As we predicted, the S&P 500 had a June Swoon. We expected that it would be more of a broadening rotation than a widespread correction. That’s the way it played out. The S&P 500 market-weighted stock price index peaked at a record high of 7,609.78 on June 2 (chart). It fell 3.4% through Friday’s close. Over that same period, the S&P 500 equal-weighted stock price index was unchanged (chart).

Investors seem to be experiencing AI Fatigue. They are questioning whether the hyperscalers’ massive spending on AI infrastructure will ever pay off. They see token prices falling, suggesting there might already be excess compute capacity. They see that yet another Chinese company is offering cheaper, powerful, and open-source LLMs. They worry that new technologies will rapidly make current ones obsolete in a process known as “creative destruction.”

Companies are experiencing “token budget hangover,” where agentic AI usage is blowing up forecasted budgets. Microsoft is eyeing DeepSeek as a hyper-cheap, optional alternative to the expensive OpenAI and Anthropic models currently powering its enterprise agent tool, Copilot Cowork. To cut its own soaring internal AI token usage costs, Microsoft issued a firm June 30, 2026 cutoff deadline for its Experiences + Devices (E+D) division—the engineering teams behind Windows, Office, Teams, and Surface—to stop using Anthropic’s Claude Code.

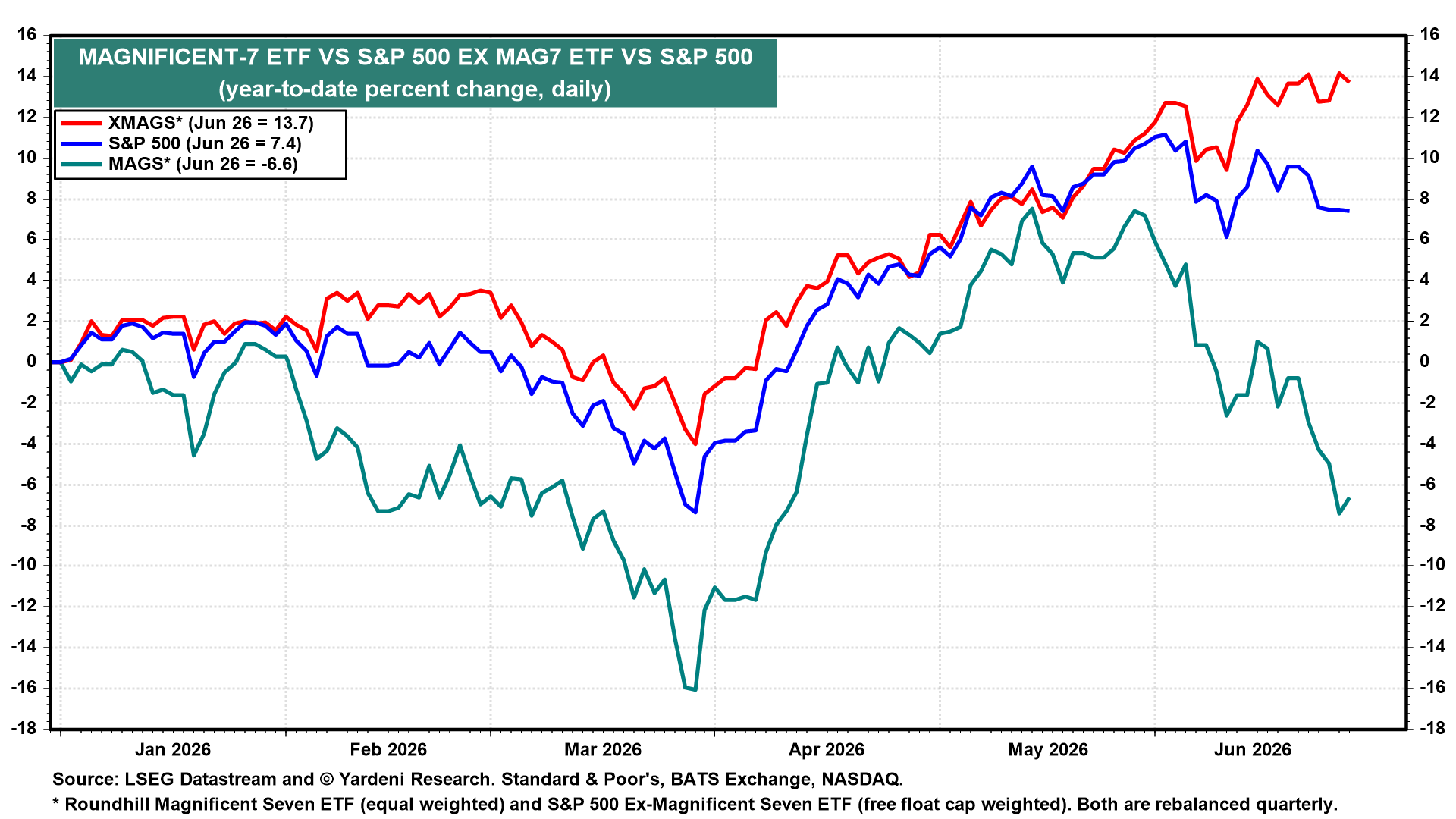

As a result, the Mag-7, which includes the biggest hyperscalers, hasn’t been so magnificent in June. The MAGS ETF peaked at a record high on May 26 and fell 12.9% though Friday’s close (chart). It is down 6.6% ytd, while the XMAGS ETF (a.k.a. the “Impressive 493”) is up 13.7%. The Mag-7s have been the Lag-7s.

