Despite the Fed’s hawkish stance, disappointing US labor market data released earlier this month dampened market expectations regarding the extent of the Fed’s policy tightening. In June, the nonfarm payrolls report showed an increase of only 57,000 jobs, falling well short of the projected 110,000. This sharp slowdown in hiring confirmed the overall, controlled cooling of the US economy. Market participants are now awaiting new signals to better understand the Fed’s intentions regarding changes to its monetary policy. These signals are on the way: US consumer and producer price indices are expected to be released during the upcoming trading week of July 13–July 19, 2026.

Market participants will also focus on the release of other key US macroeconomic data and important macroeconomic statistics from China, as well as the outcome of the Bank of Canada’s meeting.

Note: During the coming week, new events may be added to the calendar, and/or some scheduled events may be canceled. GMT time.

The article covers the following subjects:

Major Takeaways

- Monday: None scheduled.

- Tuesday: US CPI.

- Wednesday: Key macroeconomic data from China, including Q2 GDP, the US PPI, and the Bank of Canada’s interest rate decision.

- Thursday: US retail sales.

- Friday: UoM Consumer Sentiment Index (Preliminary).

- Key event of the week: US CPI and PPI.

Monday, July 13

There are no important macroeconomic statistics scheduled for release.

Tuesday, July 14

12:30 – USD: US Consumer Price Index

The Consumer Price Index (CPI) measures the change in prices of a selected basket of goods and services over a given period. It is a key indicator for assessing inflation trends and changes in consumer preferences. Food and energy are excluded from the Core CPI to provide a more accurate assessment.

A high index reading typically strengthens the US dollar by signaling an increased likelihood of the Fed interest rate hike, while a low reading generally weakens the currency.

Previous values YoY:

- CPI: +4.2%, +3.8%, +3.3%, +2.4% in February and January 2026, +2.7% in December 2025, +2.7%, +3.0%, +2.9%, +2.7%, +2.7%, +2.4%, +2.3%, +2.4%, +2.8%, +3.0% in January 2025, +2.9%, +2.7%, +2.6%, +2.4%, +2.5%, +2.9%, +3.0%, +3.3%, +3.4%, +3.5%, +3.2%, +3.1%, +3.4%, +3.1%, +3.2%, +3.7%, +3.7%, +3.2%, +3.0%, +4.0%, +4.9%, +5.0%, +6.0%, +6.4% in January 2023;

- Core CPI: +2.9%, +2.8%, +2.6%, +2.5% in February and January 2026, +2.6% in December 2025, +2.6%, +3.0%, +3.1%, +3.1%, +2.9%, +2.8%, +2.8%, +2.8%, +3.1%, +3.3% in January 2025, +3.2%, +3.3%, +3.3%, +3.3%, +3.2%, +3.2%, +3.3%, +3.4%, +3.6%, +3.8%, +3.8%, +3.9%, +3.9%, +4.0%, +4.0%, +4.1%, +4.3%, +4.7%, +4.8%, +5.3%, +5.5%, +5.6%, +5.5%, +5.6% in January 2023.

The figures indicate renewed inflationary pressure, which economists attribute primarily to rising energy prices amid the unrest in the Middle East and around the Strait of Hormuz. Although inflation is significantly lower than it was in 2022, when annual inflation hit a 40-year high of 9.1% in June, it remains a concern for the Fed’s leadership, whose top priorities include keeping inflation below the 2.0% target while promoting economic growth and labor market stability.

US inflation remains well above the Fed’s 2% target, forcing the central bank to keep interest rates high or take a pause to assess the economic and labor market situation if the reduction occurs.

If the data points to a decline in inflation or comes in weaker than expected, the dollar will most likely decline temporarily. If the numbers surpass expectations and previous readings, the greenback will strengthen, as this scenario would heighten the chances that the Fed will keep interest rates elevated for longer or resume its cycle of monetary policy tightening.

Wednesday, July 15

02:00 – CNY: Industrial Production. Retail Sales. Q2 GDP.

The National Bureau of Statistics of China’s report on industrial production shows the output of Chinese industrial enterprises, such as factories and manufacturing facilities. An increase in industrial production is a positive factor for the yuan, indirectly signaling the possibility of accelerating inflation, which may force the People’s Bank of China to tighten monetary policy.

