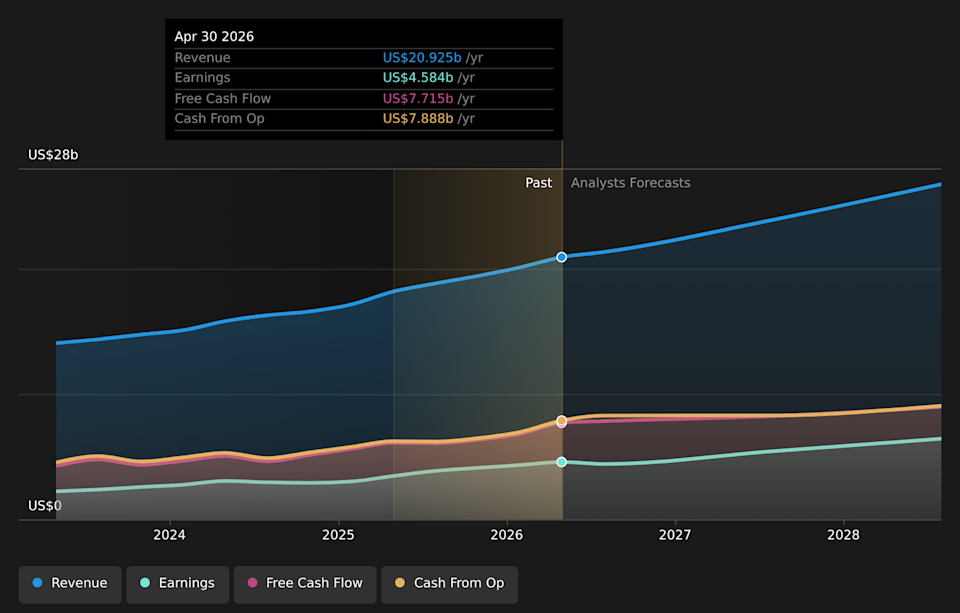

There’s been a notable change in appetite for Intuit Inc. (NASDAQ:INTU) shares in the week since its third-quarter report, with the stock down 19% to US$307. Intuit reported US$8.6b in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of US$11.09 beat expectations, being 3.0% higher than what the analysts expected. This is an important time for investors, as they can track a company’s performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We’ve gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

After the latest results, the 30 analysts covering Intuit are now predicting revenues of US$23.9b in 2027. If met, this would reflect a decent 14% improvement in revenue compared to the last 12 months. Per-share earnings are expected to expand 15% to US$19.33. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$23.9b and earnings per share (EPS) of US$18.95 in 2027. The analysts seems to have become more bullish on the business, judging by their new earnings per share estimates.

See our latest analysis for Intuit

The consensus price target fell 11% to US$525, suggesting the increase in earnings forecasts was not enough to offset other the analysts concerns. There’s another way to think about price targets though, and that’s to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Intuit analyst has a price target of US$921 per share, while the most pessimistic values it at US$315. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that Intuit’s revenue growth is expected to slow, with the forecast 11% annualised growth rate until the end of 2027 being well below the historical 15% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 17% annually. So it’s pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Intuit.