The 2025 holiday season exposed a clear split in consumer behavior across the world’s two largest e-commerce markets. In the United States, spending continued, but with tighter budgets and more deliberate timing. In China, platforms pushed discounts harder to defend traffic amid weak confidence. That contrast is now shaping how Alibaba (NYSE:) vs. Amazon (NASDAQ:) stocks are priced heading into the year-end.

U.S. Consumers Slow, Not Stop

U.S. holiday retail sales for the 2025 season are expected to grow 2.9% to 3.4% year over year, reaching roughly $1.61–$1.62 trillion, according to Deloitte forecasts cited by Reuters. Growth slowed from 4.2% last year as higher borrowing costs and persistent inflation constrained discretionary spending.

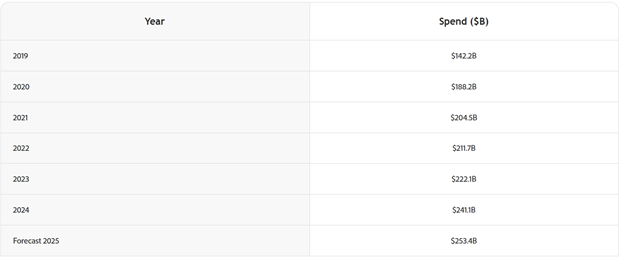

Online channels continued to carry most of the expansion. Adobe Analytics projects U.S. online holiday sales of $253.4 billion, up 5.3% year over year, driven by mobile usage and longer promotional windows.

Source: https://business.adobe.com/resources/holiday-shopping-report/consumer-spend-during-the-holiday-season.html

Payment behavior points to caution rather than confidence. Adobe estimates Buy Now, Pay Later spending will reach $20.2 billion, an 11% increase from 2024, indicating consumers are spreading payments instead of raising total outlays.

Source: https://business.adobe.com/resources/holiday-shopping-report/buy-now-pay-later-forecast.html

Together, these signals frame Amazon stock vs. Alibaba as a comparison between a stable but budget-aware U.S. consumer base and more fragile demand elsewhere.

China Turns to Discounts

China entered the holiday period under heavier pressure. Slower income growth and soft confidence pushed platforms into sustained price competition. This Alibaba pricing strategy mirrors broader China consumer spending trends, where maintaining volume has taken priority over protecting margins.

Reuters reports that China’s major e-commerce platforms are locked in a prolonged price war, with subsidies and discounts weighing on profitability across the sector. Nomura estimates that competition in instant retail alone led to more than $4 billion in industry-wide cash burn in Q2 2025.

Alibaba still delivered quarterly revenue of 247.8 billion yuan (about $35 billion), beating expectations as logistics efficiency and cloud services offset weaker discretionary demand.

Management acknowledged that promotions continued to pressure margins.

The dynamic points to ongoing e-commerce discount wars in China, with pricing intensity well above U.S. levels.

Markets Price the Split

Equity performance in 2025 followed consumer behavior closely. Baba vs. AMZN comparisons increasingly reflect a divide between stimulus-driven volume and predictable cash generation.

Alibaba’s revenue resilience contrasts with domestic demand risks, complicating the outlook for Alibaba stock vs. Amazon. Investors, by contrast, continue to favor scale, logistics reach, and recurring revenue in the U.S. market.

These forces define the broader AMZN vs. BABA narrative across US vs. china e-commerce stocks.

What to Watch in 2026

The holiday season did not reset global consumption. It clarified where pressure remains. U.S. spending slowed but held. China relied on discounts to keep volumes moving.

For investors looking to trade Amazon vs. Alibaba or structure a versus trade AMZN BABA, the focus in 2026 will be on consumer confidence, the durability of discount-led growth in China, and margin discipline across platforms. In a period of global consumer slowdown, those factors may matter more than headline sales figures. In that context, BABA vs. AMZN stock increasingly reflects a choice between stimulus-driven volume and predictable cash generation.