blackred/iStock via Getty Images

By Richard Stevens

The Bank for International Settlements (“BIS”) has updated its 2025 Triennial Central Bank Survey of foreign exchange (FX) markets with additional data. Every three years, this data provides invaluable insight into the state of the world’s foreign exchange markets.

But what can it tell us about potential future developments in FX? Here are five things to consider.

1. Volatility Levels Are Not What They Were

Firstly, it is important to remember that the BIS survey was conducted in April 2025. During that particular month, the markets were abound with revelations about the United States’ tariff policy, which in turn led to substantial volatility in the FX markets.

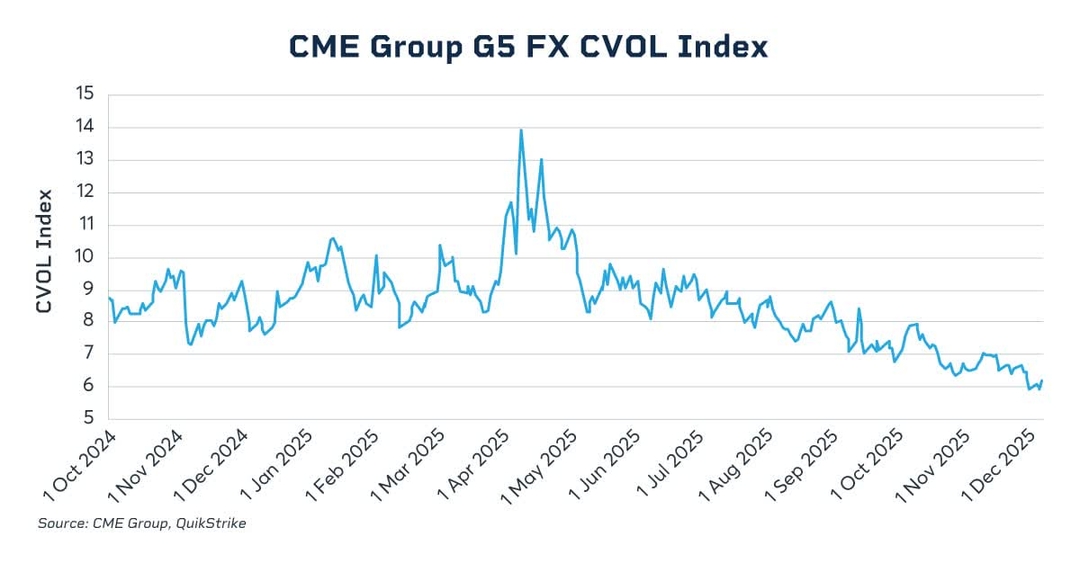

This heavily contributed to the record level of transactions observed by the BIS of $9.51 trillion per day. Since that period, trade policy has stabilized and FX volatility has declined. CME Group’s CVOL indices of options’ implied volatility are decidedly lower, with values in the lower quartile for all time data.

With fewer shake-ups in trade policy anticipated, volatility and transaction volumes may continue to be lower than the levels seen last April.

However, lower volatility does not seem to have reduced the need for hedging in FX markets. Toward the end of 2025, CME Group saw records for total open interest in FX futures and in the hedging positions held by asset managers, with the latter ending the year approximately 32% higher than at the start, at $185bn.

2. Emerging Markets Are On the Rise

The BIS survey highlighted an outsized growth in emerging market currency activity. Trade in emerging market currencies has grown at more than double the pace of developed market currencies over the three years to April 2025.

The largest emerging market currency is the Chinese renminbi. Turnover in the renminbi grew 56% in the three years to April, consistent with the pace it has been expanding at for the previous decade. As the world’s second-largest economy, this growth seems justified and it’s highly likely that the rapid growth in renminbi trading will continue into 2026.

CME Group recently announced a new suite of futures and options contracts linked to the internationally-traded version of the renminbi, referred to as “CNH”. These physically delivered contracts are designed to meet the needs of international firms active in the growing renminbi marketplace and will complement the leading primary market status of EBS’s offering in spot CNH.

Another notable mention in CME Group’s emerging market FX offering is the growth seen in Brazilian real futures (BRL). While the BIS assesses the growth in BRL trading to be 37% between 2022 and 2025, CME Group’s futures volumes have increased 109% in the same period.