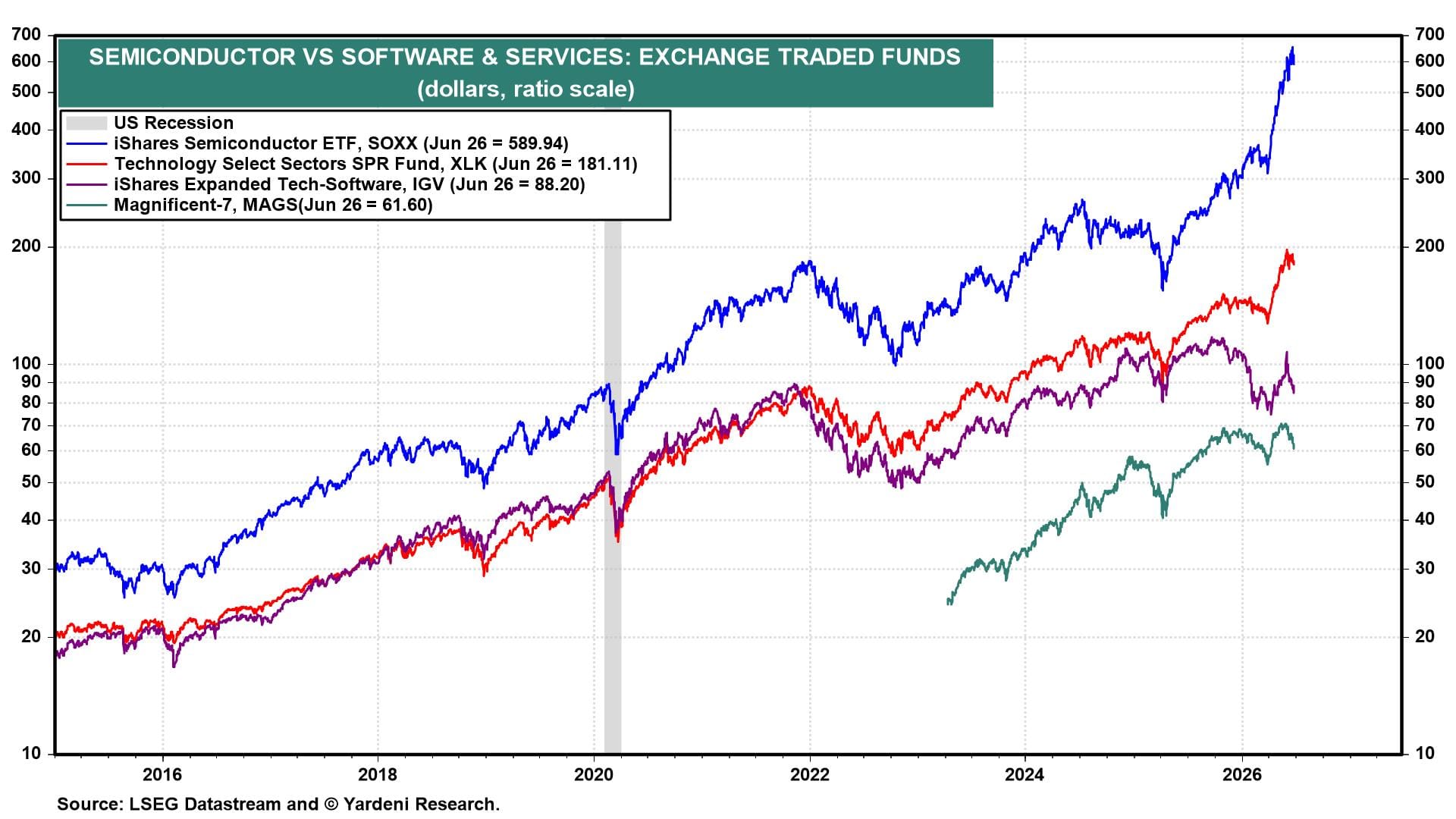

While the MAGS and IGV (i.e., software ETF) swooned during June, the SOXX semiconductor ETF continued to soar to a new record high on June 22 (chart). So there has been rotation even within the Information Technology sector.

Now let’s turn to some other market-moving developments:

