Greg Abel took over from Warren Buffett as CEO of Berkshire Hathaway at the beginning of the year. His first quarter at the helm was eventful. Abel and his team closed several positions while buying shares in new companies. Some of his choices were not surprising. For instance, Apple remains Berkshire Hathaway’s largest holding, which everyone expected. Another decision the conglomerate made that may seem odd at first but actually makes sense is the choice to get rid of Amazon (AMZN +1.60%).

Image source: Getty Images.

Why Berkshire Hathaway dumped Amazon

Amazon is a leader in e-commerce and cloud computing. It provides exposure to several other markets. The company’s revenue and earnings are growing at a good clip, and it has attractive long-term prospects across several niches in which it competes. Further, Amazon benefits from a wide moat from its brand name, network effects, and switching costs. All of these factors (and more) arguably make the stock an attractive long-term bet and one that, to some extent, aligns with the criteria prominent in the Buffett school of investing.

Today’s Change

(1.60%) $4.00

Current Price

$254.02

Key Data Points

Market Cap

$2.7T

Day’s Range

$251.78 – $255.83

52wk Range

$196.00 – $278.56

Volume

1.4M

Avg Vol

44.8M

Gross Margin

50.60%

However, Amazon made up a small percentage of Berkshire Hathaway’s portfolio. The conglomerate owned about 2.3 million shares as of the fourth quarter. That accounted for a tiny portion of Berkshire’s massive $263 billion portfolio. Further, Abel and his team sold many of the stocks (including Amazon) managed by Todd Combs, who left the company in December to join JPMorgan. So, it wasn’t a particularly shocking move. Let’s look into one decision Abel made during the first quarter that seems like far more of a head-scratcher.

Berkshire buys a stake in a legacy retailer

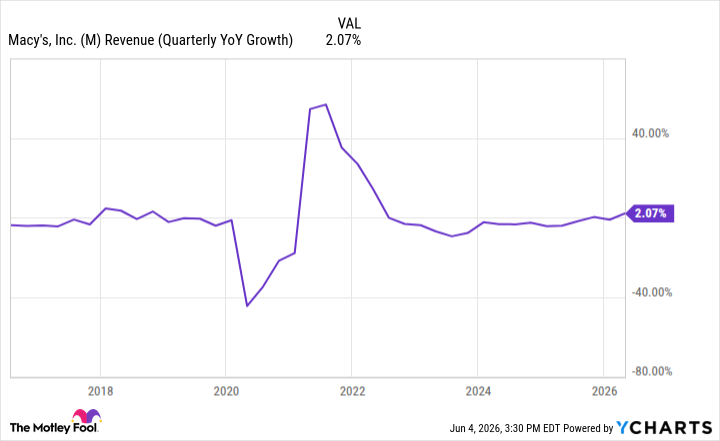

Berkshire Hathaway bought about three million shares of Macy’s (M +5.64%). At first glance, this looks like a dubious decision. Macy’s has faced significant problems in recent years — in fact, the last decade has not been kind to the retailer. The shift to e-commerce and the decline in mall and department store foot traffic have led to poor financial results. Meanwhile, Macy’s has faced growing competition from a variety of sources, not just online stores. The company has struggled to grow revenue at a good clip for a long time, and the strongest top-line increase in recent years came after the pandemic, when customers who had been stuck at home finally had the opportunity to go out again.

M Revenue (Quarterly YoY Growth) data by YCharts

In fairness, Macy’s has made some progress. More recent financial results have been stronger amid a push to turn things around. The company notably decreased its retail footprint by closing many unprofitable stores and selling off real estate assets while making a push in e-commerce.

Today’s Change

(5.64%) $1.23

Current Price

$23.03

Key Data Points

Market Cap

$6.1B

Day’s Range

$21.93 – $23.59

52wk Range

$10.54 – $24.41

Volume

13M

Avg Vol

7M

Gross Margin

40.31%

Dividend Yield

3.21%

It’s also admirable that Macy’s has survived this long, especially as other legacy retailers weren’t so lucky and have now gone out of business. However, can Macy’s deliver strong returns from now on? Or is there another reason Abel and his team got in the game? Perhaps Berkshire Hathaway is attracted to Macy’s real estate holdings because they may be more valuable than the market is giving the company credit for. It’s in that sense that the retail giant may be “undervalued.”

We could also look at traditional valuation metrics. Macy’s is trading at 10.2x forward earnings, which is lower than the consumer discretionary average of 26.2. Macy’s also appears undervalued by this standard, at least at first glance. It’s also worth pointing out that in the first quarter of its fiscal year 2026, ending on May 2, Macy’s net sales increased by 1.8% year over year to $4.7 billion, while comparable sales grew 3% year over year. The company’s adjusted earnings per share climbed to $0.13, 18% higher than the year-ago period.

The company beat Wall Street estimates on the top and bottom lines. Macy’s increased its guidance for its full fiscal year 2026 as well. Macy’s is moving in the right direction. There is plenty of risk remaining here, and that’s probably one reason why Berkshire Hathaway did not buy enough of the company’s shares to make it anything close to a top holding in its portfolio. However, at current levels, Macy’s might be worth a second look for contrarian value investors.