China’s manufacturing clout, access to cheap energy and robust IPO pipeline are giving it the edge in sectors like AI and robotics—and luring back Western LPs, say market participants.

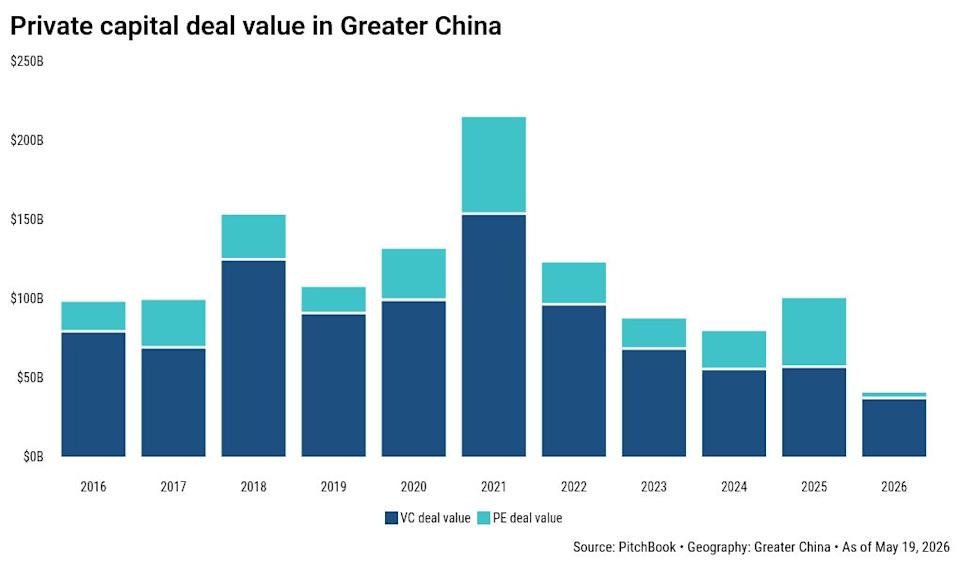

Greater China’s private markets have seen four straight years of fundraising decline, buffeted by both US tensions and weak domestic consumption. More recently, supply chain shocks resulting from the Iran war have continued to weigh heavily on the minds of investors.

However, many investors speaking at the Hong Kong Venture Capital Association’s Greater China Private Equity Summit on Tuesday said China’s private markets are already bottoming out.

“I do observe very clearly that sentiment is improving from a Western LP perspective. … If you look across the world, Chinese private equity still churned about 14% net returns, which isn’t bad compared to various indices including the MSCI. That’s an outperformance of at least 200-400 basis points,” said Brooke Zhou, who co-leads Swiss-headquartered asset manager LGT Capital Partners’ APAC business in Hong Kong.

While China continues to face most of the same geopolitical and regulatory risks as before, it shows a commanding edge in specific areas, especially those sitting at AI’s intersections with hardware, infrastructure and applications, noted investors.

China’s existing strengths in hardware manufacturing mean its AI companies can go beyond the algorithm layer to create full-stack solutions that can be executed at an industry level. It also has the ability to export electricity cheaply, which gives it a unique competitive edge, explained Jing Hong, founding partner at growth stage investor Gaocheng Capital.

“China is already exporting low-cost electricity in the form of tokens. Ultimately, the LLM model relies on chips, energy, and which country can provide the lowest-cost token. China has double the electricity productivity than the US, but at a 50% lower cost per kilowatt,” she said.

While US-based AI companies like OpenAI and Anthropic are still pursuing superintelligence and unprecedented growth, Chinese players like DeepSeek are more urgently chasing financial goals, including returns and operational efficiency.

GPs have already been putting money to work again. According to a recent PitchBook analyst note on China’s AI market, AI deal value recovered to more than $10 billion in 2025 after bottoming out at $7.8 billion in 2023. It accounted for 19.6% of total VC deal value last year—even as overall activity remains well below the 2021 peak of $23.3 billion.

Investors expect Chinese AI investments to remain resilient.