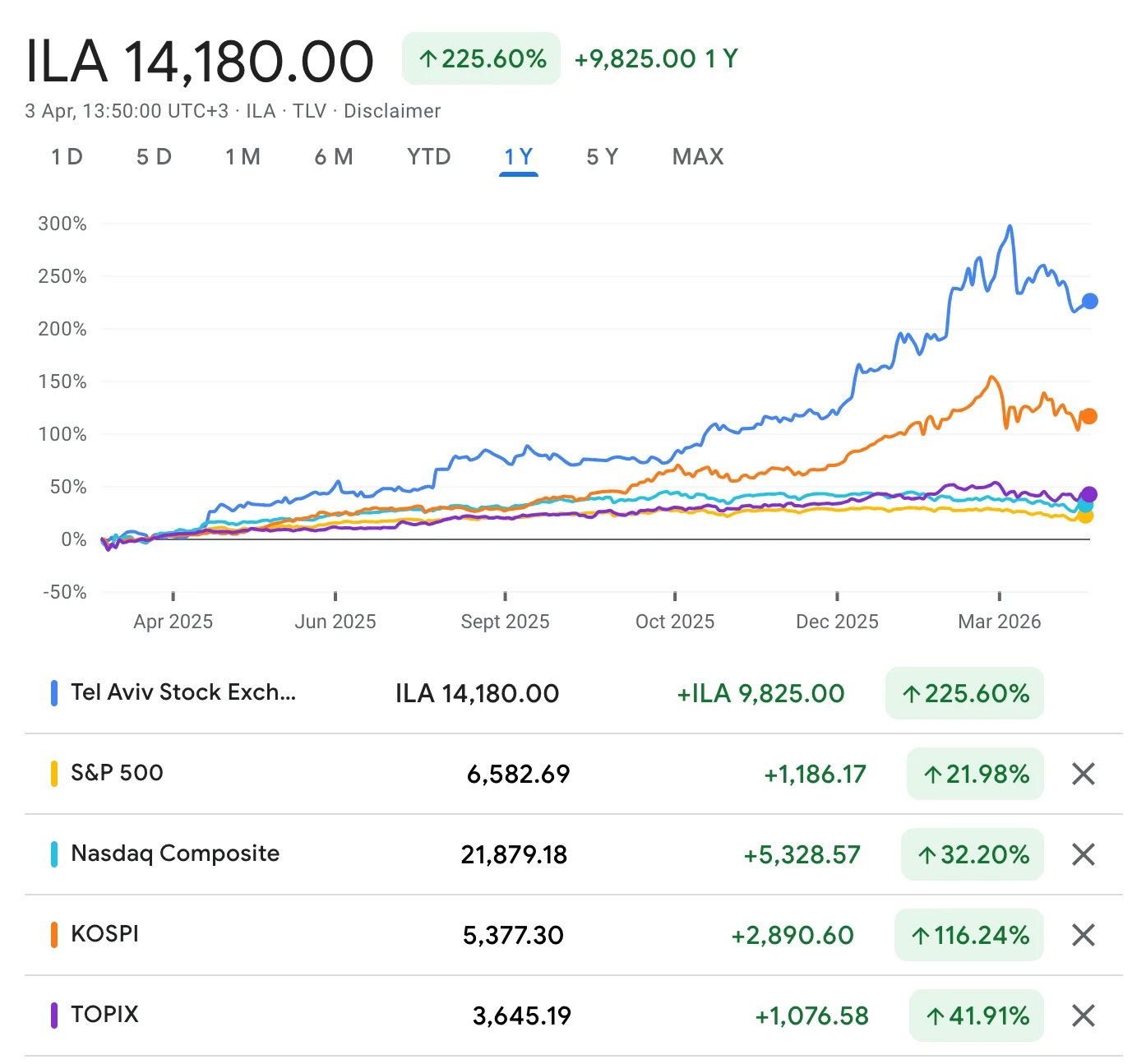

With the S&P 500 down 7.5% YTD, Nasdaq down 10.5%, and crude oil reaching $105/barrel, there’s one country posting positive returns since the year began. Israel. But the question is, why?