Conversely, the decline in the indicator value may negatively impact the yuan.

Previous values YoY: +4.5%, +6.3%, +6.5%, +5.2%, +5.7%, +6.8%, 5.8%, +6.1%, +7.7%, +5.9%, +6.2% in December 2024.

The retail sales index, published monthly by the National Bureau of Statistics of China, gauges the change in the aggregate value of sales at the retail level across the country. The index is often viewed as an indicator of consumer confidence and economic prosperity and reflects the state of the retail sector in the near term. An increase in the index value is usually positive for the yuan, while a decrease in the index value will affect it negatively. Previous YoY values: -0.6%, +2.8%, +0.9%, +1.3%, +2.9%, +3.0%, +3.4%, +3.7%, +4.8%, +6.4%, +5.1%, +5.9%, +4.0%, +3.7% in December 2024.

The data indicate that this sector of the Chinese economy continues to recover after a strong decline in February and March 2020. If the data prove weaker than the forecasted or previous values, the yuan may experience a decline, potentially a sharp one.

China is a major buyer of commodities and a supplier of a wide range of finished goods to the global commodity market. Since China’s economy is the second largest in the world, the release of its significant macroeconomic indicators can profoundly influence the overall financial market.

Besides, China is the largest trading partner of Australia and New Zealand, purchasing a significant amount of commodities from these countries.

Therefore, positive macro statistics from China may also exert a positive influence on these commodity currencies. Conversely, if the anticipated data indicates a deceleration in one of the world’s largest economies, it would be a detrimental factor for global stock markets and commodity currencies.

In addition, the National Bureau of Statistics of China will release the GDP growth data for Q2 2026.

China’s GDP is expected to grow again in Q2 2026 after +1.3% (+5.0% YoY) in Q1 2026, 1.2% (+4.5% YoY) in Q4 2025, +1.1% (4.8% YoY) in Q3, +1.1% (+5.2% YoY) in Q2 2025, +1.2% (+5.4% YoY) in Q1 2025, +1.6% (+5.4% YoY) in Q4 2024.

An increase in the indicator is a positive factor for the yuan. Conversely, a decline in the indicator may negatively affect the yuan, as well as currencies in the Asia-Pacific region, particularly the Australian and New Zealand dollars.

12:30 – USD: Producer Price Index (PPI)

The Producer Price Index (PPI) measures the average change in wholesale prices determined by manufacturers at all stages of production. The index is one of the leading inflation indicators in the United States, estimating the average change in wholesale producer prices.

Rising production costs increase wholesale selling prices, which ultimately boosts inflation. In normal economic conditions, growing inflation usually puts upward pressure on the national currency, implying a tighter central bank monetary policy.

Previous figures: +1.4% (+6.0%), +0.7% (+4.3%), +0.5% (+3.4% YoY), +0.6% (+3.1% YoY) in January 2026, +0.4% (+3.2% YoY) in December 2025, +0.4% (+3.1% YoY), +0.1% (+2.8% YoY), +0.6% (+3.0% YoY), -0.2% (+2.7% YoY), +0.8% (+3.2% YoY), +0.1% (+2.4% YoY), +0.4% (+2.7% YoY), -0.3% (+2.4% YoY), -0.2% (+3.2% YoY), +0.1% (+3.4% YoY), +0.7% (+3.8% YoY) in January 2025.

If the data exceeds the forecasted value, the US dollar will likely strengthen. Conversely, if the data falls below forecasted and previous values, this will exert pressure on the Fed. This could lead to the Fed’s monetary policy easing, which will negatively impact the US dollar.

13:45 – CAD: Bank of Canada Interest Rate Decision and Accompanying Statement

At its June 5, 2024, meeting, the Bank of Canada cut its interest rate by 0.25% to 4.75% for the first time since July 2023. Over the course of 2024, it reduced the rate by a total of 1.75% (175 basis points), and in October 2025, brought it down further to the current 2.25%.

It is unclear what decision the Bank of Canada’s policymakers will make this time, given the ongoing events in the Middle East and the sharp rise in oil prices. The bank may decide to take a pause at this meeting.

