| Company | Market Share (%) | Installations (GWh) |

|---|---|---|

| CATL | 40.1% | 141.4 |

| BYD | 14.2% | 50.0 |

| LG Energy Solution | 9.1% | 32.0 |

| CALB | 5.1% | 18.1 |

| Gotion High-tech | 4.4% | 15.6 |

| SK On | 3.5% | 12.3 |

| Panasonic | 3.4% | 12.0 |

| Eve Energy | 3.3% | 11.5 |

| Svolt | 2.6% | 9.3 |

| Sunwoda | 2.5% | 8.7 |

| Others | 11.8% | 41.7 |

- Seven Chinese companies rank among the top 10, commanding a combined 72.2% share of the global EV battery market.

- CATL’s market share increased compared to the same period last year, while BYD saw a slight decline.

CATL (HKEX: 3750) and BYD (HKEX: 1211) continued to dominate the fiercely competitive global electric vehicle (EV) battery market in the first four months of 2026, despite showing divergent performances.

Total global EV battery usage reached 352.7 gigawatt-hours (GWh) between January and April, representing a 13.8% increase from a year earlier, according to data released Tuesday by South Korean market research firm SNE Research.

CATL’s battery installations reached 141.4 GWh during the period, up 19.8% year-on-year.

The Chinese battery behemoth maintained its dominance in the global market from January to April, recording an overall market share of 40.1%. This was higher than the 38.1% seen in the same period last year, though slightly below the 40.7% recorded in the January-March period.

Second-ranked BYD experienced a minor setback in the first four months of 2026, registering total battery installations of 50.0 GWh, a 2.4% decline compared to a year earlier.

BYD’s global market share stood at 14.2% for the January-April period, keeping it firmly in the No. 2 spot globally. This was down from 16.5% a year ago, but higher than the 13.7% share it held in the first three months of the year.

The combined market share of the two Chinese giants reached 54.3%, underscoring the dominance of Chinese firms in the EV battery market.

South Korea’s LG Energy Solution (LGES) secured the third position globally with 32.0 GWh of battery installations in the first four months.

Although LGES saw its total usage grow by 8.3% year-on-year, its market share dropped to 9.1% from 9.5% a year earlier, as the broader market expanded at a faster pace.

China’s CALB (HKEX: 3931) posted EV battery installations of 18.1 GWh from January to April, a 39.3% year-on-year surge. It ranked fourth with a 5.1% market share.

China’s Gotion High-tech (SZSE: 002074) followed closely in fifth place with a 4.4% share. Its installations reached 15.6 GWh, achieving a 30.2% year-on-year growth during the period.

South Korea’s SK On suffered a notable decline, with its battery installations falling 7.9% year-on-year to 12.3 GWh.

The company ranked sixth globally with a 3.5% share, down from 4.3% a year earlier, a drop primarily attributed to slowing EV sales among its major customers in North America and Europe.

Japan’s Panasonic recorded installations of 12.0 GWh during the period, a 3.7% drop from the same period last year.

Its 3.4% share placed it seventh globally, down from 4.0% a year ago, largely impacted by slowing sales growth of its key customer, Tesla, in certain regions.

China’s Eve Energy (SZSE: 300014), Svolt Energy, and Sunwoda (SZSE: 300207) ranked eighth, ninth, and tenth in the global market, with battery installations of 11.5 GWh, 9.3 GWh, and 8.7 GWh, respectively. Their market shares stood at 3.3%, 2.6%, and 2.5%.

The three Chinese firms achieved year-on-year installation growth of 30.3%, 37.2%, and 17.6%, respectively, during the January-April period.

Among the top 10 companies globally, seven were Chinese companies, which together accounted for a 72.2% share of the global market.

This combined share increased by 2.1 percentage points from a year earlier, further squeezing the market space of their Japanese and South Korean rivals.

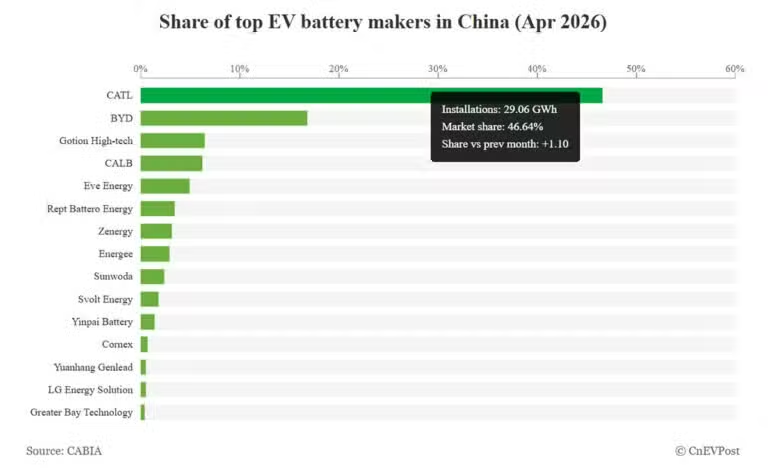

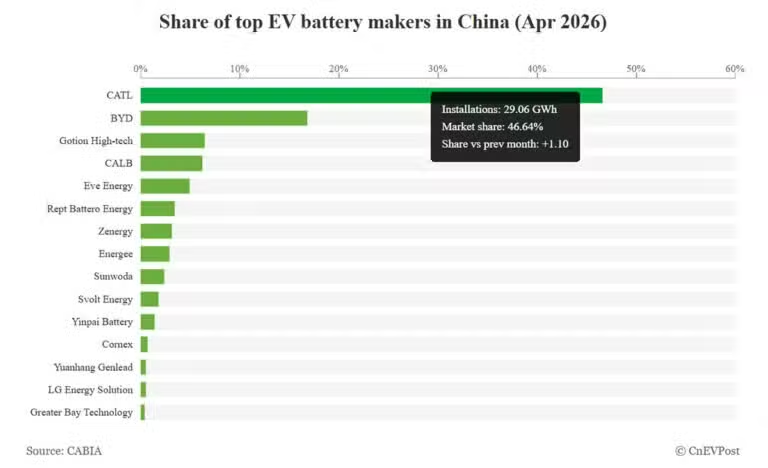

CATL consolidated its position as China’s largest power battery maker in April, with its share rising 1.1 percentage points from March.