Key Points

The two companies obviously have a lot in common, and it goes beyond having Elon Musk as their CEO. The reality is that they are both stocks valued and bought today, not for their current earnings, but for what they could become in the future.

However, there are key differences between the investment profiles of Tesla (NASDAQ: TSLA) and Space Exploration Technologies (NASDAQ: SPCX), better known as SpaceX, that make them suitable for different types of investors and also challenge the notion that folding Tesla into SpaceX is a good idea.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Three key differences between Tesla and SpaceX

The major factors to consider are as follows:

- Tesla’s projects (electric vehicles, robotaxis, and Optimus robots) embody artificial intelligence (AI). At the same time, SpaceX is largely dependent on end demand for AI, not least for its xAI business and its orbital data center ambitions.

- The scaling of Tesla’s long-term recurring income drivers, namely robotaxis and Optimus are, despite the delays and previously over-optimistic assumptions articulated by Musk, much closer to near-term fruition than SpaceX’s.

- The two companies have vastly different medium-term capital expenditure requirements and cash flow profiles, with SpaceX requiring significantly more investment.

Putting these points together, it’s clear that, while both are growth stocks and priced as such, Tesla is less risky than SpaceX and has a shorter time horizon before it starts scaling earnings and cash flow. That’s not to argue that Tesla is necessarily the better stock, but rather to point out that they will suit different types of investors.

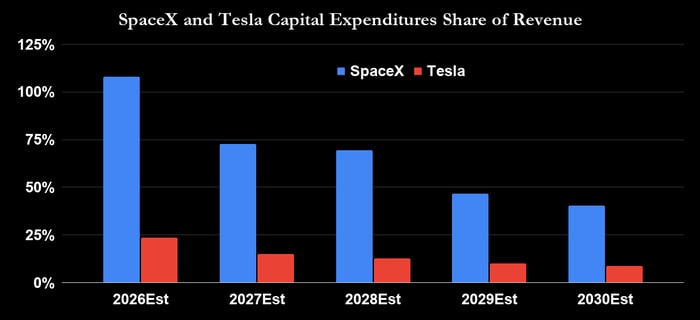

Capital expenditure requirements and cash flow

The chart below shows the Wall Street consensus on capital spending. It implies that SpaceX will put more into capital expenditures than it generates in revenue in 2026 and will still be at a whopping 40% of revenue in 2030.

Meanwhile, Tesla’s relative capital spending is expected to decline as revenue grows and its phase of significant investment in securing its supply chain moderates. Tesla is investing heavily right now to build a lithium refinery and a lithium battery production plant, and is beginning to produce the Cybercab, Semi, and Optimus.

Data source: S&P Global Market Intelligence. Wall Street consensus. Chart by the author.

Tesla’s catalysts are near-term

Investors can be forgiven for growing restless given the timing of Tesla’s key initiatives (robotaxis/Cybercab and Optimus); the reality is that they are much closer to fruition than orbital data centers.

For example, Tesla is taking a very cautious approach to ramping the robotaxi rollout. On the lastearnings call Musk made it clear that “it wouldn’t be right for us to go to like very large scale unsupervised FSD when we know that there are software improvements in the pipeline that would improve safety.” Those improvements are likely to come with v15 of its full self-driving (FSD) software due in late 2026 or early 2027.

Image source: Tesla.

That’s when investors can start to expect a significant and “very large scale” rollout. Still, it’s a lot closer than SpaceX’s orbital data centers. SpaceX expects to deploy them in 2028, but as clearly stated in the initial public offering (IPO) registration filing, “the timeline for certain of our initiatives involving unproven or new innovations, including our goal of deploying 100 gigawatts of annual compute power to orbit … may be difficult or impossible to determine.”

A different kind of AI company

As previously discussed in more detail, Tesla’s solutions embody AI, making it one of the most exciting ways to play on the growth of AI capability. While SpaceX also benefits from these trends, it’s much more dependent on the growth in AI applications. If demand slows, it could “result in existing terrestrial data centers sufficiently meeting such demand, thereby reducing the need for our orbital AI compute infrastructure,” according to SpaceX filings.

Which stock is better?

Ultimately, the decision boils down to your risk profile, level of confidence in the growth of AI applications, and willingness to wait for each company’s growth catalysts to come to fruition.

Those differences in investment profiles also make a potential merger somewhat problematic, as Tesla investors will be swapping the likelihood of a ramp in recurring cash flows from robotaxis and Optimus for the prospect of those cash flows being reinvested to support long-term growth in SpaceX’s existing businesses. That might not suit most Tesla investors unless the acquisition price is a significant premium.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $519,482!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $56,092!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $392,713!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of June 24, 2026.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.