Market Snapshot

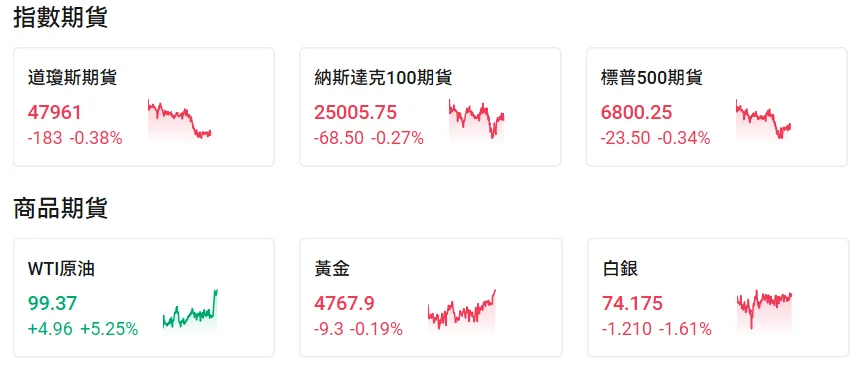

Before the market opened on Wednesday, Nasdaq 100 futures fell by 0.27%, S&P 500 futures dropped by 0.34%, Dow futures declined by 0.38%, U.S. crude oil rose by 5.25%, and spot gold decreased by 0.19%.

Following the temporary ceasefire agreement, U.S. President Trump issued a strongly worded public warning to Iran via social media platforms. He explicitly stated that the current ceasefire was only a phased outcome, and the U.S. military’s large carrier strike groups, fighter jet squadrons, and ground forces would remain in their current combat-ready deployments without withdrawing from areas surrounding Iran. Trump emphasized that if Iran failed to fully implement the consensus reached in the peace agreement or adopted delaying tactics during negotiations, the U.S. would immediately resume military strikes. The scale and intensity of such a conflict would far exceed the previous “Epic Wrath Operation” and could even escalate into an unprecedented full-scale war.

$Star Tech Companies (LIST2518.US)$ The pre-market session saw fluctuations: Meta gained 0.64%, Netflix rose by 0.31%, and Apple fell by 0.24%.

$China Concept Stocks (LIST2517.US)$ Pre-market volatility continued as Nio surged over 3%, New Oriental Education rose more than 2%, and Kingsoft Cloud advanced nearly 2%.

$China Concept Stocks (LIST2517.US)$ Pre-market volatility continued as Nio surged over 3%, New Oriental Education rose more than 2%, and Kingsoft Cloud advanced nearly 2%.

Individual Stock News

-

CoreWeave signed a $21 billion AI infrastructure agreement with Meta Platforms, locking in AI cloud computing capacity until 2032. The stock initially surged but later pulled back in pre-market trading.

$CoreWeave (CRWV.US)$ followed by $Meta Platforms (META.US)$ The largest-ever AI cloud computing cooperation agreement was reached, highlighting the strong demand for high-performance AI computing power among enterprises.

Meta Platforms will expand its inference workloads through CoreWeave’s AI cloud platform. On April 9, 2026, both parties announced the upgrade of their existing partnership into a long-term agreement valued at approximately $21 billion, extending services until December 2032.

This agreement represents a significant business milestone for CoreWeave since its listing on Nasdaq in March of last year, further solidifying its position as a core supplier of AI infrastructure. It also provides robust support for the large-scale commercial deployment of NVIDIA’s next-generation Vera Rubin platform.

CoreWeave has proposed the issuance of $3 billion in convertible senior notes.

-

Stock prices fall back to a decade ago! Reports suggest that Disney’s new CEO is taking immediate action upon assuming office, with plans to cut 1,000 jobs.

According to reports,$Disney (DIS.US)$ Is preparing for large-scale layoffs, one of the first major initiatives by the new CEO, Josh D’Amaro. According to insiders, the entertainment company plans to cut up to 1,000 jobs in the coming weeks, with layoffs primarily concentrated in the marketing department following recent corporate restructuring.

The report states that, like many Hollywood studios, Disney has been striving to adapt to declining profitability in the streaming business while also addressing falling box office revenues and fierce competition from tech companies such as Amazon and YouTube, owned by Google. Additionally, Disney is working to free up funds to invest in its digital operations, which it considers to have growth potential.

According to reports, since Bob Iger, D’Amaro’s predecessor, returned as Disney’s CEO in 2022 and initiated a large-scale reorganization, the company has laid off more than 8,000 employees. Insiders revealed that the upcoming round of layoffs had been planned even before D’Amaro took office.

$Tesla (TSLA.US)$ Tesla is secretly advancing plans for a new compact and affordable electric SUV, which is set to be manufactured in China and may later expand to Europe and the U.S. markets. This model will feature smaller dimensions, a single motor, a smaller battery, and a price lower than the Model 3, focusing on cost reduction and boosting sales volume. This move is seen as a strategic pivot back to the mass market amid setbacks in autonomous driving efforts.

How do analysts view Tesla’s future?

Bulls point out that Tesla’s non-automotive businesses hold long-term “option value,” particularly in the progress made in Full Self-Driving (FSD), the Robotaxi initiative, and the Optimus robot. They also note that demand catalysts in markets such as South Korea have yet to be unleashed and believe that as the stock price becomes “cheap” relative to its future potential in AI and energy sectors,risk-reward ratiois improving.

