Tech investors and Wall Street are waiting for Taiwan Semiconductor or TSMC to kick-start the busy part of the second quarter earnings season when it reports on Thursday, July 16.

The AI chip manufacturing powerhouse will provide Wall Street with critical insights into what’s next on the artificial intelligence front.

TSMC might have to provide robust guidance to reassure investors that the AI hyperscalers’ capex spending spree remains in full force after Meta said recently that it would begin selling excess AI computing power to customers.

Where the Stock Market Sits Heading into Q2 Earnings Season

The stock market has cooled down heading into the unofficial start of Q2 earnings on Tuesday, July 14, when JPMorgan and other big Wall Street banks report.

The Nasdaq is trading roughly where it was two months ago after pulling back from its early June highs. The bulls are fighting to hold their ground at the tech-heavy index’s 50-day moving average and its early May breakout levels. They did just that on Thursday, sending the Nasdaq 1.3% higher to overtake its 50-day again.

Image Source: Zacks Investment Research

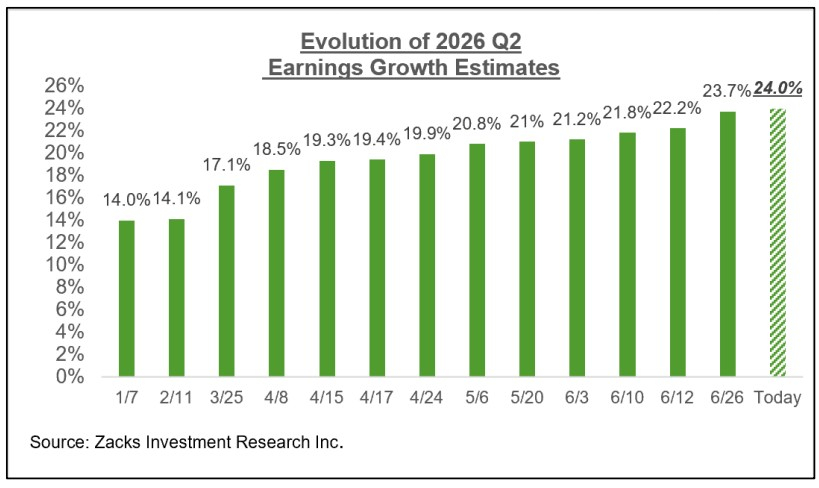

The bulls are banking on another impressive earnings season from big tech and beyond. Total S&P 500 earnings are projected to grow by 24% YoY based on the most recent Zacks data—up from 14% in early January and 21.2% in early June.

On the technology front, total tech sector earnings are expected to grow 48.5% in Q2 on 28.0% higher revenues. Taiwan Semiconductor’s report on July 16 will provide Wall Street essential insights into what to expect from AI companies, including Nvidia, and the entire tech sector in the second half.

Image Source: Zacks Investment Research

Is TSMC the Best Long-Term Buy and Hold Stock on Wall Street?

Semiconductors are arguably the most complex and critical technologies that humans have ever created. Chips are the lifeblood of the entire technology-driven economy and the foundation of the AI age. This is why Nvidia, Micron, and tons of other semiconductor stocks have skyrocketed over the past five years and in the first half of 2026.

The all-important role that semiconductors play in tech and the economy is why investors must consider buying the company that physically builds and manufactures almost all of the cutting-edge semiconductors for Nvidia and nearly every other firm competing to win the AI arms race.

Taiwan Semiconductor Manufacturing Company TSM is perhaps the most important technology company in the world, building and manufacturing semiconductors used for AI innovations and much more. (Note: Taiwan Semi or TSMC trades under the ticker TSM in the U.S.)

Image Source: Zacks Investment Research

TSMC reportedly captures 60% of the entire global chip foundry market and 90% of advanced semiconductor manufacturing. Taiwan Semi has spent decades carving out what’s now a nearly impenetrable moat around its leading-edge chip-building business.

Nvidia NVDA relies on TSMC to manufacture its most sophisticated AI chips, as do other tech titans and Mag 7 companies. TSMC said it “served 534 customers and manufactured 12,682 products for various applications” in 2025.

TSMC was founded in 1987 on a simple but revolutionary idea dubbed the “pure-play foundry” model. The tech company decided it would focus exclusively on manufacturing advanced semiconductors for other companies, never aiming to design or sell its own branded products.