(comparison between TASE, S&P 500, Nasdaq, KOSPI & TOPIX international indices)

2026 has been a tale of two halves. January started extremely strong, with the S&P 500 hitting new all-time highs and going above 7,000 on optimism around AI.

The second half of Q1 saw Trump’s escalating tariff threats in February give an initial shock to the market as a reaction to the Supreme Court nullifying his April 4th 2025 liberation day tariffs. Right afterwards, the Iran conflict that started a month ago triggered another decline, driven by the disruption in the Strait of Hormuz.

The Korean KOSPI plunged and tripped the circuit breaker. Even the Tokyo Stock Exchange dropped. Almost all major indices have since entered correction territory, except one.

In early March, the Tel Aviv Stock Exchange climbed sharply on its first trading day after the conflict began as both the TA35 index and the TA125 index reached new record levels.

Israel is the only major index that was still in positive territory in March, yet it’s supposed to be the one country that is most exposed to geopolitical risks. Why? That is the question we’re looking to answer in this edition of Impactfull Weekly.

The anatomy of an Israeli index

Most global investors hear Israel and they think of the famous Unit 8200, the cybersecurity unicorns Wiz, CyberArk, Snyk, Wix and Monday.com and all these software and cyber security darlings. The thing is that it represents the companies listed in the US.

When you open the TA-35 index and you look at the names, you quickly find that you’re buying something that’s very different from what the “Startup Nation” brand suggests.

Financials

What you need to understand about the Israeli index, TA35, is that bank stocks comprise 33% of the TA35, and if you include insurance within it, companies like Phoenix, Harel, and other incoming additions, financial stocks represent 41% of the flagship index.

For context, financials make up only 13% of the S&P 500.

Banks like Leumi, Hapoalim, Discount, Mizrahi Tefahot, First International Have been recording double-digit returns on capital that was unimaginable just a few years ago, and insurance companies like Phoenix, Harel, Menora, Clal, and Migdal have returned more than 150% in 2025, becoming the top-performing sector on the exchange.

In addition, the banks’ loan books have been growing by nearly 15% annually, with an efficiency ratio in the 26-28% range.

Israeli financials & insurers are benefiting the most from this high interest rate environment.

Energy

So this is the second biggest pillar in the TA35 index, with about 12% of companies being in energy, with Delek Group, NewMed Energy, and Ratio Energies being some of the biggest names.

The reason why energy is such a big component of this index is that Israel is a net natural gas exporter, with Leviathan and Tamar pipelines sitting in the eastern Mediterranean, which are completely outside of the Strait of Hormuz choke point. They are therefore relatively shielded from the Iran conflicts.

These gas companies are expected to produce a record amount of natural gas above 3 billion cubic feet per day for the first time. And as we mentioned in a previous essay on the Strait of Hormuz and its effects on global commodities, Israel has found itself on the right side of the non-Gulf supply diversification.

Defence

This should come as no surprise to most, as with 8-10% of companies being in this sector, Elbit Systems is the single largest constituent by market cap at around $40 billion.

However, it is capped at 7% of the index so that no one stock can dominate the entire index.

Elbit Systems recorded a backlog of $28.1 billion, and a combined Israeli defence sector backlog is above $80 billion.

In Elbit Systems’ case, the latest production collaborations with Volkswagen is just an example of many of the deals that they’ve been signing with leading industrial heavyweights to boost their exporting capacity.

For example, the Arrow 3 missile system contract with Germany is now valued at more than $6.5 billion, which is the largest defence export deal in Israeli history.

Tech/Semiconductors

With a nearly 18% composition, semiconductor stocks are usually quite underrated, but with the latest AI boom, there has been one Israeli darling that was acquired by Nvidia, Mellanox.

(source: NVIDIA Newsroom)

Since then, lots of companies have had their stock rise considerably, like Tower Semiconductor, Nova, Check Point, and NICE.

Another interesting point that we will cover later on is how there have been reforms in the way Israeli companies can list to promote a dual listing of stocks for the companies founded in Israel. Palo Alto Networks completed the CyberArk acquisition in February and therefore immediately announced a Tel Aviv Stock Exchange dual listing under the ticker CYBR.

Pharma

The Israeli pharma sector with 8% weight in the TA-35 is anchored by Teva Pharmaceuticals, the second biggest stock on the index, who says around 200 million people worldwide take a Teva medicine every day and is widely described as one of the world’s largest generic-medicine companies.

