-

In March 2026, Macy’s reported fourth-quarter revenue of US$7,916 million and net income of US$507 million, alongside full-year 2025 revenue of US$22,621 million and net income of US$642 million, while also issuing 2026 net sales guidance of US$21.40 billion to US$21.65 billion.

-

Despite slightly lower year-over-year sales, Macy’s grew earnings per share and completed a multi-year buyback totaling 43,158,000 shares, or 15.22% of its share count, signaling a continued commitment to shareholder returns.

-

Next, we’ll examine how Macy’s higher earnings despite softer sales and its completed buyback program influence the existing investment narrative.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

To own Macy’s today, you need to believe its omnichannel and store optimization efforts can offset structurally softer sales and intense margin pressure. The latest results, with higher earnings on lower revenue and 2026 sales guidance of US$21.40 billion to US$21.65 billion, support a thesis focused on efficiency and capital returns, but they do not materially change the near term risk that tariffs, freight costs, and weak discretionary demand could squeeze margins further.

The completion of Macy’s multi year buyback, retiring 43,158,000 shares or 15.22% of the share count for US$876.2 million, is especially relevant here. It helps explain how earnings per share rose despite revenue slipping, and it ties directly into analyst expectations that share count could continue to trend lower, which is an important part of the current catalyst story around potential earnings per share growth even if total revenue remains under pressure.

Yet beneath the stronger earnings headline, investors should be aware that…

Read the full narrative on Macy’s (it’s free!)

Macy’s narrative projects $18.5 billion revenue and $663.0 million earnings by 2028. This implies a 6.5% yearly revenue decline but an earnings increase of about $169 million from $494.0 million today.

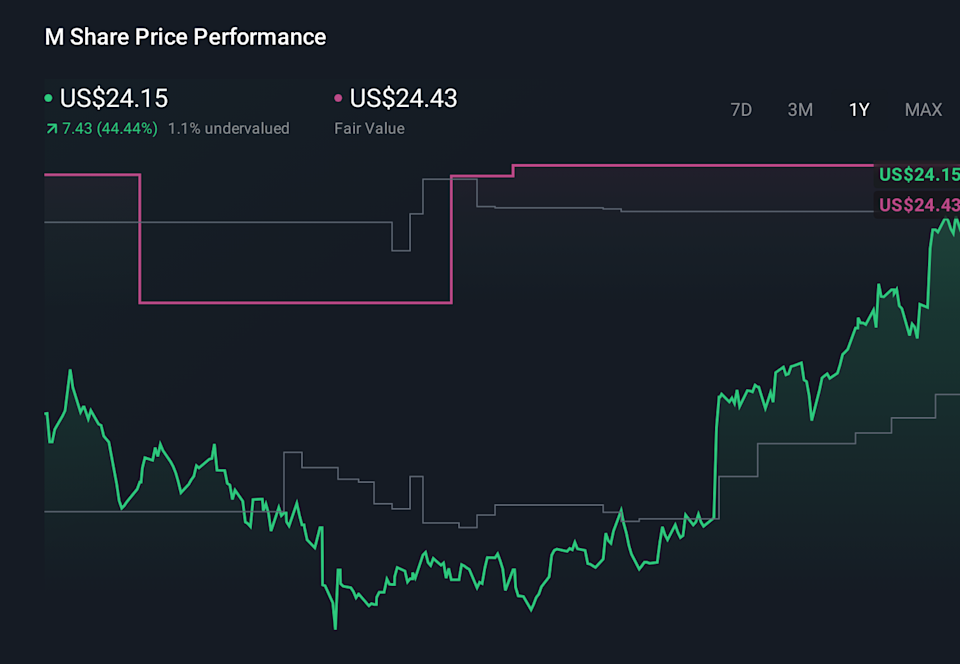

Uncover how Macy’s forecasts yield a $21.80 fair value, a 22% upside to its current price.

Some of the lowest analysts were assuming Macy’s revenue could fall to about US$17.4 billion by 2028 and still saw higher earnings of roughly US$743 million, which is far more pessimistic on the top line than the recent guidance and highlights just how differently you and other investors might weigh the risk that heavy fixed costs and an aging customer base continue to pressure margins even after this latest earnings beat.