①Geopolitical sentiment cools, the Hang Seng Index gains and then loses the 26,000-point level; what are the characteristics of the short-term market? ②The market refocuses on high-elasticity assets; which sectors are favored by capital?

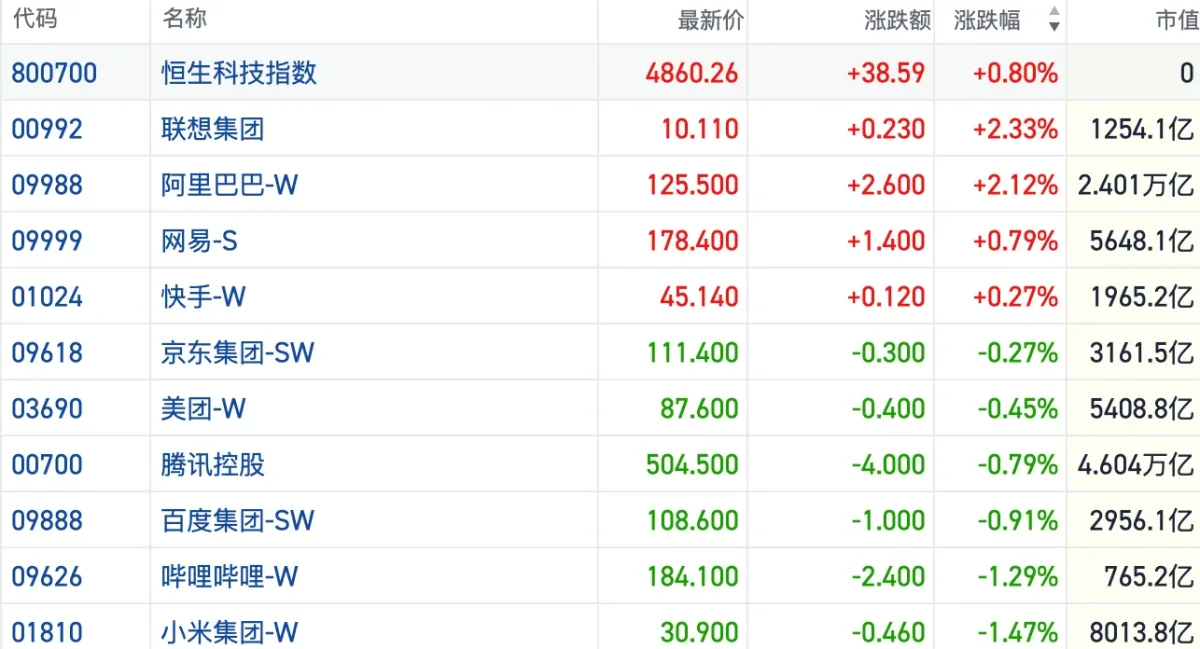

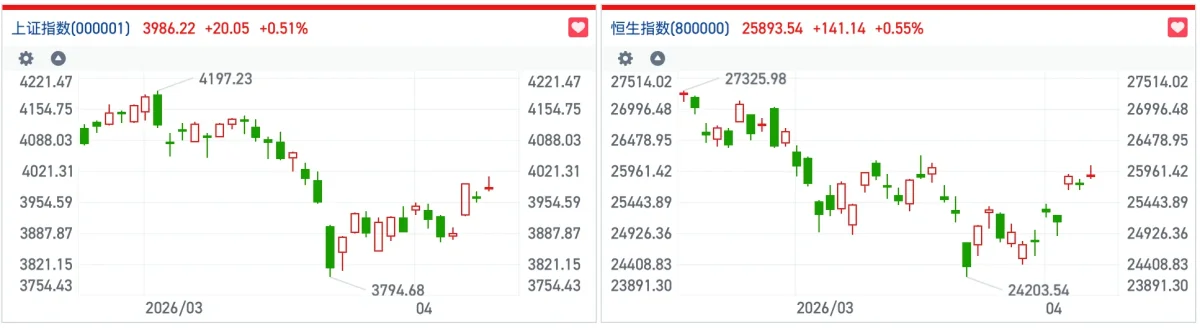

Cailian Press, April 10 (Editor: Feng Yi) As geopolitical sentiment further eased, the Hong Kong stock market became active again today. By the close, the Hang Seng Index rose 0.55%, the Hang Seng China Enterprises Index gained 0.5%, and the Hang Seng Tech Index increased by 0.8%.

