Key Points

-

Serve Robotics is a leading developer of last-mile delivery robots, which could replace human-driven solutions because of their cost efficiency.

-

Serve has deployed 2,000 of its latest Gen 3 robots into the Uber Eats and DoorDash food delivery networks so far.

-

Serve stock isn’t cheap right now, but the company has enormous potential.

- 10 stocks we like better than Serve Robotics ›

Serve Robotics (NASDAQ: SERV) believes existing last-mile logistics solutions are inefficient because they rely on humans and cars to deliver relatively small orders from restaurants and retailers. The company says robots and drones are better suited for these tasks because they are significantly more cost-effective and more scalable.

Serve predicts the shift from humans to robots in the last-mile logistics industry will create a $450 billion opportunity by 2030. Thousands of the company’s latest Gen 3 autonomous robots are already making deliveries through Uber‘s Uber Eats network and also through DoorDash, which has created a pathway to widespread adoption.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Serve stock is down 7% in 2026 as investors reconsider its sky-high valuation, especially amid volatility in the broader market. But could this be a great long-term buying opportunity?

Image source: Getty Images.

Driving the shift from humans to robots

Serve’s Gen 3 robots are powered by Nvidia‘s Jetson Orin platform, which includes all of the hardware and software necessary to achieve Level 4 autonomy. This means the robots can safely drive on sidewalks in designated areas with no human intervention.

Over the last 12 months, Serve’s fleet has grown from 100 robots to 2,000 robots, allowing the company to provide its service in over 110 neighborhoods across 20 major American cities. It will expand to more U.S. markets during 2026, but it plans to go global in 2027 by entering cities in Japan, Spain, Taiwan, and the United Kingdom.

Serve believes it can eventually achieve an average delivery cost of under $1 as the Gen 3 fleet expands, a substantial reduction from the cost of human-driven deliveries, which typically range from $8 to $10. Plus, the cost of human labor will only rise, making robotic solutions even more attractive over time.

In January, Serve also announced the acquisition of Diligent, which will facilitate its expansion into a new vertical. Diligent developed a robot called Moxi, which operates exclusively in hospitals and uses the same Nvidia-powered technology as Serve’s Gen 3 robots. Moxi transports supplies, medications, and lab samples, giving nurses and other staff more time to assist patients.

Serve is forecasting a massive revenue increase in 2026

Serve generated a record $2.65 million in revenue in 2025, a 46% increase from 2024. However, the company only deployed its 2,000th robot in mid-December, so it didn’t get the benefit of operating its entire fleet for the whole year.

With a full fleet now in service, Serve believes its revenue could grow almost tenfold to $26 million during 2026.

But scaling a robotics business is very expensive. Serve had over $97 million in operating costs in 2025, and given its minimal revenue, this contributed to a generally accepted accounting principles (GAAP) net loss of $101 million. That loss more than doubled compared to 2024, and even if the company’s revenue jumps tenfold in 2026, it will likely lose a substantial amount of money again unless it dramatically slashes costs.

Serve ended 2025 with $260 million in cash and marketable securities on its balance sheet, so it can afford to lose money at the current pace for now. However, if it doesn’t chart a path to profitability in the next couple of years, it might have to raise more money by issuing new shares, which will dilute the holdings of existing investors.

Serve stock looks expensive, despite the recent dip

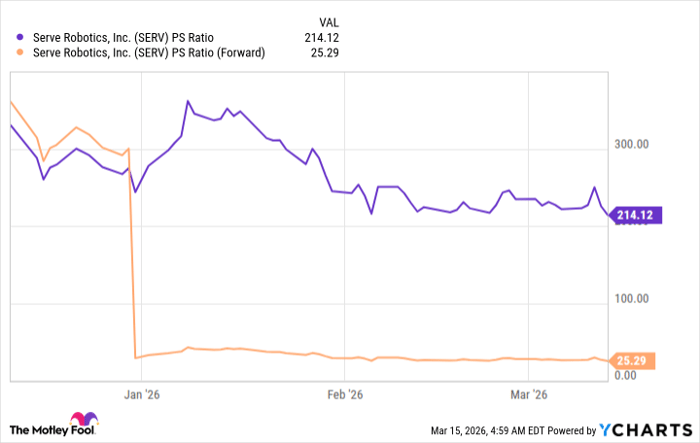

Serve stock is trading at a sky-high price-to-sales (P/S) ratio of 214 as I write this, so it certainly isn’t cheap. For some perspective, Nvidia stock trades at a P/S ratio of just 20, and even Palantir Technologies, which I believe is expensive in its own right, trades at a much lower P/S ratio of 86.

But if we assume Serve will deliver $26 million in revenue during 2026 as management expects, then its forward P/S ratio is 25, which looks far more reasonable.

SERV PS Ratio data by YCharts

Given that Serve stock would still be trading at a premium to Nvidia, which is arguably the world’s highest-quality artificial intelligence (AI) company, there might not be much room for upside in 2026. That means investors probably need to take a longer-term view to maximize their chances of earning a positive return.

If the market for robotic last-mile delivery really does reach $450 billion by 2030 as Serve predicts, the company’s revenue would have significant room to grow from here. Therefore, when investors reflect back on this moment in four or five years, Serve’s current stock price might actually look extremely attractive.

In summary, investors who are looking for strong gains in the next few months should probably steer clear of Serve stock, but there is certainly potential for upside in the longer run.

Should you buy stock in Serve Robotics right now?

Before you buy stock in Serve Robotics, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Serve Robotics wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $508,877!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,115,328!*

Now, it’s worth noting Stock Advisor’s total average return is 936% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of March 18, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends DoorDash, Nvidia, Palantir Technologies, Serve Robotics, and Uber Technologies. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.