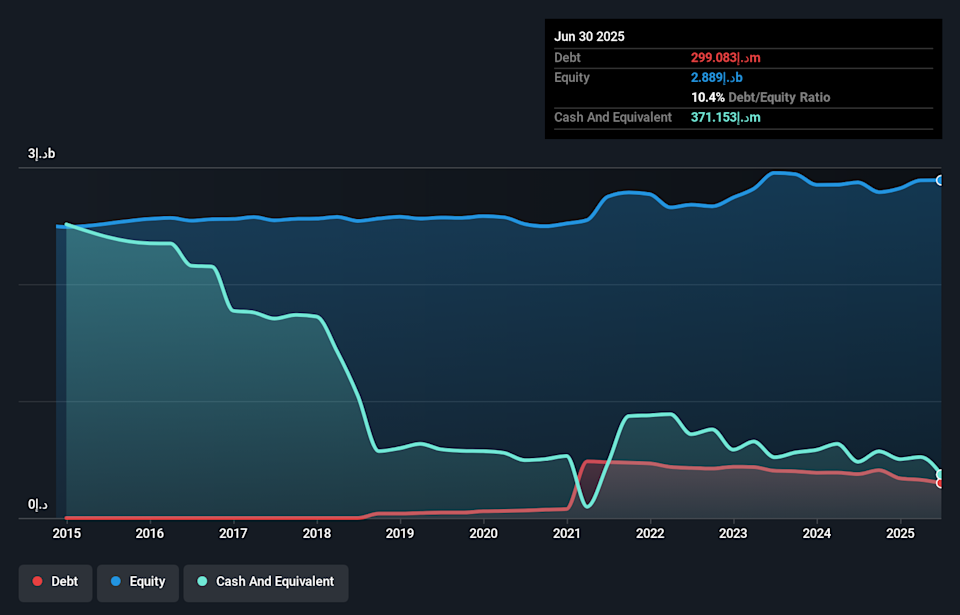

Amanat Holdings, a smaller player in the Middle East market, has shown impressive performance with earnings growing 48.4% last year, outpacing the industry average of 12.8%. Despite a debt-to-equity ratio increase from 3% to 9.7% over five years, its financial health remains robust as it holds more cash than total debt and covers interest payments comfortably. The company reported AED176.99 million net income for 2025, up from AED115.84 million previously; however, this was partly due to a non-recurring gain of AED68.3 million impacting results. With revenue expected to grow by 15.74% annually despite forecasted earnings decline, Amanat continues to offer intriguing prospects in its sector.

DFM:AMANAT Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: Union Properties Public Joint Stock Company is involved in property investment and development, with a market capitalization of AED3.31 billion.

Operations: The company’s primary revenue streams include Goods and Services, contributing AED491.13 million, followed by Housekeeping at AED95.61 million. Contracting and Real Estate generate AED69.12 million and AED81.02 million, respectively.

Union Properties, a notable player in the Middle East’s commercial services sector, has shown impressive financial strides with earnings growth of 67.8% over the past year, outpacing industry averages. Their debt-to-equity ratio dropped significantly from 57.2% to 8.9% over five years, highlighting improved financial health. Despite a large one-off gain of AED574 million impacting recent results, their price-to-earnings ratio at 7.2x remains attractive compared to the regional market average of 10.7x. With revenue forecasted to grow by 39%, Union Properties seems poised for continued expansion while maintaining profitability without cash runway concerns.

DFM:UPP Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: Dogu Aras Enerji Yatirimlari AS operates in Turkey, focusing on the retail sale and distribution of electricity through its subsidiaries, with a market capitalization of TRY25.42 billion.

Operations: Dogu Aras Enerji Yatirimlari AS generates revenue primarily from electricity distribution and retail electricity sales, with TRY18.02 billion and TRY19.17 billion respectively. The company does not include “Other”, “Unallocated” or “Inter-Segment” amounts in its financials.

Dogu Aras Enerji Yatirimlari, a notable player in the electric utilities sector, has demonstrated impressive financial resilience. With earnings surging by 979% over the past year, it outpaced industry growth of 1.9%. The company’s net debt to equity ratio stands at a satisfactory 11.2%, indicating strong financial health. Interest payments are well covered with EBIT coverage at 9.4 times, showcasing robust operational efficiency. Despite sales dipping to TRY 32.72 billion from TRY 52.22 billion last year, net income rose significantly to TRY 2.24 billion from TRY 207 million, reflecting high-quality earnings and potential for future growth in this dynamic market landscape.

IBSE:ARASE Earnings and Revenue Growth as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include DFM:AMANAT DFM:UPP and IBSE:ARASE.