- Wondering whether Luckin Coffee at US$32.52 is offering value or just noise in the headlines? This article breaks down what the current price is really implying.

- The stock has been relatively quiet over the last year with a 1.2% return, but that sits alongside a 3.9% gain over the past week and a decline of 7.7% over the last month and 8.2% year to date.

- Recent coverage has focused on Luckin Coffee’s position in the Chinese coffee market and the competitive backdrop with both local rivals and international chains expanding store counts and product ranges. There has also been attention on how the company is using promotions, digital ordering, and store formats to defend and grow its customer base, which can influence how investors think about future cash generation and risk.

- Against that backdrop, Luckin Coffee scores a valuation check of 6 out of 6. The rest of this article looks at how different valuation methods arrive at that result and why there may be an even better way to interpret what it means for you.

Approach 1: Luckin Coffee Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of the cash a company could generate in the future, then discounts those cash flows back to today to arrive at an estimated intrinsic value per share.

For Luckin Coffee, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flows in CN¥. The latest twelve month free cash flow is CN¥2,459.2m. Analyst projections and Simply Wall St extrapolations then extend this out, with forecast free cash flow of CN¥5,511.9m in 2028 and a set of projections running through 2035.

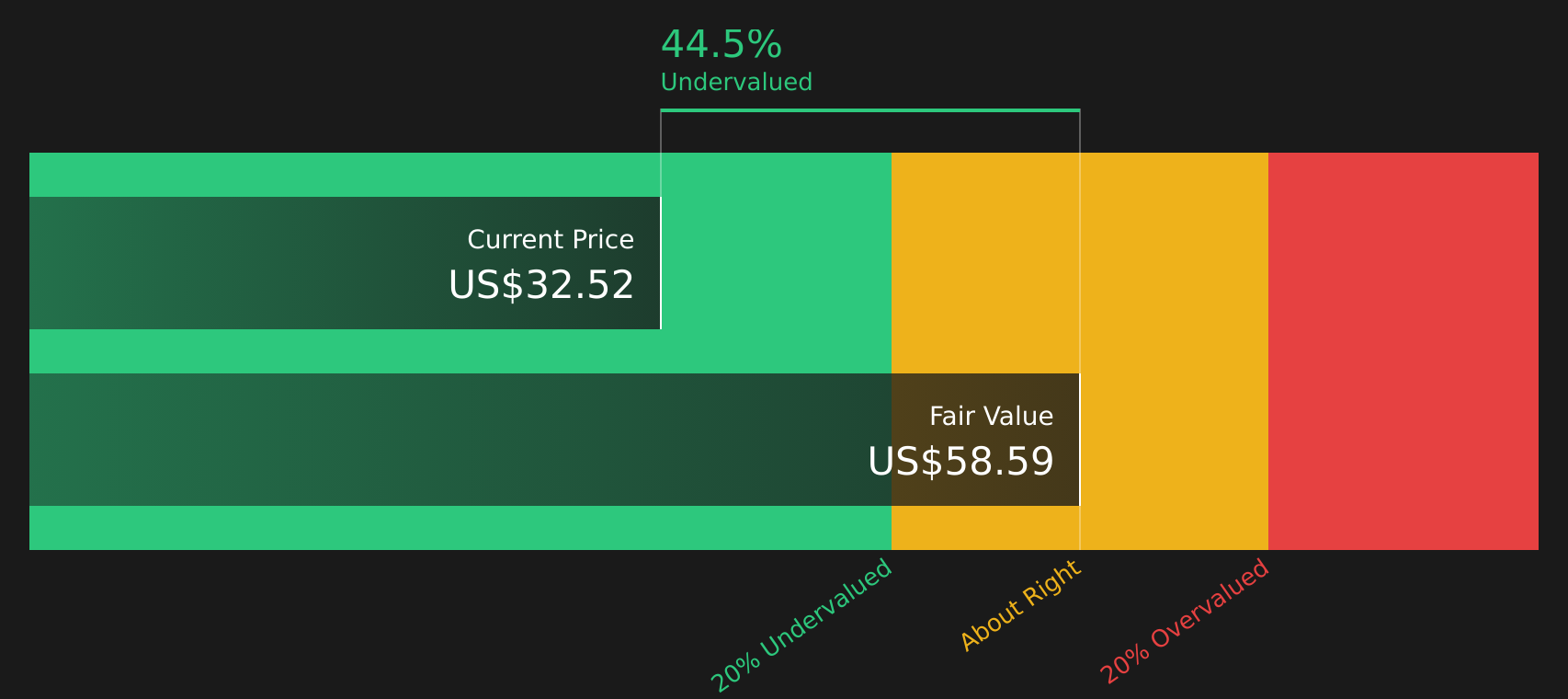

Each of these future cash flows is discounted back to today using a required return. They are then combined to produce an intrinsic value estimate of US$58.58 per share. Compared with the current share price of US$32.52, this implies the stock trades at a 44.5% discount to the DCF estimate. On this model, the stock appears undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Luckin Coffee is undervalued by 44.5%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Luckin Coffee Price vs Earnings

For profitable companies, the P/E ratio is a useful way to connect what you pay for each share with the earnings the company is currently generating. It gives a quick sense of how many dollars investors are willing to pay today for one dollar of current earnings.

In general, higher growth expectations and lower perceived risk can support a higher P/E ratio, while slower expected growth or higher risk usually line up with a lower P/E. That is why context is important rather than looking at the headline multiple in isolation.

Luckin Coffee is trading on a P/E of 19.85x, compared with an average of 20.31x for the wider Hospitality industry and 70.52x for its peer group. Simply Wall St’s Fair Ratio for the stock is 29.64x, which is a proprietary estimate of what the P/E might be given factors such as earnings growth, industry, profit margins, market cap and company specific risks.

This Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for those fundamentals rather than assuming all companies deserve similar multiples. Since Luckin Coffee’s current P/E of 19.85x is below the Fair Ratio of 29.64x, the multiple suggests the stock may be undervalued on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Luckin Coffee Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced here as a clear story you create about Luckin Coffee that links what you think about its store expansion, roasting network, margins and risks to specific forecasts for revenue, earnings and profit margins, and then connects those forecasts to a fair value that you can compare with the current share price.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors to turn views into numbers. You can see on one screen whether your fair value sits closer to the higher analyst target of US$54.68 or the lower target of US$38.50, and then decide for yourself whether the current price of US$32.52 looks attractive, fully valued or expensive.

Narratives are updated automatically when new information arrives, such as Luckin Coffee’s share repurchase plans, changes to fair value assumptions or news about its roasting capacity. This means your story, forecast and valuation stay aligned without you needing to rebuild a model each time.

Do you think there’s more to the story for Luckin Coffee? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com