3 Undervalued Small Caps In Global With Insider Action

Uncategorized

3 Undervalued Small Caps In Global With Insider Action

08 mins

In recent weeks, global markets have shown resilience amid geopolitical tensions and energy market volatility, with smaller-cap indexes posting solid gains as major U.S. stock indexes advanced. As investors navigate these uncertain times, identifying stocks that may be undervalued can offer potential opportunities for growth, particularly within the small-cap sector where insider activity might suggest confidence in a company’s prospects.

We’re going to check out a few of the best picks from our screener tool.

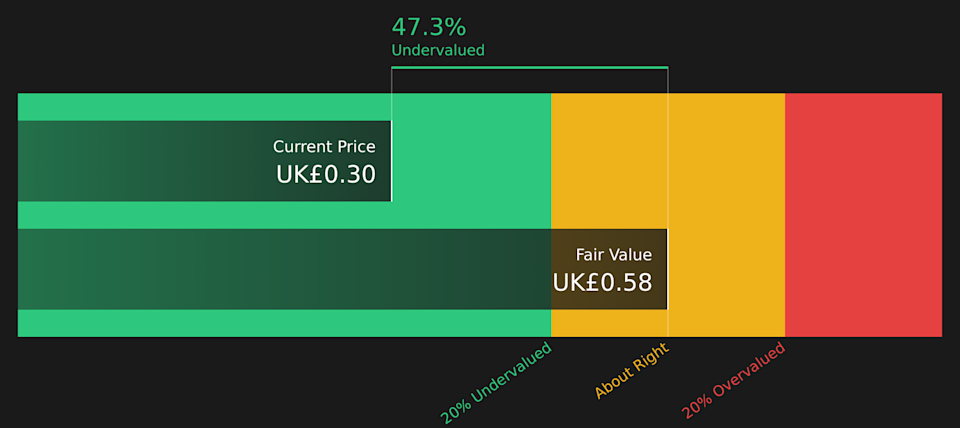

Simply Wall St Value Rating: ★★★★★☆

Overview: S4 Capital is a digital advertising and marketing services company with operations primarily in marketing and technology services, boasting a market cap of approximately £1.15 billion.

Operations: The company generates revenue primarily from Marketing Services (£695.80 million) and Technology Services (£59 million). Over recent periods, the gross profit margin has shown an upward trend, reaching 89.16% by the end of 2025. Operating expenses are a significant cost component, with general and administrative expenses consistently being the largest portion.

PE: -8.2x

S4 Capital, with its recent executive appointments and a focus on AI-driven systems, is positioning itself for strategic growth in a competitive media landscape. Despite reporting a net loss of £24.8 million for 2025, the company has shown improvement from the previous year’s larger loss. Insider confidence is evident as insiders purchased shares over the past year. The proposed dividend increase to 1.1 pence per share reflects management’s commitment to returning value to shareholders amid volatile share prices and higher-risk funding sources.

LSE:SFOR Share price vs Value as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

Overview: Primaris Real Estate Investment Trust focuses on the ownership, management, and development of its investment properties with a market capitalization of approximately CA$1.90 billion.

Operations: The company generates revenue primarily from the ownership, management, and development of its investment properties, amounting to CA$648.47 million. Its gross profit margin has shown a range from 47.54% in 2020 to 57.65% in recent periods, indicating variations over time. Operating expenses have been recorded at CA$41.58 million recently, while non-operating expenses are noted at CA$142.96 million for the same period.

PE: 11.5x

Primaris Real Estate Investment Trust, a smaller player in the real estate sector, has shown potential for value with its recent financial performance. For the year ending December 2025, sales rose to C$648 million from C$502 million previously, while net income more than doubled to C$183 million. The company recently appointed Julian Schonfeldt as CIO to enhance investment strategies and leverage excess lands. Additionally, Primaris completed a share repurchase of 3.43% for C$53.22 million by December 2025, reflecting management’s confidence in its long-term growth prospects.

TSX:PMZ.UN Share price vs Value as at Apr 2026

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Versamet Royalties is a company engaged in acquiring and managing royalty interests primarily in the mining sector, with a market capitalization of approximately C$1.2 billion.

Operations: Versamet Royalties generates revenue from multiple locations, with Greenstone in Canada contributing the largest share at $14.43 million, followed by Kiaka in Burkina Faso at $8.10 million. The company experienced fluctuations in its gross profit margin, peaking at 56.54% as of December 31, 2025. Operating expenses and non-operating expenses are significant cost components impacting financial performance over the observed periods.

PE: 51.7x

Versamet Royalties, a smaller player in the industry, has shown significant growth with 2025 revenue reaching US$34.76 million, up from US$12.03 million the previous year. Insider confidence is evident as Tether Investments increased their stake through private placements in February 2026. The company recently expanded its credit facility to US$225 million, enhancing financial flexibility despite relying solely on external borrowing for funding. Future prospects include strong earnings growth and increased gold and silver revenue contributions.

TSX:VMET Share price vs Value as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LSE:SFOR TSX:PMZ.UN and TSX:VMET.