Bears, on the other hand, emphasize structural issues in the core automotive business, including a narrowing competitive moat and intensifying pressure from rivals such as BYD. They highlight the concerning increase in inventory caused by the significant gap between production and sales volumes and argue that the current forward price-to-earnings ratio of over 300xforward P/E ratiois difficult to justify amid margin compression and deteriorating brand image.

Investment firm Seaport Research Partners downgraded $Broadcom (AVGO.US)$ the rating from “Buy” to “Neutral,” citing the company’s encounter with growth bottlenecks in both the semiconductor and artificial intelligence industries.

Analyst Jay Goldberg stated: ‘In the field of AI computing power, Broadcom remains one of NVIDIA’s primary competitors. However, like NVIDIA, it is increasingly approaching the upper limit of industry growth. In addition to widely discussed supply chain constraints, we have also observed Broadcom’s increasing involvement in providing financing solutions for its clients. Although Broadcom is currently performing well, we believe its growth prospects are already fully priced into market expectations.’

Global Macro

-

The number of initial jobless claims in the U.S. last week was 219,000, compared to an expected 210,000.

The number of initial jobless claims in the U.S. for the week ending April 4 was 219,000, compared to an expected 210,000 and a previous value of 203,000.

The core PCE price index in the U.S. increased by 3.0% year-over-year in February, meeting expectations of a 3.0% rise, with the previous value at 3.1%. The month-over-month rate of the core PCE price index in February remained unchanged at 0.4%, in line with expectations. The final annualized quarterly rate of the core PCE price index for Q4 was 2.7%, matching expectations of 2.7% and a previous value of 2.7%.

Financial Stability Board Chairman Andrew Bailey warned that signs of stress may be emerging in the private credit sector following the market shock triggered by the Iran conflict. Bailey, who also serves as the Governor of the Bank of England, stated on Thursday that regulators need to closely monitor the threats posed by this sector, given the rapid expansion of private credit and the volatile market reactions spurred by Middle Eastern tensions.

“Private credit is a relatively opaque area, and because it is relatively new, it has not yet truly undergone a stress test, but we may now be witnessing such a scenario,” Bailey noted during a European Parliament hearing. Since the financial crisis, private credit has flourished, with Bailey repeatedly warning of the associated risks. At that time, tightened bank regulations prompted corporate borrowers to turn to alternative channels outside public markets, such as investment funds. There are concerns in the market that any issues within this industry could quickly spread to regulated banks and the broader economy. Bailey specifically highlighted similarities to the subprime mortgage crisis.

Helen Jewell of Blackrock recently stated in an interview that corporate earnings expectations need to be revised downward due to inflationary pressures stemming from the conflicts in the Middle East.

The Chief Investment Officer for Fundamental Equities International at the world’s largest asset management firm stated during the interview: ‘Current earnings forecasts for this year remain exceedingly high, at 15%, 16%, 17%, and 18%, indicating significant room for a downward adjustment.’

She also noted that projections of stable earnings in the consumer sector are ‘hard to justify, especially considering interest rate levels and inflationary effects triggered by the situation in the Middle East.’

Signs of loosening optimistic earnings expectations have begun to emerge in the market. After weeks of upward revisions by analysts, Citi’s U.S. Earnings Momentum Index turned negative last Friday, with downgrades surpassing upgrades by the largest margin in nearly a year.

A bond fund that achieved strong positive returns during last month’s record sell-off in the global government bond market, driven by ‘stagflation’ expectations catalyzed by the Iran war, is betting that the yield curves of global government bonds will steepen as countries implement populist-oriented expansionary fiscal policies to cushion the impact of energy shocks. In other words, as ‘developed country governments spend to stabilize public sentiment,’ the bond market may soon begin to demand a price — particularly through an increase in the ‘term premium’ metric, which could drive global long-term bonds into a ‘steepening storm,’ triggering a sustained rise in yields for 10-year and longer-dated government bonds.

The core strategy of this 3 billion euro (approximately 3.5 billion US dollars) bond fund, named Carmignac Portfolio Flexible Bond, focuses on purchasing short-dated government bonds, based on the expectation that yields will fall as aggressive bets on central bank rate hikes are unwound amid multiple favorable factors in the market.

However, the senior fund manager who successfully avoided the sharp downturn in the bond market in March warned that ‘populist’ policies would significantly impact bond prices, with governments adopting populist fiscal stimulus measures to combat economic recession, thereby driving up long-term sovereign yields.

Top 20 pre-market trading volume stocks in the U.S.

Reminder of the US stock market macroeconomic calendar

(The following times are in Beijing Time)

20:30

U.S. Initial Jobless Claims for the week ending April 4 (in ten thousand people)

U.S. Core PCE Price Index Year-over-Year Rate for February

U.S. Personal Spending Month-over-Month Rate for February

U.S. Fourth Quarter Real GDP Annualized Quarter-over-Quarter Growth Rate Final Estimate

U.S. Fourth Quarter Real Personal Consumption Expenditures Quarter-over-Quarter Growth Rate Final Estimate

U.S. Fourth Quarter Core PCE Price Index Annualized Quarter-over-Quarter Growth Rate Final Estimate

U.S. Core PCE Price Index Month-over-Month Rate for February

22:00

U.S. Wholesale Sales Month-over-Month Rate for February

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Looking to pick stocks or diagnose stock performance? Want to know the opportunities and risks in your portfolio? For all investment-related questions,just ask Futubull AI!

Editor/Lee