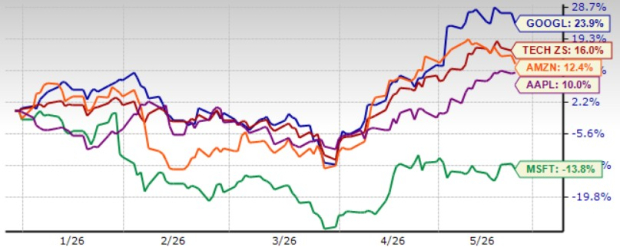

Alphabet GOOGL shares closed at $387.66 on Tuesday, near the 52-week high of $408.61 GOOGL shares hit on May 18. Year to date (YTD), the company’s shares have surged 23.9%, outperforming the Zacks Computer & Technology sector’s return of 16%. GOOGL’s prospects are benefiting from its growing AI-powered Search capabilities and significant investments in Cloud computing.

However, capacity constraints, despite the improving pace of server deployments and data center construction, are expected to hurt Alphabet’s prospects in 2026. This, along with higher depreciation expenses and related data center operations costs, including energy, is expected to hurt profitability. Moreover, the Wiz acquisition is expected to have a low single-digit percentage point headwind to Google Cloud’s operating margin for the remainder of 2026. So, what should investors do with GOOGL shares?

GOOGL Suffers From Stiff Competition & Higher Capex

Alphabet is facing stiff competition in the cloud computing space from Microsoft MSFT and Amazon AMZN. According to Synergy Research Group’s first-quarter 2026 data, Amazon maintained a strong lead in the market, though Microsoft and Alphabet’s Google continued to achieve substantially higher growth rates. Amazon, Microsoft and Alphabet’s market share were roughly 28%, 21% and 14%, respectively. In the search domain, Google continues to dominate with a roughly 90.02% share, followed by Microsoft’s Bing, with a 5.14% share, per the latest data from StatCounter. In the consumer technology market, Alphabet continues to face stiff competition from Apple AAPL.

Investor skepticism over GOOGL’s ability to monetize its AI-infused services, given the huge capital expenditure guidance, which is now pegged between $180 billion and $190 billion for 2026, has been a headwind. Most of this spending is marked for building AI and cloud infrastructure, including data centers, chips and servers for Gemini and cloud growth. Although Alphabet generates considerable cash flow ($174.4 billion on a trailing 12-month basis at the end of first-quarter 2026), this steep increase in capital expenditure is expected to squeeze free cash flow ($64.4 billion on a trailing 12-month basis at the end of first-quarter 2026). GOOGL expects 2027 capital expenditure to significantly increase compared to 2026.

GOOGL shares have outperformed peers, including Amazon, Apple and Microsoft, YTD. Shares of Apple and Amazon have returned 10% and 12.4%, respectively, while Microsoft has dropped 13.8%.

GOOGL Stock’s Price Performance

Image Source: Zacks Investment Research

Alphabet Shares Are Overvalued

GOOGL shares are overvalued, as suggested by a Value Score of D. The Alphabet stock is trading at a forward 12-month price/earnings (P/E) of 26.81X compared with the broader sector’s 25.48X.

Alphabet shares are trading at a premium compared with Microsoft, shares of which are trading at a P/E multiple of 21.89. However, GOOGL shares are trading at a lower multiple compared with Apple’s 32.31 and Amazon’s 27.9.

GOOGL Stock’s Valuation

Image Source: Zacks Investment Research

AI Push Boosts GOOGL’s Search Business

Alphabet has been actively embedding AI, especially within Search, to enhance user experience, provide better AI-focused features and consequently improve ad performance. Features such as AI Overviews and AI Mode are increasing both user engagement and overall query volume. Management noted that search queries are at an “all-time high,” with users returning more frequently because of these AI-enhanced experiences. GOOGL is also expanding Personal Intelligence, which delivers more personalized search responses based on user context. Google believes this makes search more useful for complex and conversational queries.

Alphabet is embedding Gemini models across its advertising infrastructure to improve ad relevance and monetization. AI is strengthening Search monetization by improving ad quality and targeting, AI-powered advertiser tools such as AI Max and Performance Max, as well as new ad formats inside AI Mode. Google is positioning Search as a platform for agentic shopping experiences through the new Universal Commerce Protocol (UCP) and integrations with retailers such as Sephora and Ulta Beauty. Users can discover products, compare options, and complete purchases directly within AI Mode and Gemini experiences.

Faster and more efficient Search infrastructure is driving GOOGL’s Search market share. Google stated it has reduced search latency by more than 35% over the past five years, even while adding AI-intensive features. The company also reduced the cost of core AI responses by more than 30% after upgrading AI Overviews and AI Mode to Gemini 3, benefiting from hardware and engineering improvements.

Alphabet emphasized that it is aggressively strengthening its cloud computing business by expanding AI infrastructure, deepening enterprise adoption, improving profitability, and differentiating itself through a full-stack AI strategy. GOOGL’s broad portfolio of Custom TPUs, Axion CPUs, and NVIDIA GPUs, including Blackwell, Hopper, and upcoming Vera Rubin systems, is expanding its clientele. Google launched several new enterprise AI tools at Cloud Next, including the Gemini Enterprise Agent Platform, which allows businesses to build and manage AI agents securely at scale. Gemini Enterprise’s paid monthly active users grew 40% quarter-over-quarter in the first quarter of 2026. Google also signed multiple $1 billion-plus cloud contracts, reflecting an expanding clientele.

2026 Earnings Estimate Revisions Rise for GOOGL Stock

The Zacks Consensus Estimate for 2026 earnings is pegged at $14.29 per share, up 22.1% over the past 30 days, indicating 32.2% year-over-year growth. The consensus mark for 2026 revenues is pegged at $422.05 billion, indicating 23.1% year-over-year growth.

Alphabet Inc. Price and Consensus

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

The consensus mark for second-quarter 2026 earnings is pegged at $2.85 per share, up by a nickel over the past 30 days, suggesting a 23.4% growth year over year. The Zacks Consensus Estimate for second-quarter 2026 revenues is pegged at $101 billion, implying 23.6% year-over-year growth.

Conclusion

Alphabet is benefiting from accelerated growth across AI infrastructure, Google Cloud and Search. However, stiff competition in cloud computing and higher capex have been concerning. GOOGL’s stretched valuation is a concern.

Alphabet currently has a Zacks Rank #3 (Hold), suggesting that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.