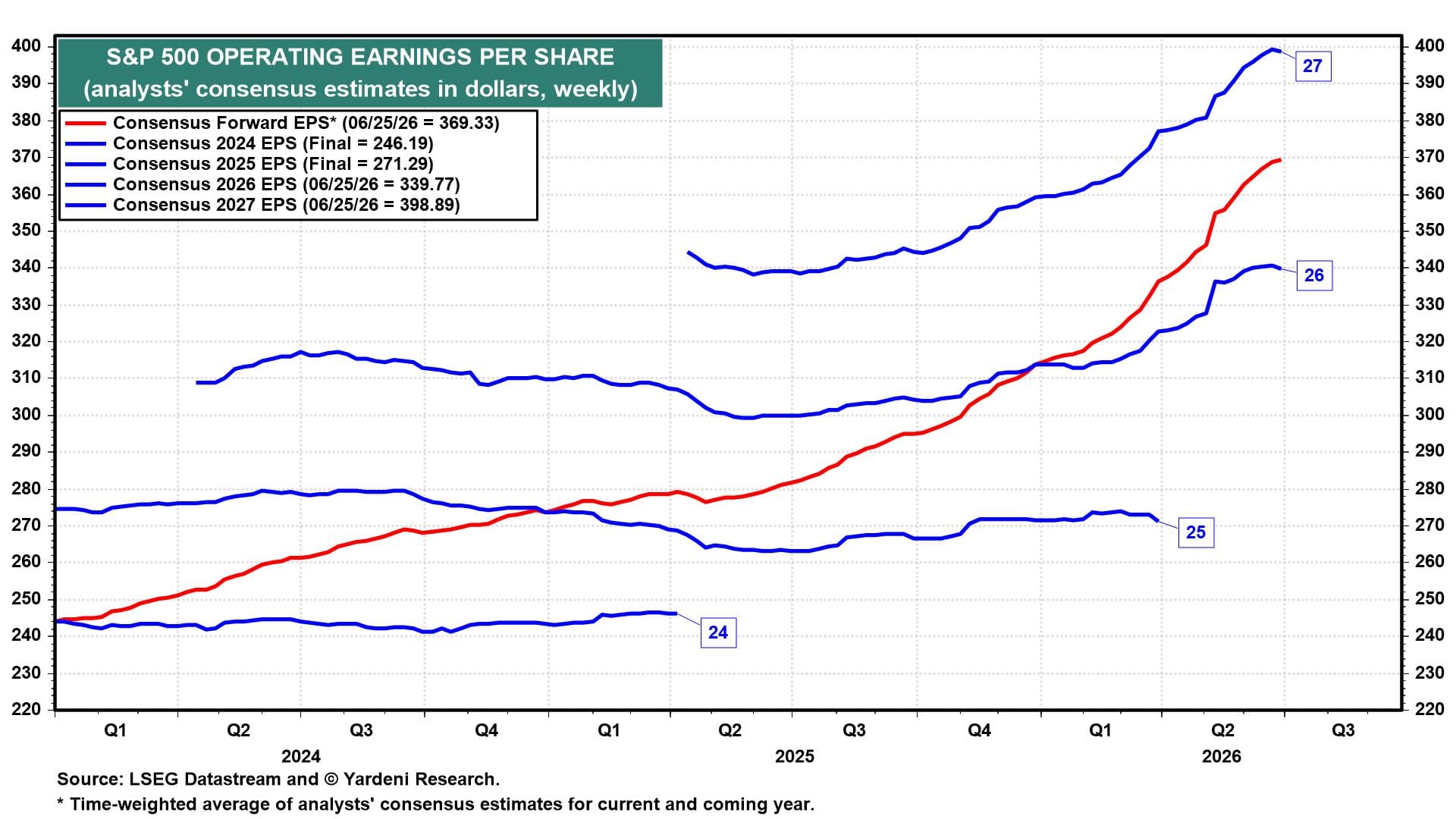

(1) Earnings. FEMO (Fabulous Earnings Momentum) may be starting to lose a wee bit of its mojo. S&P 500 forward earnings edged up to another record high during the week of June 25 as both the 2026 and 2027 analysts’ consensus earnings expectations edged down (chart).

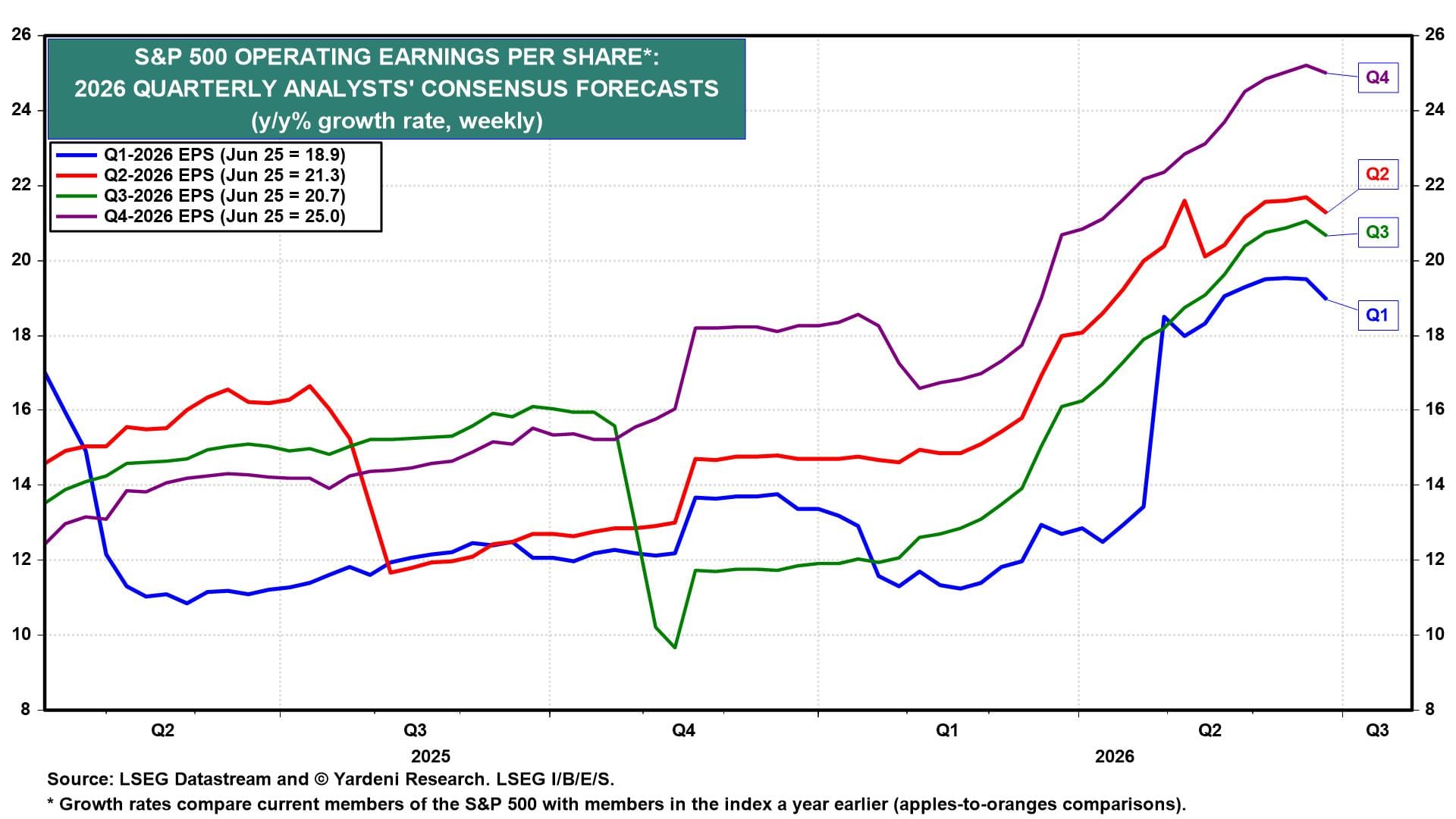

The same can be said for the analysts’ consensus earnings estimates for Q2-Q4 of 2026 (chart). However, they are still forecasting y/y growth rates in the low- to mid-20s.