This founding principle helped Taiwan Semi build trust with customers like Apple, Nvidia, AMD, and Qualcomm. Apple AAPL, Nvidia and others rely on TSMC because of its expertise. On top of that, NVDA executives and others can sleep easy at night knowing that Taiwan Semi won’t compete against them.

As a result, TSMC attracted huge orders, invested heavily in cutting-edge technologies, growing into the world’s most dominant chip manufacturer through unmatched scale and expertise.

Image Source: Zacks Investment Research

It’s not hyperbolic to say that AI and technology growth and innovation would grind to a halt without TSMC. This is exactly why Taiwan Semi is addressing one of its only potential shortfalls: geopolitical fears by expanding its manufacturing footprint outside of Taiwan into the U.S., Japan, and elsewhere.

The company is actively building fabs in the U.S. Yet, in a sign of just how important and cutting-edge TSMC is, the Taiwan-based firm had to bring thousands of employees from the small island to the Arizona desert to help build the complex manufacturing plants.

The Chip Builder’s AI-Boosted Growth Outlook

Taiwan Semi is ramping up its industry-leading 3-nanometer production to support the AI arms race. So-called advanced technologies made up 74% of its total wafer revenue in Q1 FY26, with 3-nanometer chips accounting for 25% of TSMC’s quarterly wafer sales.

The leading chip builder said earlier this year that it expects to grow its revenue by 30% in 2026 as part of a compound annual growth rate (CAGR) of ~25% between 2024 and 2029.

Image Source: Zacks Investment Research

Taiwan Semi is projected to grow its revenue by 32% in FY26 and 27% next year to reach $205 billion in FY27, doubling its 2024 sales ($88 billion), based on Zacks estimates.

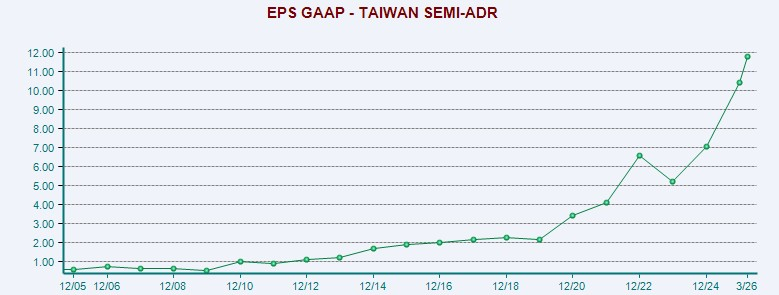

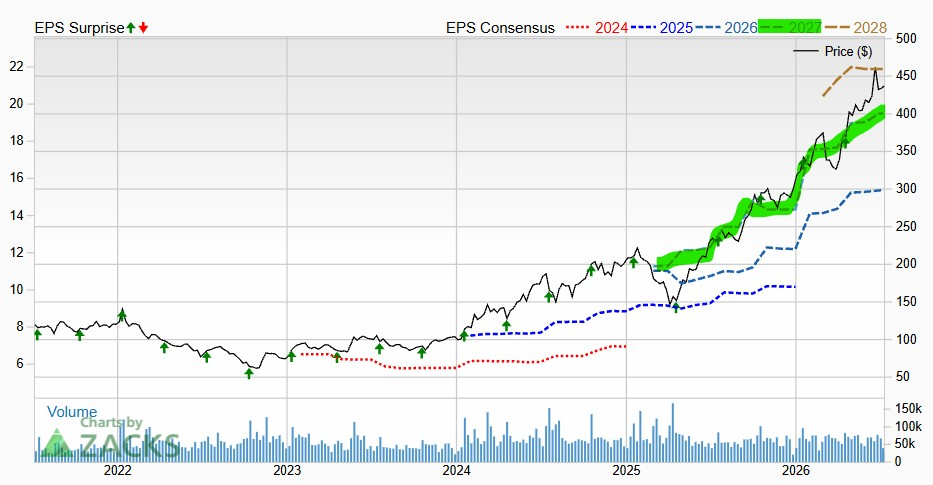

TSMC is projected to grow its adjusted EPS by 45% in 2026 and 27% in 2027, based on the most recent Zacks estimates. This growth outlook would see the firm post earnings of $19.50 per share next year, nearly quadrupling 2023’s EPS. TSMC’s upward earnings revisions earn it a Zacks Rank #2 (Buy), and it’s beaten our quarterly estimate for five years running.

