As of June 2, the benchmark S&P 500 (^GSPC 0.74%) index had hit 23 all-time highs in 2026. That’s following 96 all-time highs in 2024 and 2025.

Now sitting just below its latest high, the market has absolutely crushed it despite facing several headwinds, including doubts about AI at the very beginning of the year; the Iran war, which drove up oil and gas prices; and now, concerns about elevated inflation.

Exuberance over artificial intelligence and projected earnings growth of the S&P 500 has powered the market through these concerns. In fact, the stock market has traded at this high a valuation only one other time in its 69-year existence. History couldn’t be any clearer about what happens next.

Image source: Getty Images.

Pushing dot-com level highs

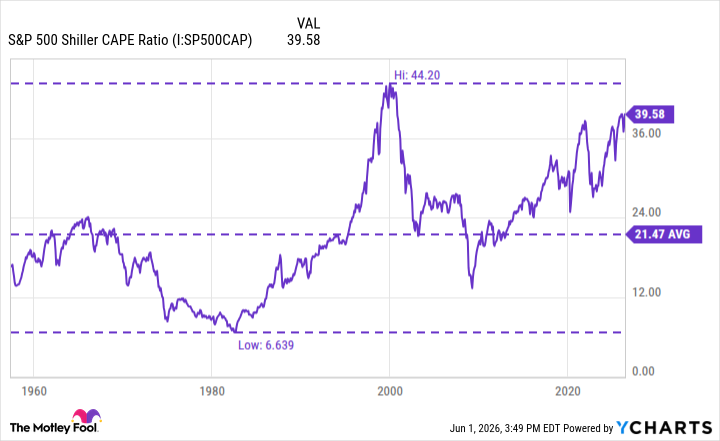

One way to assess the value of the S&P 500 is through the Shiller CAPE ratio, which compares the S&P 500’s price to its 10-year average inflation-adjusted earnings per share (EPS).

The idea behind using a 10-year, inflation-adjusted average EPS is to smooth out the noise of the economic cycle or periods with differing inflation to get a more holistic view of how the market is trading. For a while now, the S&P 500’s Shiller CAPE ratio has been creeping toward alarmingly high levels.

S&P 500 Shiller CAPE Ratio data by YCharts.

As you can see, dating back to the creation of the S&P 500 in 1957, the only other time the index had a higher Shiller CAPE ratio was in 2000, right before the dot-com bubble popped.

The tale bears similarities to the current situation. During the dot-com bubble, venture capital for start-ups soared amid the rise of the internet. Investors also poured into tech stocks, driven by fear of missing out (FOMO).

The fallout of the dot-com bubble was not pretty. The S&P 500 fell nearly 77% over the next two years.

The Shiller CAPE ratio also approached this level in late 2021 and early 2022, as people built up savings during the COVID-19 pandemic’s height and pent-up demand emerged. However, inflation also got out of hand, and the Federal Reserve had to hike interest rates incredibly fast, leading to a 20% sell-off in 2022.

That’s not nearly as dramatic as the dot-com bubble, but the point is that when the S&P 500 reaches these levels, a sharp sell-off has always followed.

Is another big sell-off coming?

Many would argue that the artificial intelligence boom is very different than the dot-com bubble.

The internet boom featured many start-ups without revenue receiving venture capital, and large tech and telecom companies funded much of the internet infrastructure build-out with debt. In 1999, there were 457 IPOs, most of which were related to the internet.

Today, much of the AI infrastructure build-out is being funded by massive, highly profitable companies that generate tremendous free cash flow (FCF). However, the hyperscalers have begun to see their FCF wells dry up and are taking on debt to fund infrastructure.

The IPO market has also been quite soft in recent years. In the U.S., there have been 63 IPOs year to date. There were 150 in 2024 and 250 last year, according to Renaissance Capital.

Of course, the other big difference is that many start-ups have been able to raise funding and stay in the private markets longer than they used to.

Some also believe that AI will be more transformational than the internet, and that the market is not yet at peak dot-com-era levels, so it may still have some runway.

Long-term investors with a five- or 10-year horizon don’t need to do anything, as the market has bounced back from most of these steep sell-offs. But they should be aware of where the market is and check their portfolios to see if they hold AI stocks with ultra-high valuations that could be vulnerable to a sell-off.

I’m not saying to not own any of these, but be cognizant of your exposure to them.

If you are concerned about preserving capital over the next two to three years and highly valued AI stocks take up the majority of your portfolio, it may be time to take some gains, increase cash, or add exposure to sectors that are more resilient during market sell-offs.