Beyond Teva, the sector includes established specialty-pharma and biotech names such as Taro, Kamada, Protalix, BioLineRx, etc.

These listed names show us that Israel’s pharma and biopharma sector is the strongest when it comes to generics, specialty therapeutics, oncology, dermatology, and rare-diseases, even going on more industrial sectors like biologics development rather than in a large domestic consumer-drug market as we see in the US.

Everyone thinks that buying into the Israeli stock market means that you’re almost entirely just buying into defence and cyber security, but seeing the diversity of this exchange, we actually see that it’s not the case.

We’re buying one of the most profitable banking sectors among developed economies, a domestic insurance industry that is being repriced as sovereign risk goes down.

(source: Bloomberg)

Plus the biggest recent vector is Israel becoming a gas export monopoly in a region where every other supplier’s route goes through the Strait of Hormuz, which is under attack, or the Bab el-Mandeb Strait, where you have Yemeni Houthis still making the passing of ships not fully zero-risk.

What makes the index the index?

The Israeli TA35 index rally is more structural in nature, compared to a pure tech-driven rally of the S&P 500, and a reflection on the export-oriented economy, where we see the following points strengthen the narrative:

7% weight cap

The individual company weights of each of the 35 companies are capped at 7% and are enforced quarterly. It was introduced in the 2017 reform of the Israeli stock exchange, where the cap was reduced from 10%. This means that any single company, like Elbit, having a 50%+ rally cannot mechanically drag the index up, the way NVIDIA tends to distort the returns of the S&P 500.

(source: Apollo)

What it means: If the TA-35 is at an all time record, it means banks, insurers, defence, energy, and pharma are all moving together. It’s a more honest barometer of economic health than an index where seven companies account for 30% of returns.

2017 index reform

Nearly ten years ago, there was a sweeping reform in the way this index was used to work, where it expanded from 25 companies to 35 companies.

Before the reform, more than 70% of the old index’ weight was concentrated in just 10 shares. This reform was explicitly designed to reduce any risk of concentration, as we see in the case of Nvidia and the S&P 500.

Why this matters for institutional investors: most global pension funds, sovereign wealth funds, and large asset managers have internal concentration limits that prevent them from buying into indices where a handful of names dominate. And this diversification made it eligible for large, institutional allocations to the resilience story of Israel.

Specialist indices

(source: Tel-Aviv Stock Exchange)

In late 2025 and early 2026, TASE launched eight new specialist indices in six months: TA-Defence, TA-Real Estate 35, TA-Infrastructures, TA-Technology 35, TA-Israel Energy, and more.

The TA-Technology 35 is the most important of these. Launched in February 2026, it mirrors the Nasdaq 100 methodology and is designed to house dual-listed tech names. But domestic institutional money actually is quite risk-off as they are invested heavily in financials over tech: only about $273 million is invested in the TA-Technology index, versus about $13 billion tracking bank stocks. That is a 46:1 ratio.

The ratio tells us two things: First, domestic institutional capital has not yet rotated into tech, which means the TA-Technology 35 is launching into a market with enormous latent demand if even a small fraction of the $13 billion currently tracking bank stocks were to rebalance towards tech.

Secondly, it tells foreign investors that TASE is now building the infrastructure they need to take targeted sector bets.

The TA-35’s war-time resilience did not appear from nowhere. Over the past 18 months, TASE has been executing a series of reforms designed to bring itself in line with global capital market standards. The war arrived just as these reforms started compounding.

Above we discussed what makes the index, but now we’ll look at why and how the market is positioned through these past reforms to take maximum advantage of the current volatility in the Middle East, making it an easy haven to absorb incoming institutional capital.

Mon-Fri trading week

On 5 January 2026, TASE made the single most important structural change in its 72-year history: it shifted from a Sunday-to-Thursday trading week to Monday-to-Friday.

For decades, the old schedule meant zero overlap with US and European markets on two days per week. If you were a portfolio manager in London or New York, you could not trade Israeli stocks on a Friday (your busiest rebalancing day) or a Monday (Israel’s day off).