Image Source: Zacks Investment Research

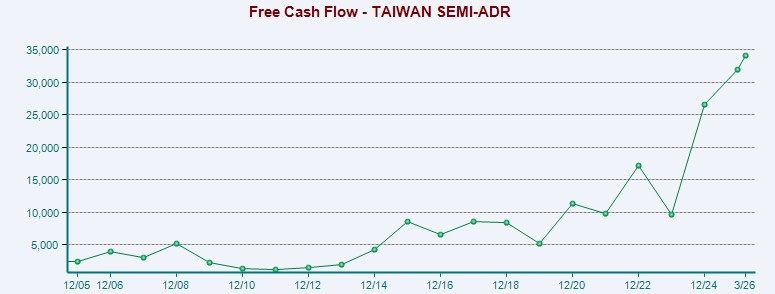

Taiwan’s balance sheet is robust, with more cash and equivalents ($109 billion) than total liabilities ($86 billion). It is also churning out impressive free cash flow growth over the last several years. Its strong financial position helped TSM feel comfortable raising its 2026 capex guidance to $52-$56 billion, blowing away 2025’s $40.9 billion.

Buy TSMC Now, Or Wait for a Pullback?

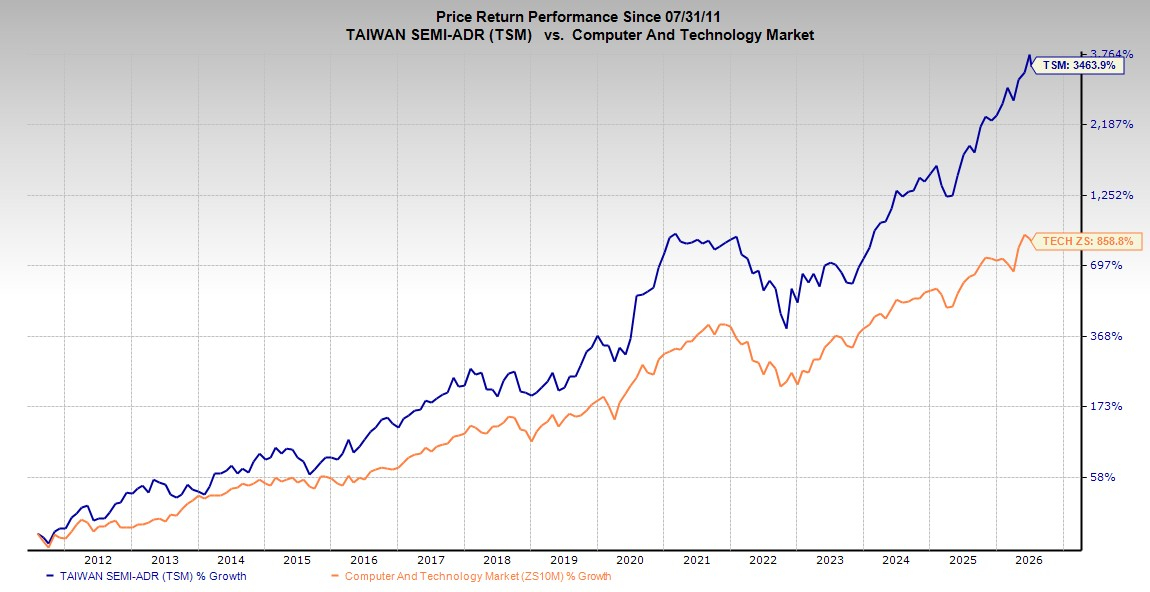

The dividend-paying chip maker stock has soared ~5,000% in the past 20 years vs. Tech’s ~1,100%. TSM has ripped 340% higher in the past three years, including its Nvidia-crushing 90% charge in the trailing 12 months to trade near its recent highs.