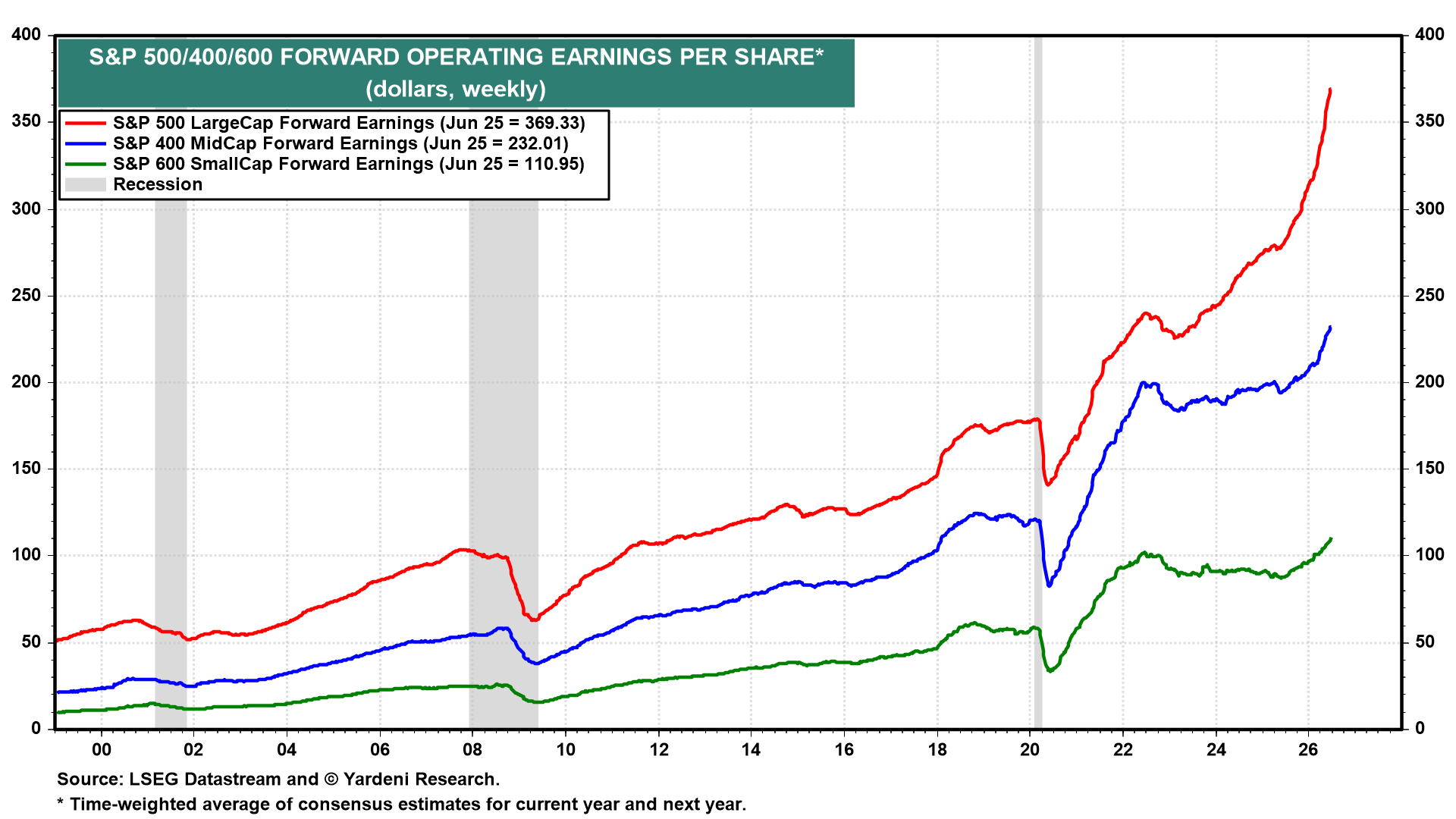

The forward earnings of the S&P 500, S&P 400, and S&P 600 all rose to record highs last week (chart). This confirms that FEMO continues to broaden within the stock market.