The Friday session is shortened (9:25 AM to 1:50 PM local time) to accommodate the start of Sabbath, but it exists. Previous attempts to make this switch failed because of opposition from banks and labour unions.

A joint initiative between TASE, the Israel Securities Authority, and the Bank of Israel finally pushed it through.

The immediate result: foreign participation on the first Friday session was double that of a typical Sunday session under the old schedule.

(source: Globes, Israel’s leading business newspaper)

This is the Israeli equivalent of Korea lifting its short-selling ban, which we covered in our previous essay on the Korean market reforms. In both cases, a structural barrier was physically preventing global institutional capital from entering.

Dual listing pipeline

In February 2026, Palo Alto Networks completed its $25 billion acquisition of CyberArk and immediately announced a TASE dual listing under the ticker CYBR.

To put that in perspective: at a $115 billion market capitalization, Palo Alto becomes the largest company on the Tel Aviv exchange by a huge margin. Elbit Systems and Teva both are at $40 billion each.

CyberArk’s Israeli R&D centre (Palo Alto Network’s largest outside Silicon Valley) has been preserved as the core innovation hub. This pattern is well recognised to keep engineering talent at home, like in some European countries, as Google’s $32 billion acquisition of Wiz (approved by the EU) also came with the Wiz founders committing to maintain Israeli operations as the centre of Google Cloud security.

(source: Palo Alto Networks Newsroom)

Four of the five largest Israeli companies on Wall Street are already dual-traded on TASE (Teva, Elbit, Tower Semiconductor, Nova).

If the NYSE/NASDAQ-listed companies or soon to IPO companies were to follow Palo Alto Networks in the near future (Wix, monday.com, Global-E, or Lemonade) for a dual-listing, they would immediately qualify for the TA-35 index at current valuations.

The new TA-Technology 35 index, launched February 2026, is designed specifically to house these dual-listed tech names using Nasdaq 100’s methodology.

MSCI Europe candidacy

Israel is currently classified in the MSCI Europe and Middle East Index, which means that most of the global “Europe” funds get zero Israeli exposure by default because of the Middle East classification.

(MSCI’s Europe & Middle East Index)

Any potential inclusion in the core MSCI Europe index could trigger significant passive inflows, as most institutional investors are exposed in one way or the other to the MSCI Europe index. (Meaning every ETF tracking European equities would also then need to add Israeli stocks to their selection.)

Here’s when the timing plays a crucial role: if the MSCI reclassifies Israel as part of the core Europe index post-U.S./Israel/Iran conflict, and with the Iranian threat structurally reduced, this decision could be materially positive for the index.

(our list of 13 companies bound to benefit from the Israeli resilience & dual-listing reform)

To dig further into smaller companies that are bound to benefit from the Israeli resilience & dual-listing reform, create your own StockScreener like we did:

Bonus: ETFScreener

To find out more about ETFs available to index this Israeli resilience & dual-listing reform, make your own ETF Screener like we did:

The Israeli stock market is rallying either by design or by accident, thanks to its constituents leveraging the macro environment we are currently living in.

When the majority of your index is financials and insurers that benefit from a higher rate environment, as well as having an energy sector relatively unaffected by the Iran attacks, and being one of the only major natural gas exporters in the region, you feel that Israel is in for a structural boom that is quite different from the ones we had covered previously (Japan, Korea, Brazil, Argentina, LatAm, etc.).

Plus the 7% weight cap makes sure that one single cyclical trade can’t affect the index as a whole, underlining the current rally as more of a structural one, where financials are benefitting, defence is benefitting, energy (via natural gas exports) is benefitting, and thanks to the dual-listing reforms encouraging the famous Israeli tech darlings that are currently listed in the US with Nasdaq or NYSE to consider a dual-listing in the TASE.

The fact that the Palo Alto dual-listing process took only a couple weeks vs. a months-long struggle, is also helping other NASDAQ/NYSE listed companies consider a dual-listing, bringing much needed liquidity and blue chip names to the TASE.

The question is whether the rest of the world’s capital allocators catch up to what the index is today and will be tomorrow: a financials-heavy, energy-exporting, defence-primed market trading at a fraction of the multiples its profitability deserves, with recent reforms only just starting to show signs of early success.

Stay invested, cautiously.