Exploring Three Promising European Small Caps With Strong Potential

Uncategorized

Exploring Three Promising European Small Caps With Strong Potential

08 mins

As European markets experience a positive uptick, with the STOXX Europe 600 Index rising by 1.91% amid optimistic corporate earnings and geopolitical de-escalation, investors are increasingly looking towards small-cap stocks for potential opportunities. In this environment, identifying promising small-cap companies often involves evaluating their innovative capabilities, market positioning, and resilience in the face of broader economic shifts.

Below we spotlight a couple of our favorites from our exclusive screener.

Simply Wall St Value Rating: ★★★★★★

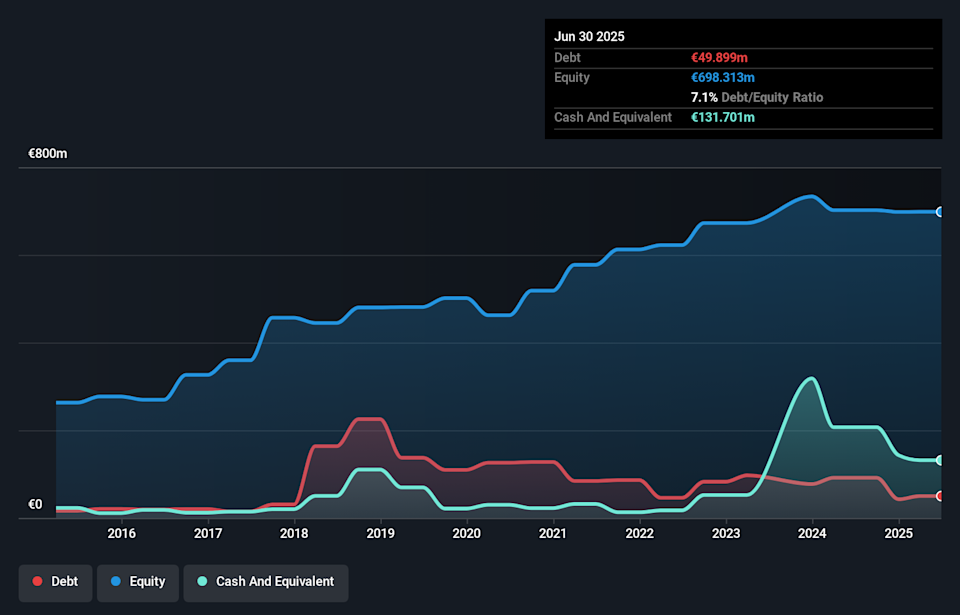

Overview: IDI is a private equity firm that focuses on leveraged buyouts, expansion capital, and acquiring significant holdings in small to medium-sized listed companies, with a market cap of €512.25 million.

Operations: IDI generates revenue through its private equity investments, which include leveraged buyouts and expansion capital in small to medium-sized listed companies. The firm focuses on acquiring significant holdings and engaging in various financial strategies such as mezzanine financing and pre-IPO co-investments.

IDI, a small player in the European market, is trading at 28.3% below its estimated fair value, offering an intriguing opportunity. The company has demonstrated impressive earnings growth of 201.3% over the past year, significantly outpacing the industry average of 3%. With a debt-to-equity ratio reduced from 24.6% to 7.1% over five years and interest payments well-covered by EBIT at a ratio of 4.4x, IDI seems financially robust. Recently announcing an annual dividend of €2.90 per share and reporting net income growth to €59 million from €19.6 million last year further highlights its potential for continued success in the capital markets sector.

ENXTPA:IDIP Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★☆☆

Overview: Finnair Oyj is an airline company that operates across North Atlantic, Asia, Europe, the Middle East, and internationally with a market capitalization of €632.99 million.

Operations: Finnair Oyj generates revenue primarily from passenger and cargo services across its international routes. The company faces significant costs related to fuel, personnel, and aircraft maintenance, which impact its profitability. Its net profit margin has shown variability over recent periods.

Finnair Oyj is navigating its path with strategic fleet renewals and capacity expansion. The airline’s debt to equity ratio has seen a favorable shift from 147.3% to 109.1% over five years, indicating improved financial health, although its net debt to equity remains high at 52.7%. Recent earnings have been bolstered by a significant one-off gain of €22.7M, contributing to an impressive earnings growth of 272.7% last year, far outpacing the industry average of 22.3%. Despite challenges like volatile share prices and interest coverage concerns (1.5x EBIT), Finnair’s focus on operational efficiency and ancillary sales growth positions it well for future demand increases, particularly with plans for a 10% ASK boost by 2025 and potential cost savings from resumed Russian airspace access.

HLSE:FIA1S Earnings and Revenue Growth as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: Selena FM S.A. operates through its subsidiaries to manufacture and distribute construction chemicals and general construction accessories across the European Union, Eastern Europe, Asia, North America, and South America, with a market capitalization of PLN1.13 billion.

Operations: Selena FM’s primary revenue streams include the Parent Company (PLN854.23 million), Production in Poland (PLN676.63 million), and Eastern Europe and Asia (PLN520.61 million).

Selena FM, a nimble player in the chemicals sector, has demonstrated impressive earnings growth of 91.9% over the past year, outpacing its industry peers who saw an 11.9% drop. Despite a net debt to equity ratio rising from 13.4% to 30.6% over five years, it remains satisfactory at 17.7%. Trading at a discount of 30.4% below estimated fair value suggests potential upside for investors seeking undervalued opportunities in Europe’s market landscape. The company’s high-quality earnings and well-covered interest payments (7.4x EBIT) underscore its financial resilience amidst evolving industry dynamics and economic conditions.

WSE:SEL Earnings and Revenue Growth as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ENXTPA:IDIP HLSE:FIA1S and WSE:SEL.