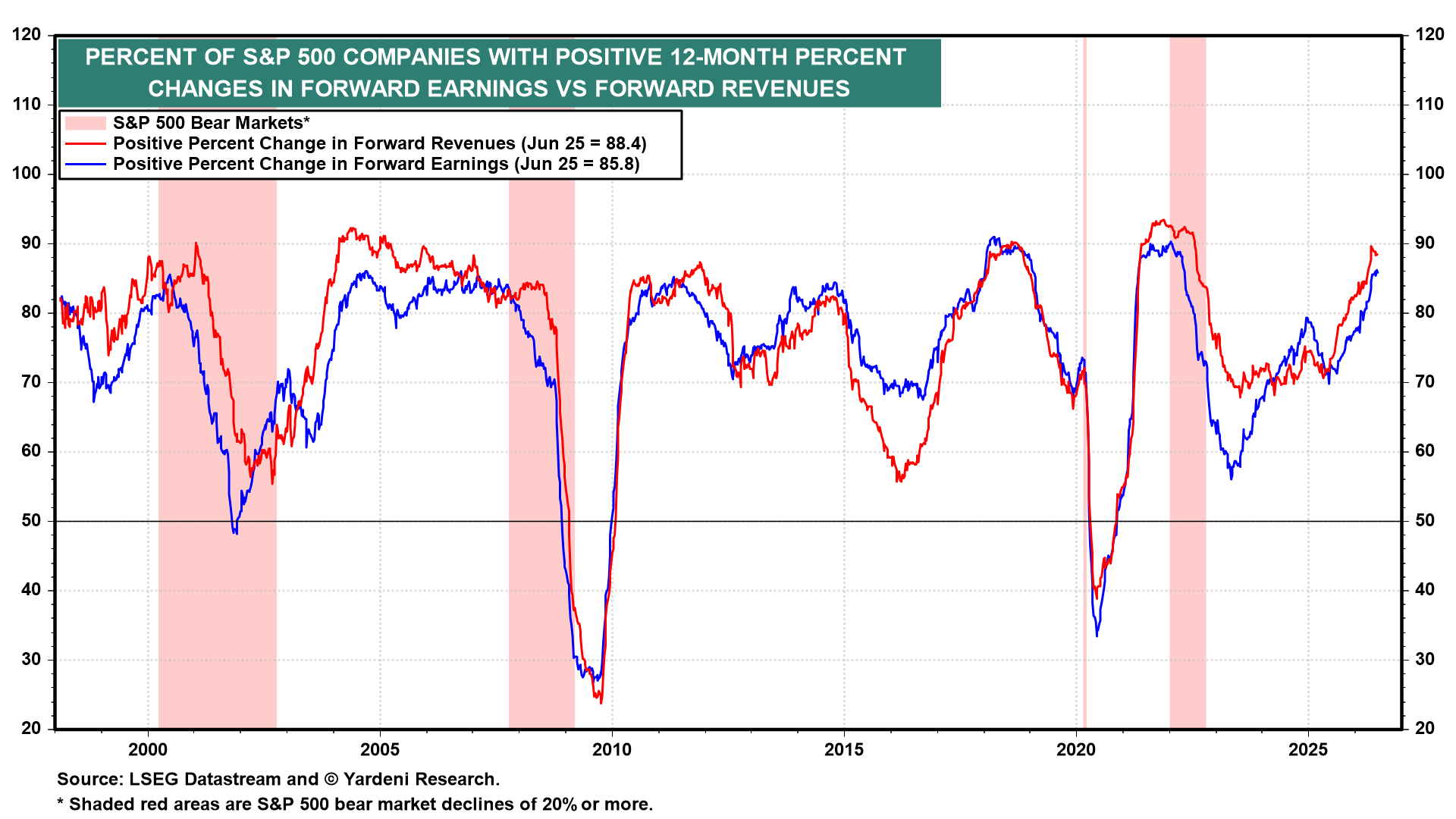

FEMO is also confirmed by the percent of S&P 500 companies with positive 12-month percent changes in forward revenues (88.4%) and forward earnings (85.8%) (chart).

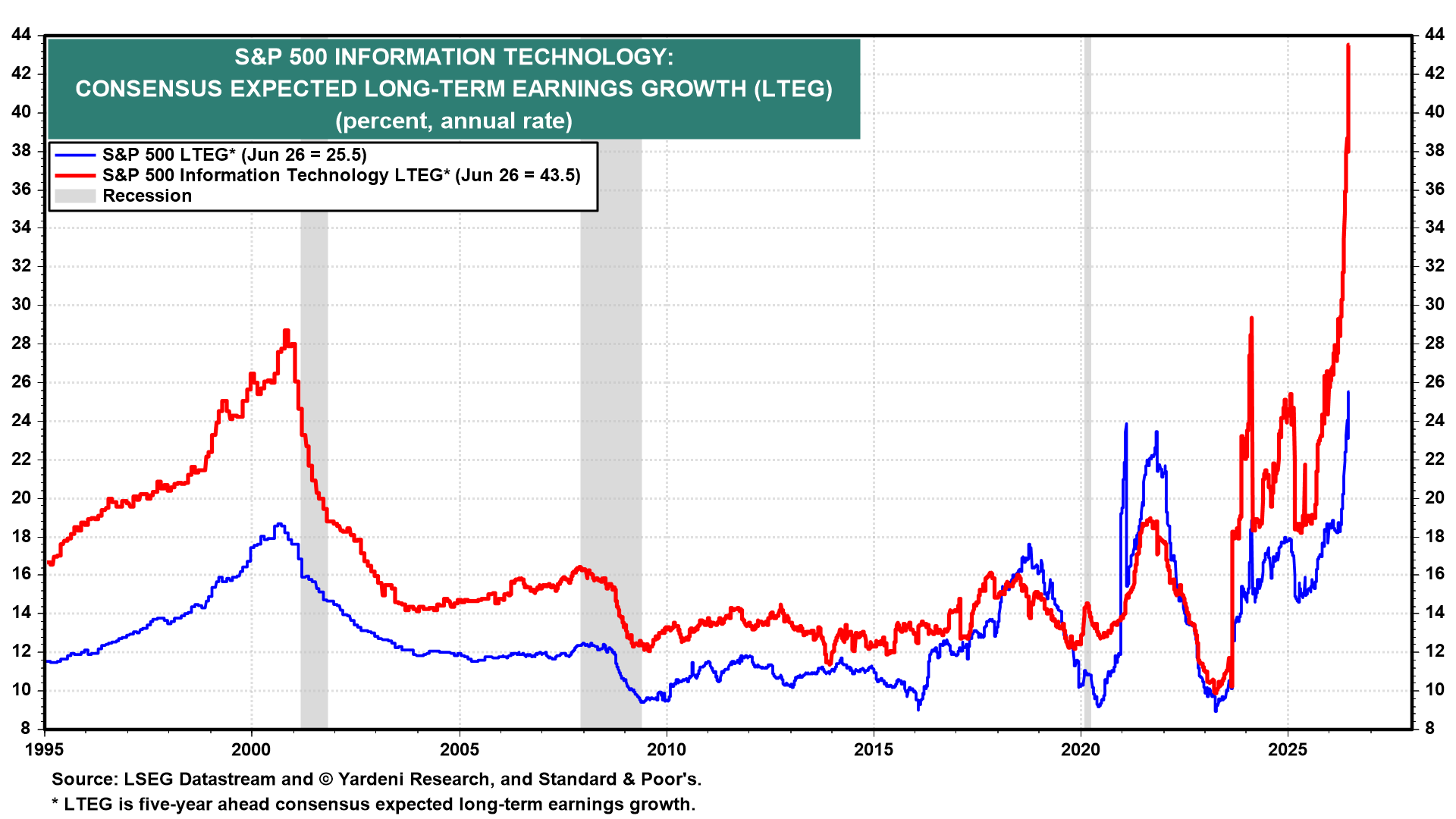

Irrational exuberance is starting to show up in FEMO, as consensus-expected long-term earnings growth (LTEG) rose to a record 43.5% for the S&P 500 Information Technology sector last week (chart). That boosted the LTEG of the S&P 500 to a record 25.5%.