[Market Sentiment Recovers but Remains Cautious; Hang Seng Index Gains and Then Loses 26,000 Points]

On the trading board, large tech companies showed mixed performance. Alibaba surged over 2%, while NetEase and Kuaishou closed positively. Xiaomi fell by 1.47%, and Baidu, Tencent, and Meituan experienced slight declines.

In other areas, Chinese brokerage stocks performed strongly today. CITIC Securities led with a 12% surge on better-than-expected earnings. Additionally, the AI sector remained robust, with semiconductor and storage concepts rotating higher, and Gigadevice Innovations soaring more than 12%. Moreover, lithium batteries, energy storage, automobiles, real estate, and shipping industries all strengthened.

Among declining sectors, papermaking and non-ferrous metals were weak. Energy stocks such as oil and coal retreated, and gold stocks were relatively subdued.

Overall, with the U.S. and Iran entering negotiations, Hong Kong’s stock market extended its generally warm trend this week in the short term.

Today, the Hang Seng Index closed slightly higher, but turnover for the day reached HKD 246.317 billion, and the 26,000-point level was gained and then lost. It is not difficult to see that uncertainties from geopolitical risks continue to weigh on bullish sentiment.

On the short-selling side, the total short-selling amount was HKD 31.445 billion, accounting for 12.77% of the Hang Seng Index’s turnover, with the short-selling ratio falling again in the short term.

Tencent, Xiaomi Group-W, and Alibaba-W ranked among the top three in short-selling amounts, at HKD 1.571 billion, HKD 1.343 billion, and HKD 1.326 billion, respectively.

[Geopolitical Risks Ease, Major Sectors See Mixed Gains with Growth and High-Elasticity Assets Favored]

In terms of market performance, most popular sectors today saw mixed gains, with capital shifting again from safe-haven assets to high-elasticity ones.

Among them, sectors with robust fundamentals such as energy storage, lithium batteries, securities firms, and automobiles led short-term gains. According to a spokesperson for the Ministry of Commerce’s Foreign Trade Department, year-to-date exports of electric vehicles, lithium batteries, and photovoltaic products—the ‘new trio’—have grown by 50.7%, becoming a key driver of foreign trade expansion.

On the other hand, geopolitical tensions continue to ease.

According to reports, Iranian Deputy Foreign Minister Ravanchi stated at a meeting attended by foreign diplomats and international organization representatives in Iran on the 10th that consensus has been reached, and Iran’s ten-point plan will serve as the basis for negotiations. Meanwhile, U.S. Vice President Vance noted that U.S. President Trump has provided clear guidelines for negotiations, expressing expectations for talks on the Iran issue and confidence in achieving positive outcomes.

Notably, positive developments have also emerged in macroeconomic fundamentals. Data released today by the National Bureau of Statistics showed that the CPI rose 1.0% year-on-year in March, while the PPI turned from a decline to an increase.

Guosen Securities analyzed that after short-term disruptions, consumer demand is steadily recovering, with neither service nor goods consumption showing a cliff-like drop, indicating sustainable domestic demand recovery.

[A-Share Market Sees Rotating Hotspots and Rising Volume; Analysts Caution Against Short-Term Overexposure]

Additionally, trading volume surged again today in A-shares, with the ChiNext Index surging over 4% intraday, breaking previous highs and reaching its highest level since December 2021. The total turnover of the Shanghai and Shenzhen markets reached 2.32 trillion yuan, up 188.8 billion yuan compared to the previous trading day. On the market, hotspots rotated quickly, with more than 3,900 stocks rising across the entire market.

Looking ahead, Guozheng International noted that oil price fluctuations driven by geopolitical factors have led to ongoing swings in market expectations regarding inflation and the Fed’s interest rate policy. Coupled with the unpredictable nature of geopolitical developments, asset price volatility remains relatively high in the short term. Investors are advised to exercise caution when pursuing high-risk assets and maintain defensive positioning strategically.