USD/JPY rose to 159.04 at the end of the week, marking the yen’s second consecutive weekly decline. The Japanese currency came under pressure after weaker inflation data reduced expectations of imminent Bank of Japan policy tightening.

Core inflation in Japan slowed to 1.4% in April, down from 1.8% the previous month – the lowest level in four years. Moreover, the indicator has remained below the Bank of Japan’s 2% target for the third consecutive month.

At its April meeting, the BOJ sharply raised its core inflation forecast for the current year to 2.8%, up from 1.9%. The regulator attributed this revision to high oil prices amid the Middle East conflict and the continued pass-through of business costs to consumers.

Additional market attention has been drawn to reports that Japanese Prime Minister Sanae Takaichi is considering an additional budget to compensate for rising energy prices.

At the same time, markets continue to monitor the risk of fresh foreign exchange interventions. The yen remains near the 160-per-dollar level — the level that triggered Japanese authorities’ interventions in late April and early May.

Technical Analysis

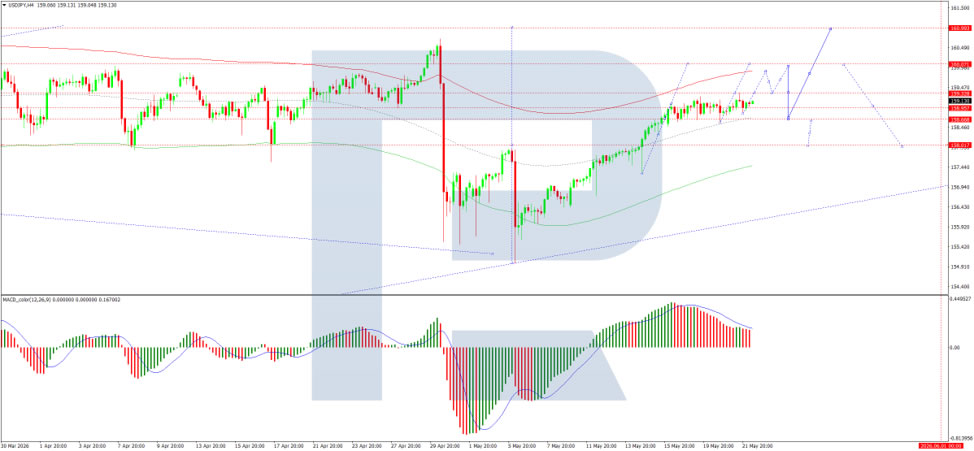

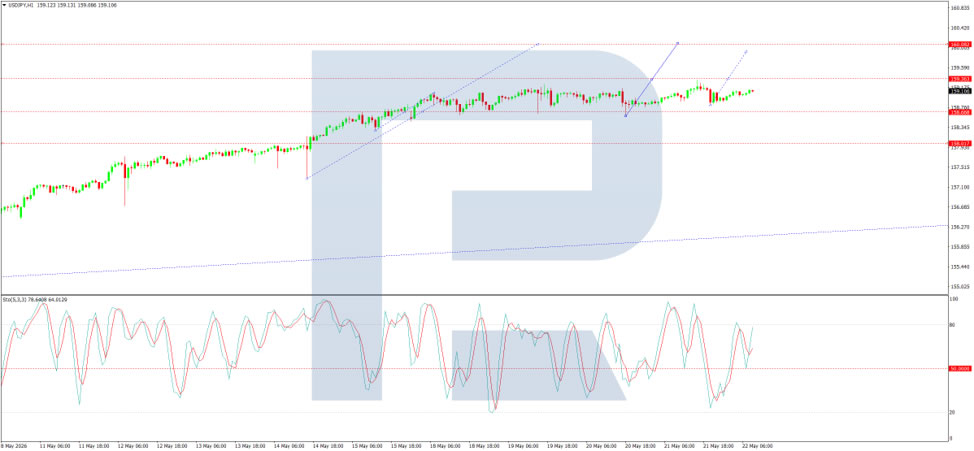

On the H4 chart, USD/JPY is trading within a consolidation range around 158.68 and is moving higher towards 160.09. A test of this level is likely, followed by a possible pullback to 158.66, with scope for a further decline towards 157.00. The MACD indicator supports this scenario, with its signal line above zero and pointing firmly upwards, indicating continued bullish momentum.

USD/JPY is set to close its second consecutive week higher as the yen remains under pressure from softer-than-expected Japanese inflation data. Core inflation slowed to a four-year low of 1.4%, falling further below the BOJ’s 2% target and dampening expectations for near-term policy tightening. This contrasts with the BOJ’s upgraded inflation forecast of 2.8%, driven by energy costs related to the Middle East conflict. With the pair hovering near the critical 160 level, where Japanese authorities intervened in late April and early May, markets remain on high alert for potential intervention. Prime Minister Takaichi’s consideration of an additional budget to address energy prices adds another layer of complexity. Technically, further upside towards 160.09 appears likely in the near term.

Conclusion

GBP/USD stabilised following weaker-than-expected UK inflation data, easing concerns about aggressive Bank of England rate hikes. However, the pound faces headwinds from a soft labour market and rising oil prices, suggesting that any recovery may be short-lived. Technical indicators point to a near-term correction before a potential continuation of the broader trend.