We started writing our Market Call on Friday. Saturday morning, we woke up to the news of the joint military campaign by the US and Israel against Iran’s evil Mullah regime. It appears that the two allies have complete air superiority. In a video statement posted to social media, US President Donald Trump vowed to destroy Iran’s missile program and navy, and ensure that the country can “never” have a nuclear weapon. Iran’s defenses were already badly degraded by last year’s attacks by Israel and the US.

So we doubt that the Iranian regime will be able to block the Strait of Hormuz, as it has threatened to do in response to being attacked. If that’s the case, then increased production by the rest of OPEC is likely to limit any rise in oil prices due to a decline in Iran’s oil exports during the current conflict. Furthermore, the oil market might start to anticipate that if the Mullahs are toppled, then Iran will export even more oil.

We wouldn’t be surprised if any rally in the S&P 500 Energy sector on Monday morning fades by the afternoon. We wouldn’t be surprised if any selloff in the S&P 500 on Monday morning turns into a rally, driven by expectations of lower oil prices once the latest Middle East war ends. The price of gold might also round-trip on Monday. Bond yields might fall due to both safe-haven demand and post-war prospects for lower oil prices.

Now back to our regularly scheduled programming:

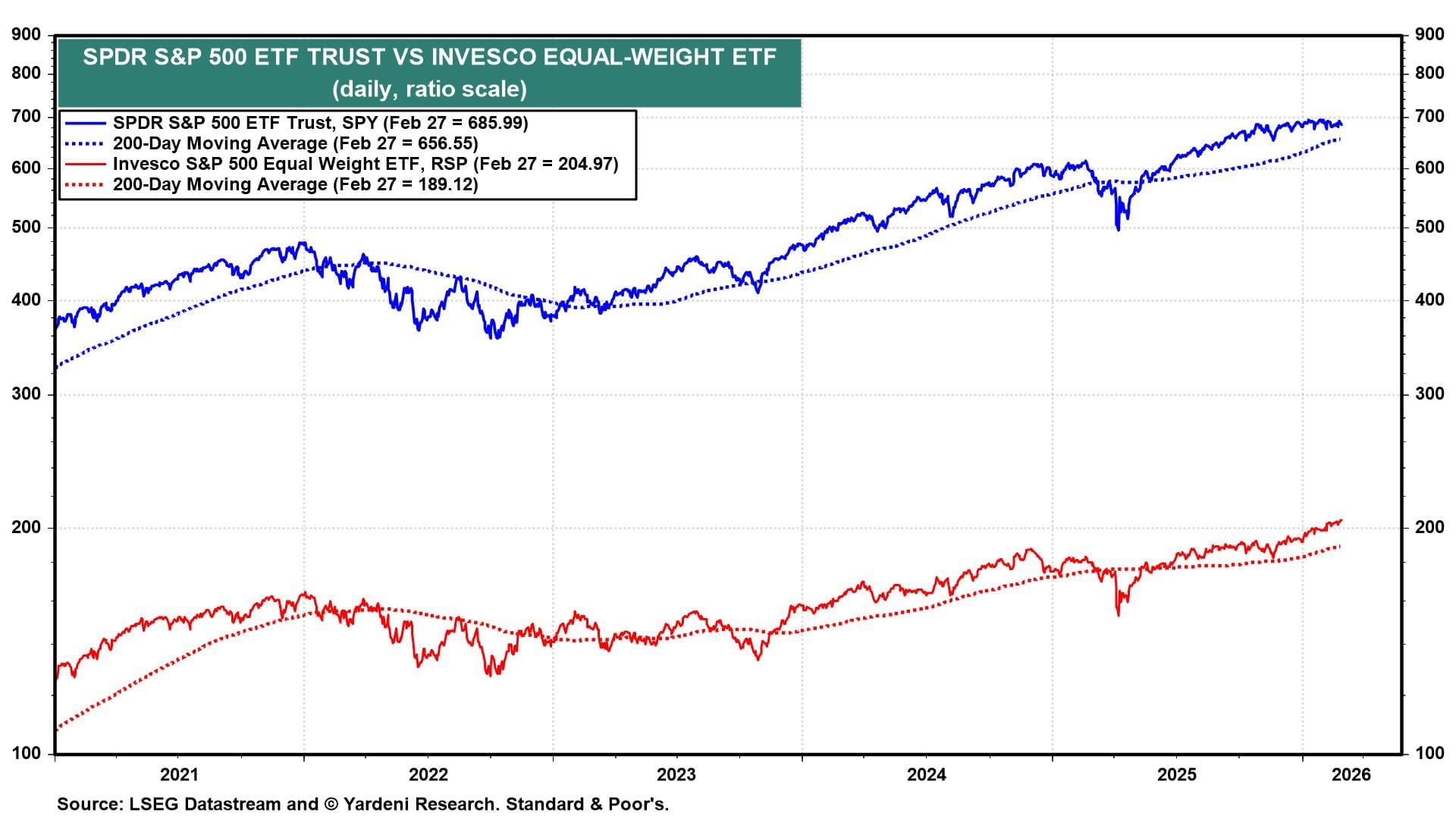

(1) Performance. RSP (the S&P 500 equal-weight ETF) rose to a new record high on Friday, while SPY (the S&P 500 market-weight ETF) fell 0.4% (chart). The former is up 7.0% ytd, while the latter is up just 0.6%. In early December of last year, we recommended rebalancing out of the Magnificent-7 and into the Impressive-493. So far, so good, as the former has outperformed the latter. We expected that the stock market might be choppy during the first half of the year. That’s half true, as RSP has risen to record highs, while SPY has churned below 700, just as the S&P 500 market-weight stock price index has been choppy below 7000.