Image Source: Zacks Investment Research

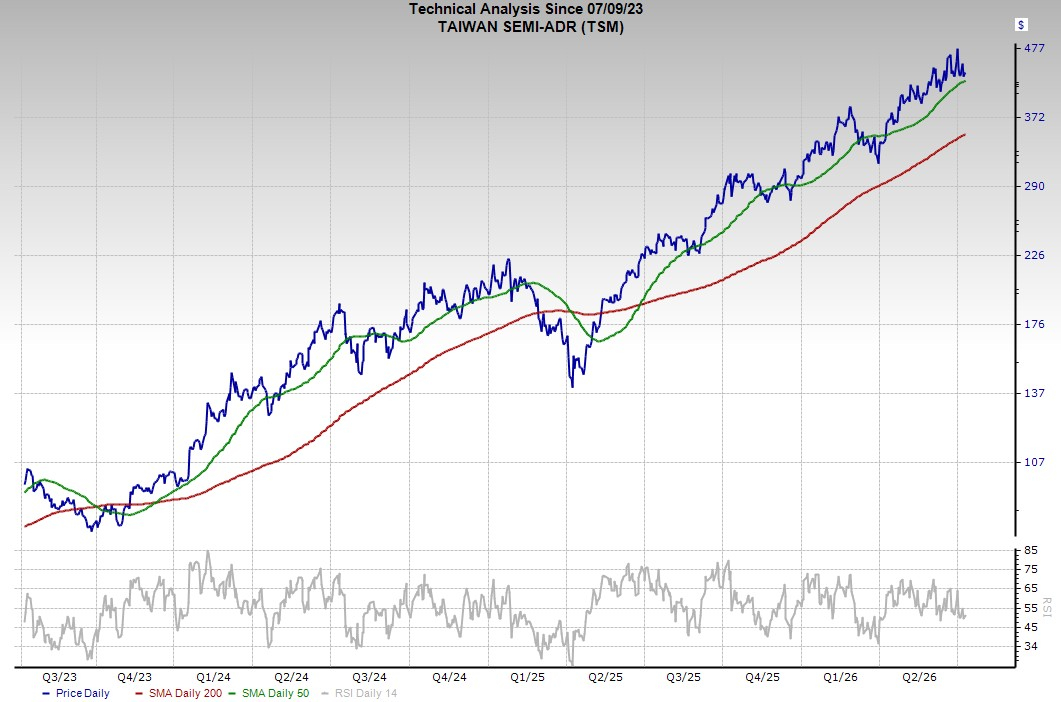

TSM is attempting to hold ground at its 50-day moving average heading into its Q2 earnings release. Some investors might want to buy the stock now before earnings in preparation for a possible breakout. Others might want to see if Taiwan Semi finally faces some healthy selling after its massive rally.

The stock market timing game is exceedingly difficult, meaning that most long-term investors should start a position in TSMC now and then add to it the next time it falls—which will happen at some point, there’s just no telling when. The stock hasn’t tested its 200-day moving average in over a year and it trades well above its 50-week.

Image Source: Zacks Investment Research

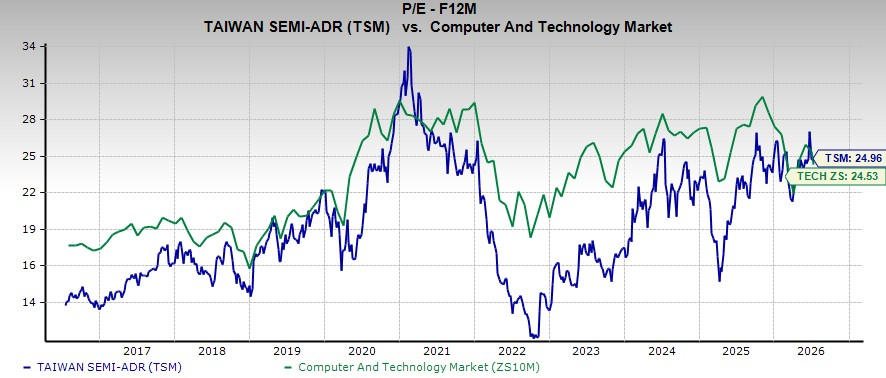

On the valuation front, Taiwan Semi trades in line with the Tech sector despite its outperformance. It also trades at a 27% discount to its 10-year highs at 24.9X forward earnings, which is far from a bubbly valuation.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Apple Inc. (AAPL) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.