- The combined EV battery installation volume of CATL and BYD in January was 42.4 GWh, accounting for 59.0% of the global total.

- The combined market share of the three major South Korean battery manufacturers dropped to 12%.

Market share of world’s top EV battery makers (Jan 2026)

| Company | Market Share (%) | Installations (GWh) |

|---|---|---|

| CATL | 45.2% | 32.5 |

| BYD | 13.8% | 9.9 |

| LG Energy Solution | 6.6% | 4.7 |

| CALB | 5.3% | 3.8 |

| Panasonic | 4.3% | 3.1 |

| Gotion High-tech | 3.9% | 2.8 |

| SK On | 3.2% | 2.3 |

| Svolt | 2.7% | 1.9 |

| Eve Energy | 2.4% | 1.8 |

| Samsung SDI | 2.2% | 1.6 |

| Others | 10.4% | 7.5 |

CATL (HKG: 3750, SHE: 300750) saw its share of the global electric vehicle (EV) battery market grow year-on-year in January, while BYD (HKG: 1211) experienced a decline in its share due to decreased vehicle sales.

In January 2026, total global EV battery usage was about 71.9 GWh, up 10.7% year-on-year, according to data released on Friday by South Korean market research firm SNE Research.

Chinese power battery giant CATL maintained its position as the global number one. Its battery installation volume reached 32.5 GWh, a 25.7% increase from 25.9 GWh in the same period last year.

The company supplies Chinese automakers such as Seres, Xiaomi, Li Auto, and Geely Auto, and is also a major supplier to global automakers like Tesla (NASDAQ: TSLA), BMW, Mercedes-Benz, and Volkswagen.

CATL is also advancing the commercialization of sodium-ion batteries to strengthen its competitiveness in next-generation battery technologies, SNE Research noted.

BYD ranked second globally with a battery installation volume of 9.9 GWh. Although this represents a 1.9% decrease from 10.1 GWh in January 2025, its global ranking remained stable.

BYD’s market share in January 2026 was 13.8%, down from 15.6% in January 2025.

BYD’s sales in the Chinese market dropped by 23.4% in January, while its European market grew by 69.4% and other regions surged by 97.6%, SNE Research noted.

The top three South Korean battery makers saw a significant decline in their market shares. The combined share of LG Energy Solution, SK On, and Samsung SDI fell to 12%.

LG Energy Solution, SK On, and Samsung SDI ranked 3rd, 7th, and 10th with 4.7 GWh, 2.3 GWh, and 1.6 GWh, respectively.

LG Energy Solution’s battery usage decreased by 14.9% year-on-year, SK On declined by 21.3%, and Samsung SDI dropped by 24.4%.

This change was primarily driven by a drop in demand in the US market, where EV sales fell by 30.2% year-on-year.

Samsung SDI mainly supplies batteries to brands like BMW, Audi, Rivian, and Land Rover, but sluggish sales of certain models dragged down its installation volume.

SK On’s batteries are mainly used by automakers such as Hyundai Motor Group, Ford, Mercedes-Benz, and Volkswagen. LG Energy Solution’s major clients include Tesla, Hyundai, Renault, and Volkswagen.

China’s CALB (HKG: 3931) ranked fourth in January 2026 with an installation volume of 3.8 GWh and a 5.3% market share.

Japan’s Panasonic ranked fifth globally in January with an installation volume of 3.1 GWh and a 4.3% share.

China’s Gotion High-tech and Eve Energy ranked sixth and ninth with market shares of 3.9% and 2.4%, respectively.

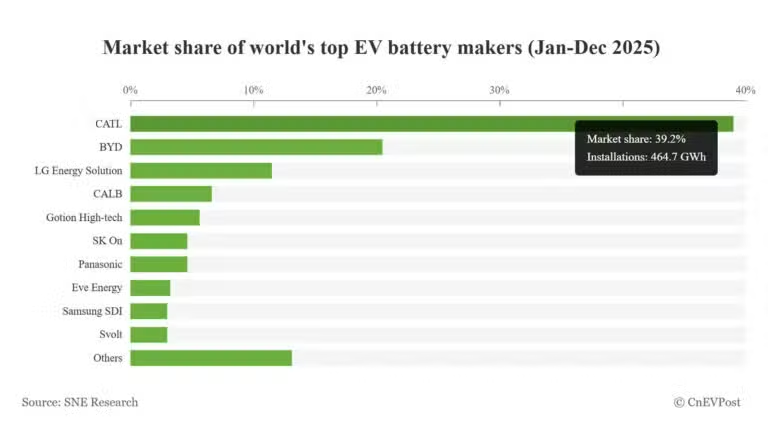

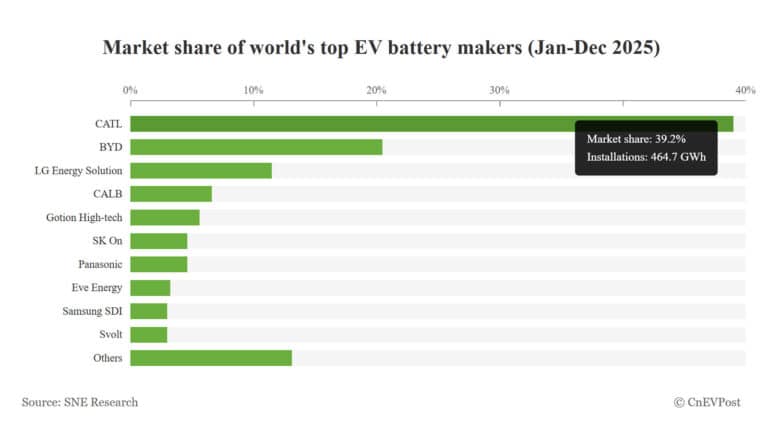

CATL and BYD’s combined EV battery installations in 2025 came in at 659.5 GWh, accounting for 55.6% of the global total.