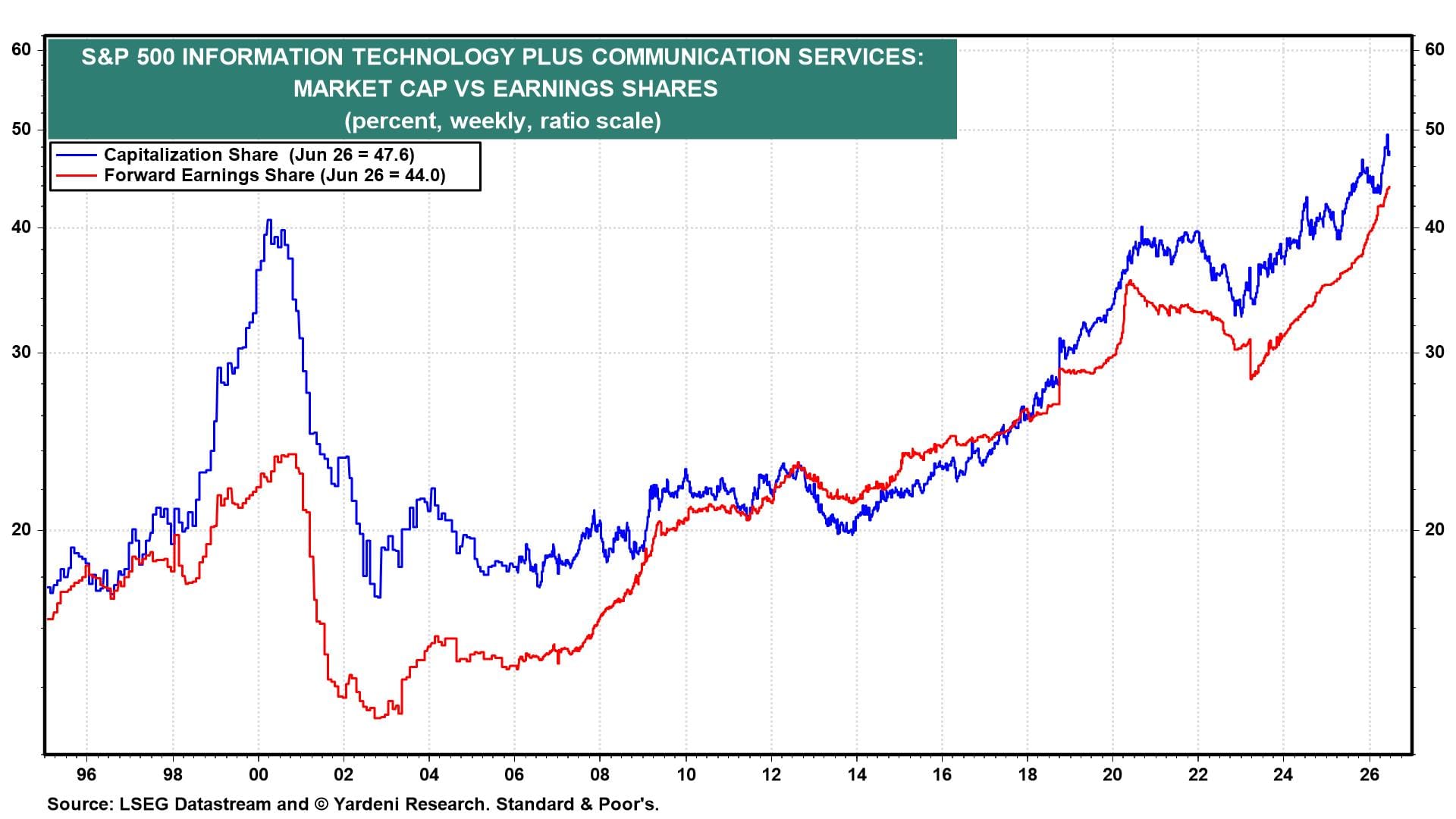

Meanwhile, the combined forward earnings share of the S&P 500 Information Technology and Communication Services sectors rose to a record 44.0% last week (chart). Such FEMO has driven the sectors’ combined market-cap share to 47.6%. That suggests a bubble only if the analysts who cover companies in these two sectors are irrationally exuberant about forward earnings, which have been driven by much better-than-expected earnings during the Q1-2026 earnings season.

