During times of global turmoil like the Iran war, some investors might be tempted to say to themselves, “The world feels a little scary right now — I think I’ll sell some stocks and wait until the market calms down to buy more.” Or: “Now feels like a bad time to invest in stocks. I’ll pause my 401(k) contributions until the Iran war settles down and stocks get cheaper.”

Those ideas are all too common, all too human, and, unfortunately, often all too wrong. When people start to try to predict the future by deciding that “now is a bad time to buy stocks” or “later will be a better time to buy stocks,” they’re doing something called “timing the market.”

And no one knows how to time the market. No one knows for sure that today, or next week, or three months from now is a “good time” or “bad time” to buy stocks. No one knows what will happen to the stock market tomorrow, or next year, or in 10 years.

Image source: Getty Images.

Instead of timing the market, most people are better off focusing on “time in the market” — buying and holding stocks for as long as possible, through short-term ups and downs, in the hope of eventually earning long-term gains.

In general, timing the market is a bad move for your money. The recent stock market volatility from the Iran war shows this classic investing concept in action.

Here are a few lessons that show the value of time in the market, not timing the market.

1. The best days for stocks often happen near the worst days

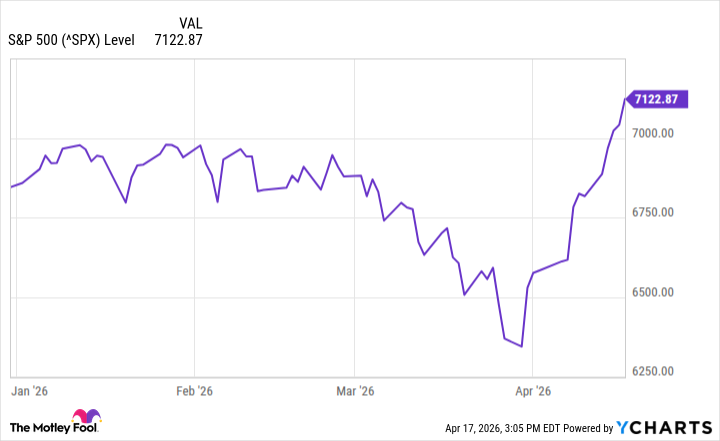

Feb. 27 was the last trading day for U.S. markets before the Iran war started on Feb. 28. Between Feb. 27 and March 30, the S&P 500 index lost almost 8% of its value.

During those weeks, the headlines were often dire, the news felt chaotic, there were terrible videos of people suffering, buildings on fire, and energy infrastructure getting blown up by drones. Many investors might have felt tempted to panic and sell their stocks.

But the stock market has really good days, too. And sometimes the biggest gains happen right after big downturns. According to Vanguard research, based on S&P 500 index performance from Jan. 1, 1980, through Dec. 31, 2024, 10 of the best 20 days of the S&P 500 performance happened during years when the market had negative total returns. And 11 of the worst 20 days for the S&P 500 happened during years when the stock market had positive total returns.

The point is: Even a “bad day” for the S&P 500 can happen during what turns out to be a “good year” for stock investors. Recent experience shows this to be true. In the past few weeks since hitting that March 30 low, the S&P 500 has gained more than 12%. Between March 30 and April 13, the market recovered to its pre-war price level. On Friday, the S&P 500 closed at a new all-time high.

How do you know which of those days during the Iran war was the best time to sell stocks, or the right time to buy stocks? No one knows. The market can move faster than you can decide.

2. Getting out is easy, getting back in is hard

Hindsight is always 20/20. Looking back on it now, Feb. 27, the day before the start of the Iran war, might have looked like a good time to sell stocks and get out of the market. Let’s say you had a crystal ball, and you knew that the U.S. was about to start airstrikes on Iran the following day. You sold all your stocks on Feb. 27 and moved the money into cash.

How do you know when it’s the “right time” to buy stocks again? You might buy “too soon” and get hit by more short-term declines, or you might buy “too late” after stock prices have already bounced back and become more expensive.

If people allow themselves to be scared out of the market by the latest news headlines, that behavior becomes hard to correct. If you’re scared enough to sell, you might not feel brave enough to buy back into the stock market anytime soon. Missing out on future stock market gains can be more costly to your wealth than a few short-term downturns.

3. Stock prices move faster than news headlines

Stocks can recover faster than the news headlines. Even if it doesn’t feel like a geopolitical crisis or economic downturn is truly “over,” stock prices might have already started to go back up. The stock market focuses on the future. If you wait for good news before you buy stocks, you might be too late — and miss out on big gains.

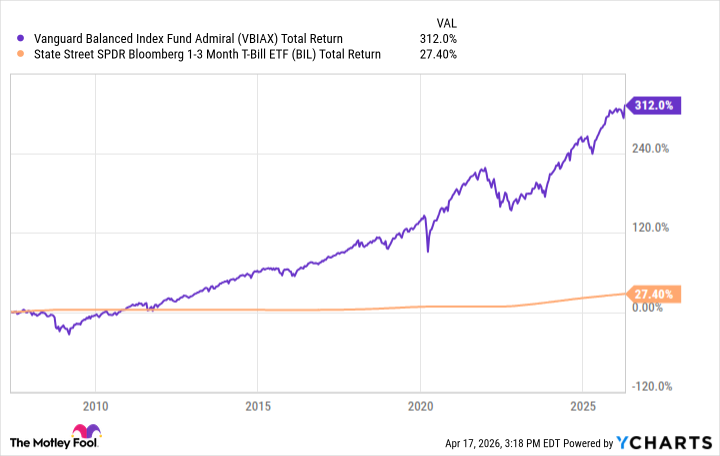

Vanguard research also shows that when people sell stocks and move to cash, they tend to underperform a portfolio of 60% stocks and 40% bonds (this is described as a 60/40 portfolio). And the longer you stay in cash, the worse your money might perform compared to just staying invested in the market.

From Jan. 1, 1980, to Dec. 31, 2024, investors who moved to cash for three months would have underperformed the 60/40 portfolio by an average of 4.1%. Investors who stayed in cash for six months underperformed by an average of 7.4%. And investors who stayed in cash for 12 months had an average underperformance of 13.3%.

Based on past performance of the Vanguard Balanced Index Fund (VBIAX +0.10%) (which holds a 60/40 portfolio) and the State Street SPDR Bloomberg 1-3 Month T-Bill ETF (BIL +0.03%) (which is a cash-equivalent investment), here’s what can happen to your money if you stay in cash for the long run:

VBIAX Total Return Level data by YCharts

Most investors can’t afford to try to out-think the stock market. If your money is intended for long-term goals like retirement, you need to try to leave it invested. Keep investing consistently with dollar-cost averaging and a buy-and-hold mindset. Staying invested for a longer time in the market is likely a better strategy for most people than trying to predict the future by timing the market.