If the Bank of Canada’s accompanying statement regarding growing inflation and the prospects for further monetary policy signals further tightening, the Canadian dollar will strengthen. Conversely, if the regulator signals the need for a monetary policy easing, the Canadian currency will decline.

14:30 – CAD: Bank of Canada Press Conference

During a press conference, Bank of Canada Governor Tiff Macklem will outline the bank’s stance and assess the country’s current economic situation. If the tone of his remarks appears hawkish, the Canadian dollar will strengthen on the currency market. If Tiff Macklem advocates maintaining a loose monetary policy, the Canadian currency will weaken. In any case, the Canadian dollar is expected to experience high volatility during his remarks.

Thursday, July 16

12:30 – USD: US Retail Sales. Retail Sales Control Group

This Census Bureau report on retail sales reflects the total sales of US retailers of all sizes and types. The change in retail sales is a key indicator of consumer spending. The report is a leading indicator, and the data may be subject to significant revisions in the future. High indicator readings strengthen the US dollar, while low readings weaken it. A relative decline in the indicator may have a short-term negative impact on the US dollar, while a rise in the indicator will positively impact the currency.

In May 2026, the value stood at +0.9% after +0.5%, +1.6%, +0.7%, 0%, 0% in December 2025, +0.5% in November, -0.2% in October, +0.1% in September, +0.5% in August, +0.6% in July, +1.0%, -0.8%, -0.2%, +1.7%, 0%, -0.8% in January 2025.

Retail sales are the main indicator of consumer spending in the United States, showing the change in the retail industry.

Retail sales serve as an indicator of domestic consumption, contributing the most to the US GDP and being one of the main factors influencing inflation. Deterioration of the indicator values is a negative factor for the US dollar. Inflation deceleration may prompt the Fed to begin the process of monetary policy easing.

The Retail Control Group indicator gauges volume in the retail industry and is used to calculate price indexes for most goods. High readings strengthen the US dollar, while low readings weaken the currency. A slight increase in the figures is unlikely to boost the dollar. If the data is lower than the previous readings, the dollar may be negatively impacted in the short term. Previous values: +0.7%, +0.5%, +0.8%, +0.6%, +0.5%, 0%, +0.2%, +0.5%, -0.2%, +0.7%, +0.5%, +0.9%, +0.3%, 0%, +0.2%, +1.3%, -0.9% in January 2025.

Friday, July 17

14:00 – USD: University of Michigan Consumer Sentiment Index (Preliminary Release)

This indicator reflects American consumers’ confidence in the country’s economic development. A high reading indicates economic growth, while a low one points to stagnation. Previous indicator values: 49.5, 44.8, 49.8, 53.3, 56.6, 56.4 in January 2026, 52.9 in December 2025, 51.0 in November, 53.6 in October, 55.1 in September, 58.2 in August, 61.7 in July, 60.7 in June, 52.2 in May and April, 57.0 in March, 64.7 in February, 71.1 in January 2025. An increase in the indicator will strengthen the US dollar, while a decrease will weaken the currency. The data shows that the recovery of this indicator is uneven, which is unfavorable for the greenback. A decline below previous values will likely negatively impact the US dollar in the near term.

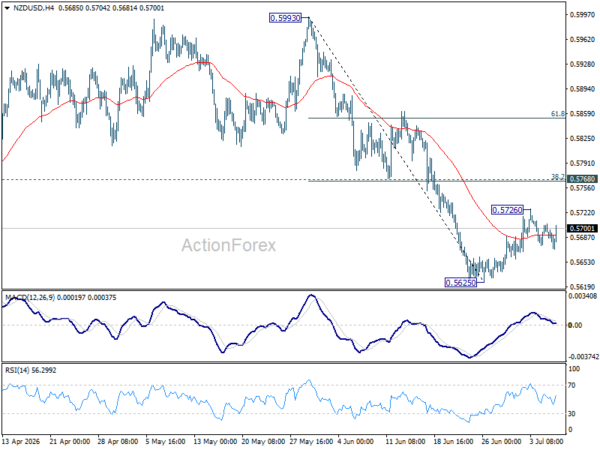

Price chart of USDX in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.