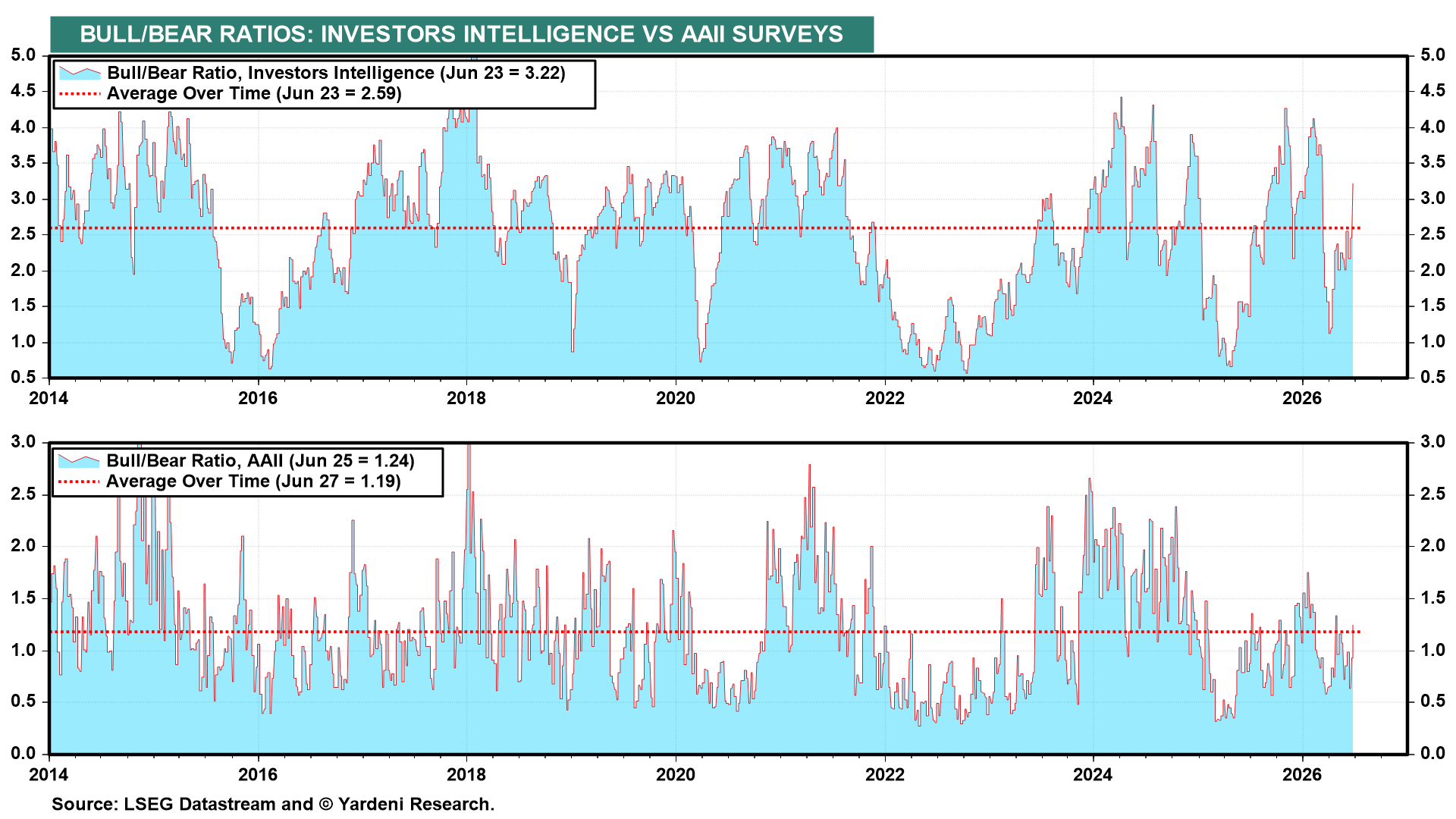

(2) Sentiment. Meanwhile, the Bull-Bear Ratios that we follow indicate greater bullishness relative to their historical averages (chart). They aren’t high enough yet to provide a sell signal from a contrarian perspective.

