Advanced Micro Devices (AMD 5.67%) has always seemed to be a second-place company, no matter what computing era it was in. Currently, it’s well behind Nvidia (NVDA 4.39%) in artificial intelligence (AI) computing, and is being dramatically outperformed in nearly every growth category. This echoes what Intel did to AMD in the early 2000s.

But even though AMD isn’t winning as much as these two did in their respective eras, it doesn’t mean that AMD can’t be a solid investment in its own right for the right price. So, is AMD a top AI stock to buy now? Let’s take a look.

Image source: Getty Images.

AMD’s business is more diversified than its peers

Some computing companies only focus on one type of component to maximize their efficiency in that area; that’s not AMD. AMD offers a wide variety of hardware, ranging from data center GPUs to OEM (original equipment manufacturer) CPUs to embedded processors. This gives AMD exposure to several parts of the computing ecosystem, which spreads out risk. However, when one segment of computing is doing much better than others (like data centers), this diversification hurts the company in terms of growth. Some investors may prefer that, as the pain won’t be as great if AI demand falls off a cliff.

Today’s Change

(-5.67%) $-25.51

Current Price

$424.19

Key Data Points

Market Cap

$692B

Day’s Range

$423.44 – $438.99

52wk Range

$107.67 – $469.21

Volume

1.1M

Avg Vol

39M

Gross Margin

47.09%

AMD’s latest quarter was solid. The data center segment did great, with revenue rising 57% year over year. Its client and gaming and embedded processors segments didn’t do as well, but still posted respectable growth of 23% and 6%, respectively. The market loved the quarter, and the stock is up over 25% since AMD reported earnings on May 5.

But after a run-up like that, is the stock still worth buying? With how quickly AMD is growing, I think the best way to assess the stock is to look at the forward price-to-earnings ratio.

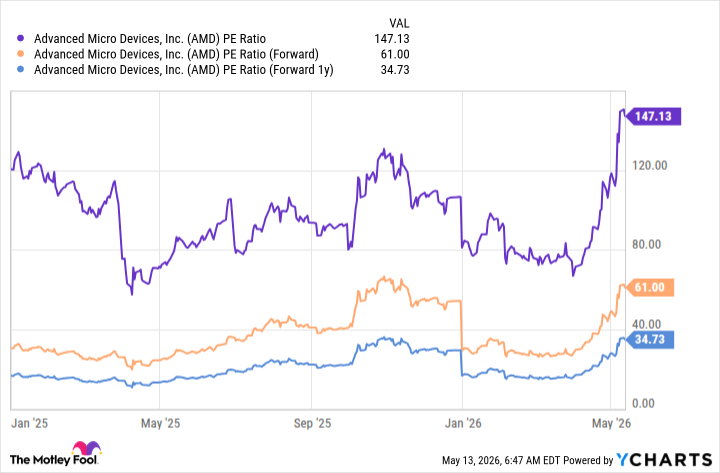

AMD PE Ratio data by YCharts

With the stock trading at 147 times trailing earnings and 61 times forward earnings, Wall Street analysts project that AMD’s earnings will more than double this year, highlighting its strong expected growth over the next year and assuming it will solve some profitability issues that plagued it last year. However, at 35 times 2027’s earnings, the stock is a long way from cheap.

While I won’t deny AMD had a strong Q1, why would you invest in it when the industry leader, Nvidia, trades for 26 times forward earnings and is growing faster? Nvidia is far cheaper than AMD and represents an overall better value.

So, while AMD may be succeeding in its AI endeavors, Nvidia is still the king. I think investors are better off investing in the market leader, rather than the more expensive second-place company.