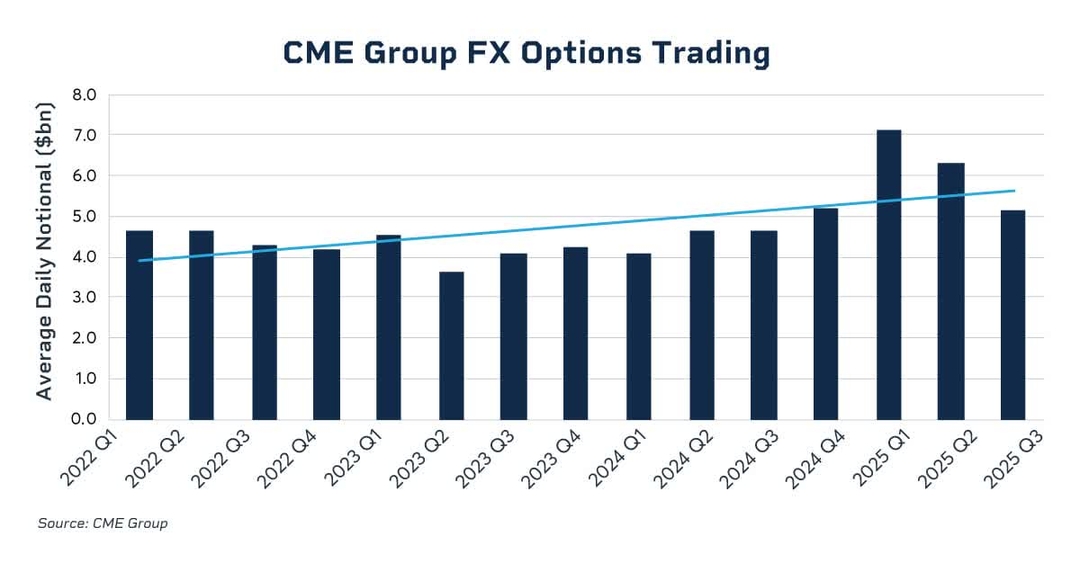

3. Options Trading Continues to Grow

Of the five main types of FX instruments that the BIS survey assesses, options had by far the largest growth rate over the three years since the preceding survey, more than doubling in that period.

This increased volume may well be a function of the heightened volatility seen at the time of the survey, but strong volumes were recorded across all counterparty types, and interim data from central banks shows a consistent increase in options trading.

While a small part of the overall market, it is noteworthy that retail trading of options in Asian currencies was up nearly 600%.

CME Group’s exchange-traded FX options, not included in the BIS analysis, have also seen a growth in activity over the same period. Planned product launches in 2026 for new CME Group FX options on Chinese renminbi and Indian rupee should appeal to traders in Asian currencies and will support the continued development of the FX options market.

4. A Shift from Swaps to Spot?

While there has been substantial growth in overall trading activity since the 2022 BIS survey, FX swaps didn’t follow this trend. As an example, trading in spot EUR/USD increased 38% between the two surveys, trading in EUR/USD forwards increased 55%, but trading in EUR/USD FX swaps decreased 14%.

This might have been the market focusing on outright trading in the face of an active news cycle, but nevertheless, it’s a significant data point given the previous survey highlighted FX swaps as the premier vehicle of growth. BIS analysis suggests the focus away from FX swaps is a longer term trend.

That being said, FX swaps are still a central tool of FX risk management. While smaller in size, FX futures are also a transparent risk management tool. Comparing CME Group’s FX futures volumes in April 2025 to April 2022 shows a 52% increase over the period. Furthermore, CME Group’s FX Link product, which combines FX futures with spot to provide a transparent pool of IMM dated FX swap pricing, had several record days in 2025, and over $14bn traded.

In spot FX, EBS spot volumes increased 35% between April 2022 and April 2025, consistent with the broader market. But April 2025 was a particularly significant month for CME Group with the launch of the FX Spot+, a unique new all-to-all spot FX marketplace that translates futures liquidity into spot terms. Volume and participation has continued to grow since launch, and CME Group’s concept of bringing the FX market together has a bright future.

5. Reliability of Data and Trading Platforms

The additional data published by the BIS includes a breakdown of the execution methods for the various transaction types. This data shows that, compared to other asset classes, voice trading continues to play a substantial role in FX markets.

While opaque in terms of process, price formation for these transactions likely relies on the data made available in public markets. This means that data from EBS Market – a primary FX venue – will continue to play an important, if indirect, role in these trades.

In 2025, CME Group announced the launch of a new FX Tape+ service to provide consolidated FX market data to a wider audience, providing timely information to help guide pricing and trading decisions for both spot and IMM dated forward risk.

Another encouraging data point from the BIS survey was the share of execution from indirect electronic venues. This category was split into anonymous and disclosed services, and includes the venues EBS Market and EBS Direct.

While the 2022 BIS survey indicated a decline in the share of transaction volume seen at these venues, 2025 data showed an increase in market share across all instruments.

As the BIS acknowledges, the FX market is decentralized and fragmented, which contributed to a resilient marketplace. Electronic venues, such as those offered by CME Group, provide consolidated credit-neutral liquidity and pricing, and have an important and sustainable place in the ecosystem.