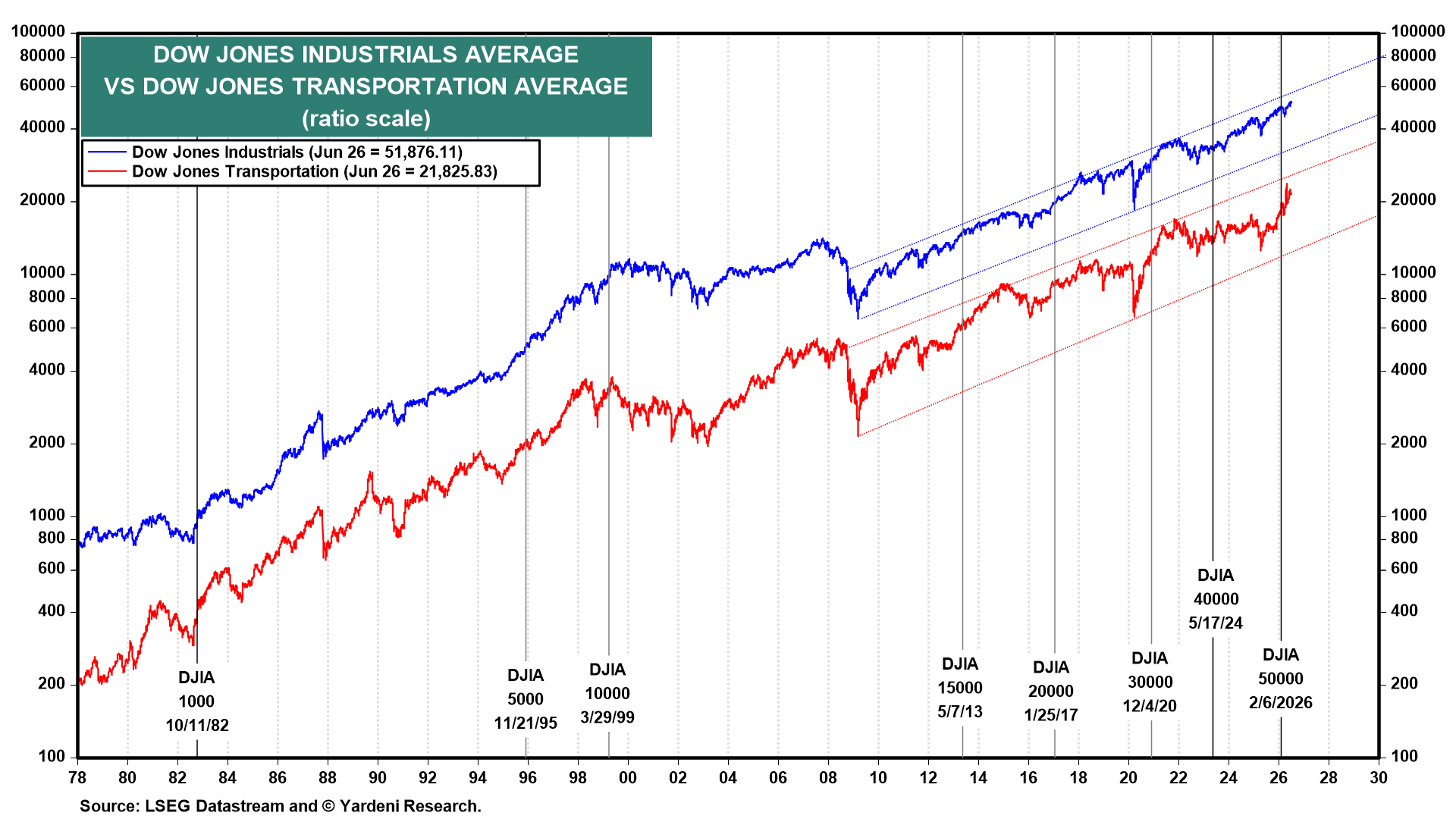

(3) Dow Theory. Both the DJTA and the DJIA have been very strong so far this year. Both are near their recent record highs (chart). So Dow Theory remains bullish.

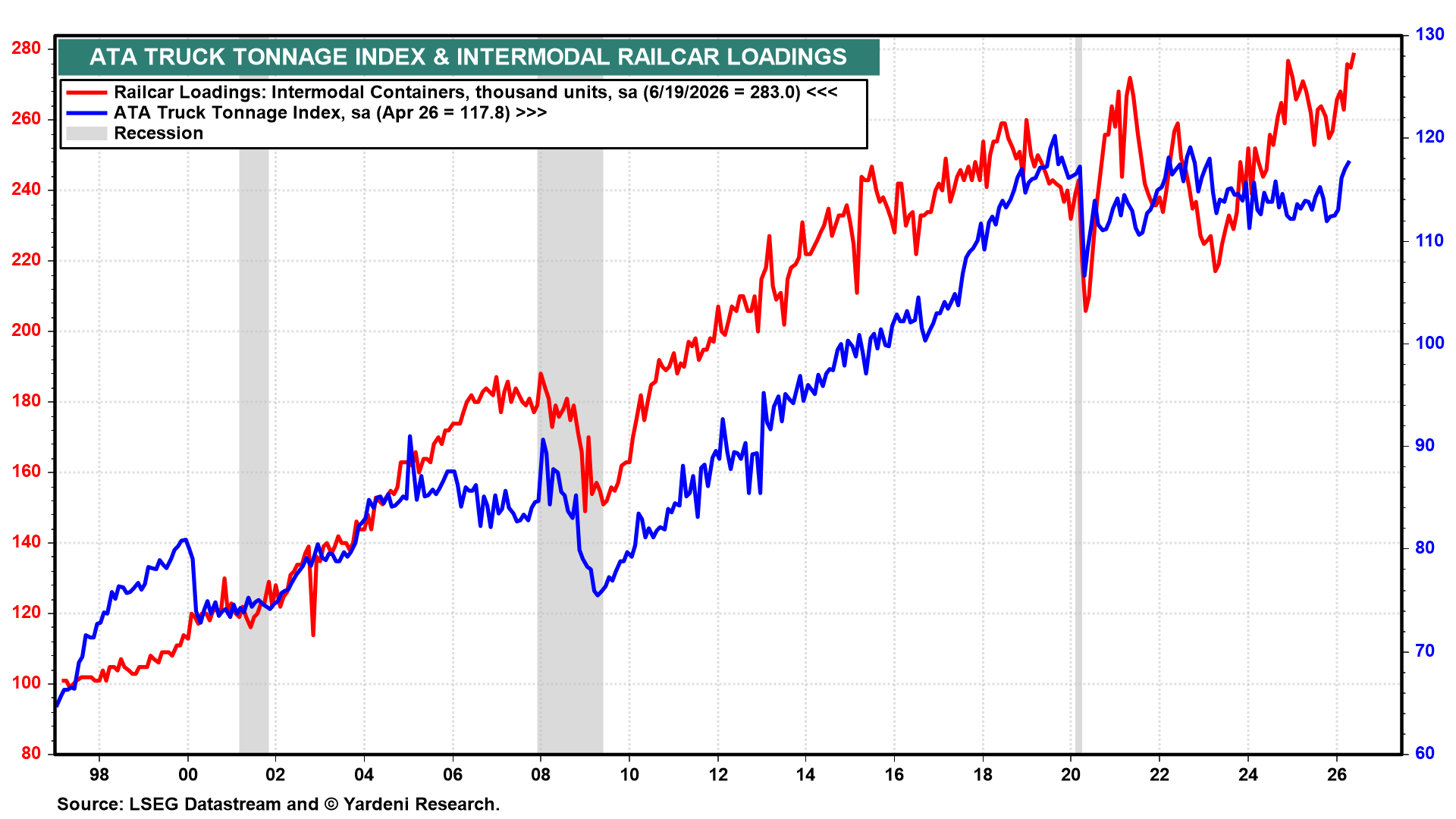

The transportation sector of the economy is showing recent improvement in ATA Truck Tonnage through April, along with a new record high in railcar loadings of intermodal containers through the week of June 19 (chart).

💡

Join the discussion with Ed below! To leave comments or questions, log in to the Yardeni QuickTakes website and post them at the end of the QuickTakes article. Paid members’ contributions may be featured in our segment, “Ed Answers Your Questions”.