Key Points

-

Tesla remains one of the largest manufacturers of electric vehicles, but the brand is struggling amid a highly competitive landscape.

-

Chief executive Elon Musk has shifted the company’s focus to other products, such as the Cybercab robotaxi and the Optimus humanoid robot.

-

These product platforms present a much larger opportunity than the passenger EV business, but that doesn’t mean investors should buy Tesla stock today.

- These 10 stocks could mint the next wave of millionaires ›

Tesla (NASDAQ: TSLA) is one of the world’s largest manufacturers of passenger electric vehicles (EVs), but the brand has struggled with sluggish sales over the past several quarters amid rising competition. As a result, CEO Elon Musk is pivoting the company’s focus to new product platforms, such as the Cybercab autonomous robotaxi and the Optimus humanoid robot.

During his conference call with investors recapping Tesla’s operating results for the first quarter of 2026 (ended March 31), Musk delivered a stream of good news regarding the Cybercab and Optimus. However, it didn’t arrest the decline in Tesla stock, which is now down 23% from its December record high.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Unfortunately, the stock might struggle to recover from here because of its sky-high valuation. Here’s what could be in store for investors.

Image source: Tesla.

The Cybercab is in production, and Optimus is close

Elon Musk believes self-driving cars are the future of mobility, so he’s making a huge bet on Tesla’s Cybercab robotaxi, which doesn’t have pedals or even a steering wheel. It will run on the company’s Full Self-Driving (FSD) software, autonomously hauling passengers and even small commercial loads around the clock.

This could unlock a new, high-margin revenue stream for Tesla, potentially offsetting the company’s declining passenger EV sales. During his April 22 conference call with investors, Musk said the Cybercab is officially in production, and he expects volumes to ramp up exponentially by the end of 2026.

But there is a catch. The unsupervised version of Tesla’s FSD software is approved for use only in Austin, Texas, right now, which means the Cybercab can’t hit the road in any meaningful capacity. Musk hopes unsupervised FSD will win regulatory approval in around a dozen U.S. states by the end of this year, but that suggests robotaxi revenues will be relatively small until 2027, and potentially even later.

But Tesla has an even bigger opportunity in the pipeline: the Optimus robot. Musk claims it will have versatile use cases in households and businesses alike, so its addressable market could be enormous. A couple of years ago, Musk even predicted that humanoid robots would outnumber humans by 2040, which highlights the scale of this opportunity.

Tesla could reveal its latest robot, Optimus V3, in the middle of this year, and the company is currently preparing its Fremont, California, factory to handle mass production. Volumes will be light in 2026, but Musk expects them to ramp up in 2027 and beyond.

We can’t ignore Tesla’s struggling passenger EV business

Tesla delivered 1.79 million passenger EVs in 2024, which was a 1% decline from the previous year. It then delivered 1.63 million cars in 2025, which was down by an even steeper 9%. This led to sharp declines in the company’s revenue and earnings last year.

Fortunately, Tesla is off to a better start to 2026. Its EV deliveries rose 6% in the first quarter, contributing to a 16% increase in revenue and a modest 8% increase in earnings per share. While those are all good signs, further growth might be patchy given the competitive landscape.

Last year, China-based BYD (OTC: BYDDY) outsold Tesla globally for the first time, as its ultra-low-cost EVs resonate with consumers who are increasingly budget-conscious. It’s capturing a massive share of emerging EV markets like Australia, where it recently outsold Tesla 10-to-1 in January alone.

Tesla planned to launch a low-cost EV of its own, the Model 2, but Musk put it on the back burner to focus on the Cybercab and Optimus. This might be the right long-term move, but those products are still a long way from generating meaningful sales, which could leave a hole in Tesla’s financial results over the next couple of years unless it finds a way to be more competitive in the passenger EV space.

Tesla stock could face further downside

Investors might think the recent 23% decline in Tesla stock doesn’t reflect the positive progress of the Cybercab and Optimus, but valuation matters.

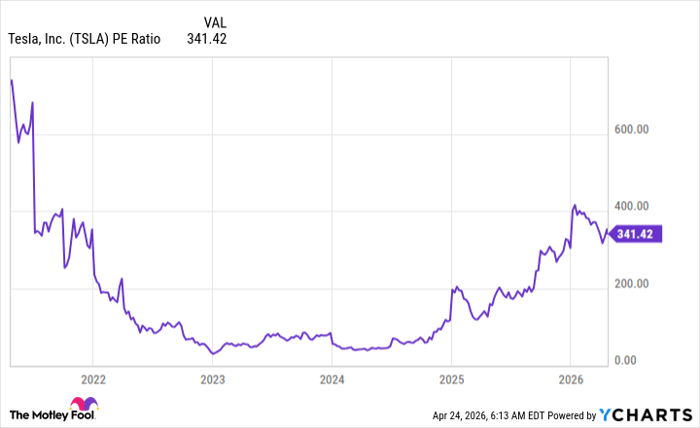

Based on the company’s trailing-12-month earnings of $1.09 per share, its stock is trading at a sky-high price-to-earnings (P/E) ratio of 341, which is 10 times the Nasdaq-100 technology index’s P/E. To put it another way, Tesla looks extremely overvalued relative to its big-tech peers.

Data by YCharts.

Most value investors would avoid Tesla stock like the plague at its current P/E, especially because of the real possibility of further weakness in the EV business, which still accounts for over 70% of the company’s total revenue. As a result, until products like the Cybercab and Optimus scale up, the path of least resistance might be to the downside for Tesla stock.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $540,224!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $51,615!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $498,522!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of April 27, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends BYD Company. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.