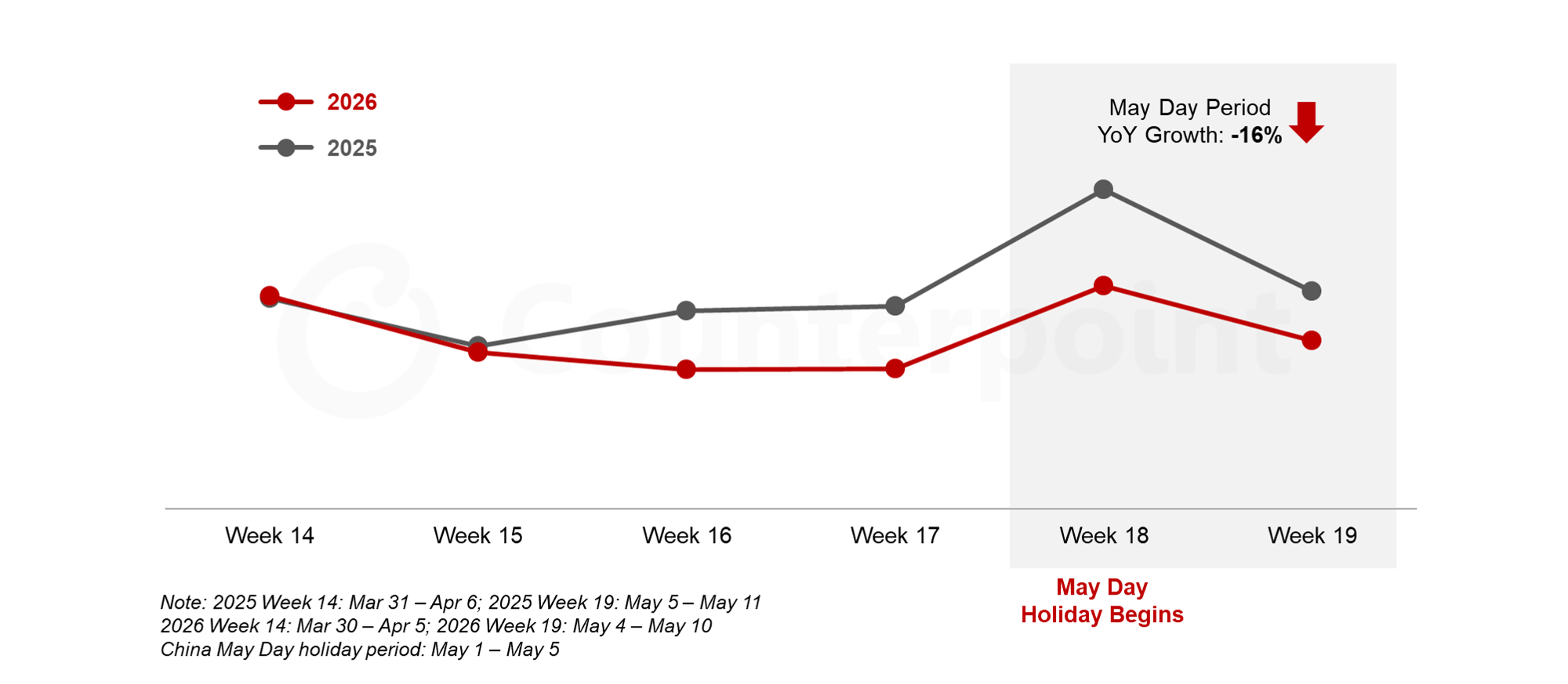

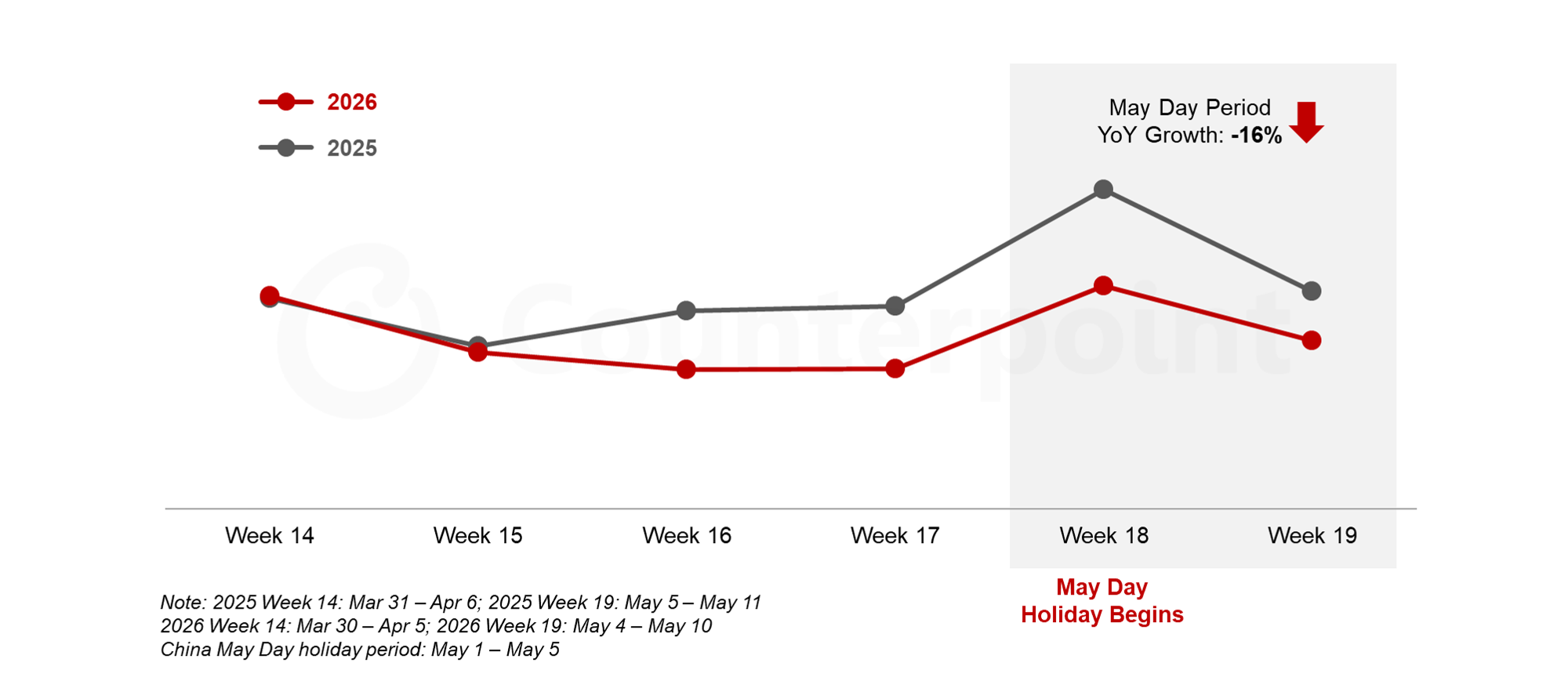

China’s smartphone sales fell 16% YoY during the two weeks surrounding the 2026 May Day holiday, (includes week 18 and week 19), mainly due to memory price increases driving higher smartphone prices and suppressing consumer upgrade demand, according to Counterpoint Research’s China Weekly Smartphone Sell-Out Tracker. Additionally, promotional intensity during the holiday was weaker than in previous years, as OEMs placed greater emphasis on profitability than simply pursuing sales volume.

China smartphone weekly sales, week 14 – week 19, 2025 vs 2026

Huawei continued to lead the China smartphone market. The Enjoy 90 Pro Max delivered significantly strong performance, driven by its exceptional battery life and strong value-for-money positioning. Combined with its stable pricing strategy, Huawei has maintained a weekly sales market share of above 25% since April. Additionally, strong sales of the Pura 90 Pro series and the foldable Pura X Max, which officially went on sale at the end of April, further reinforced Huawei’s leading position during the May Day holiday period. While competitors have raised prices under mounting cost pressure, Huawei continued to offer promotions on older models such as the Nova 15 and Mate 80 series, underscoring its domestic supply chain advantage and supporting further market share gains.

Apple is going through seasonality with competitors offering stronger new launches in April. The iPhone 17 lineup entering a more normalized demand phase following a robust six-month run. Apple had a decent Q1 in China. Domestic brands were forced to raise prices due to the memory cost pressure, which made the iPhone look more competitive by comparison, and the subsidy helped at the base level.

Other Chinese brands launched new models in late April and rolled out promotional campaigns, helping them boost sales momentum during the May Day period. However, Chinese Android OEMs have raised prices on legacy models by an average of 13% amid rising component costs, which is likely to further soften market demand in the near term. A modest sequential recovery is expected in early June, supported by the 618 shopping promotions. As the memory-related cost pressure continues to tighten, China’s smartphone shipments are expected to decline 9% YoY in 2026, but it will still outperform the global average. Counterpoint Research