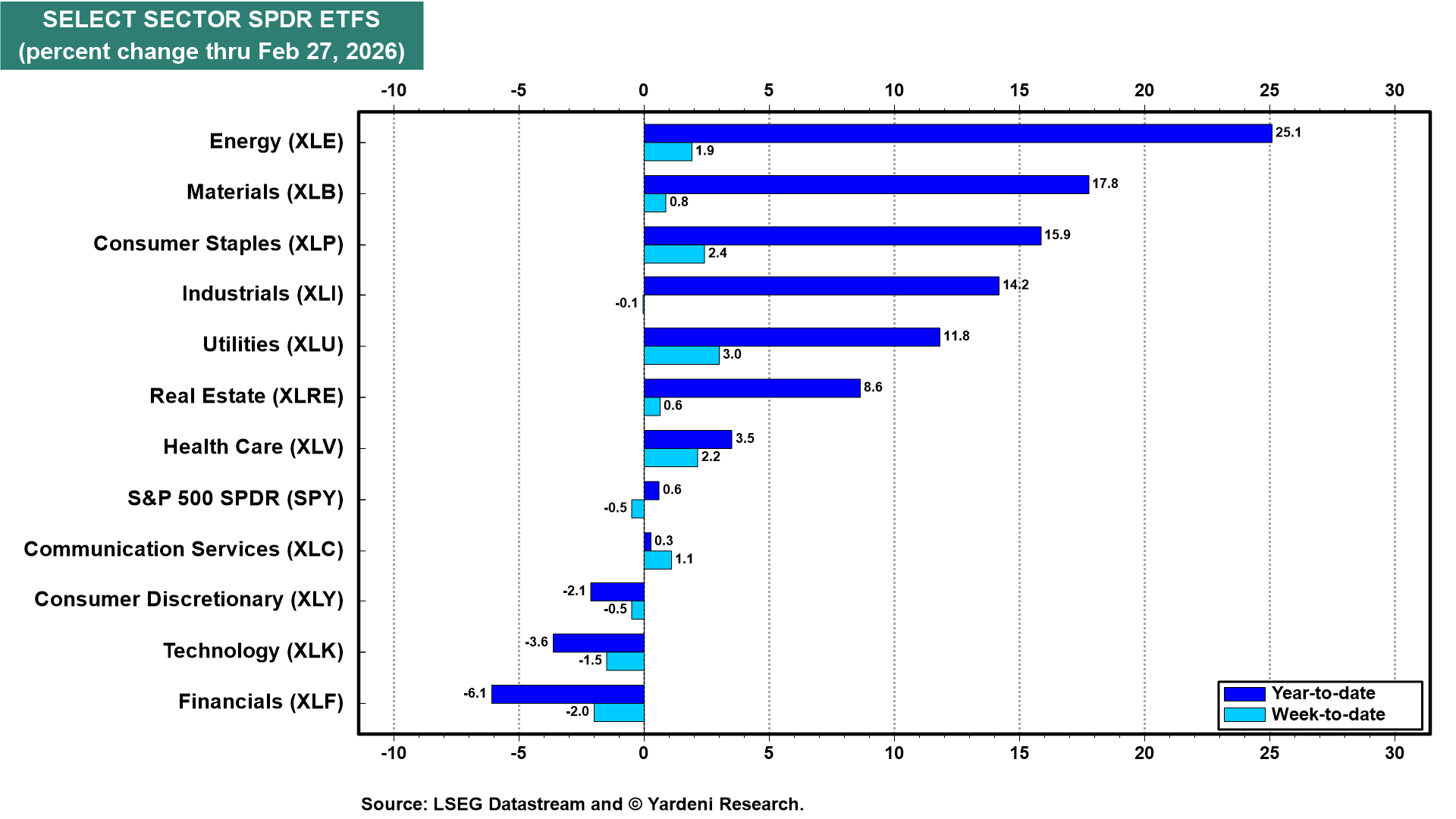

The worst performing sector of the S&P 500 ytd has been the Financials sector (chart). On February 12, we wrote: “We are dropping our overweight recommendation on Financials to market weight, while maintaining our overweights on Health Care, Industrials, and Materials (as of yesterday). We are glad that we advised underweighting the Magnificent-7 and overweighting overseas stocks in early December last year.”

Financials were hard hit this year by President Trump’s proposal to cap credit card rates at 10%, by fears of a private debt crisis, and by concerns that AI will disrupt many of their business models. On Friday, the sector was hit hard again by January’s hotter-than-expected PPI inflation rate. That reduced the likelihood of Fed rate cuts in the coming months. We remain in the none-and-done camp, for now.

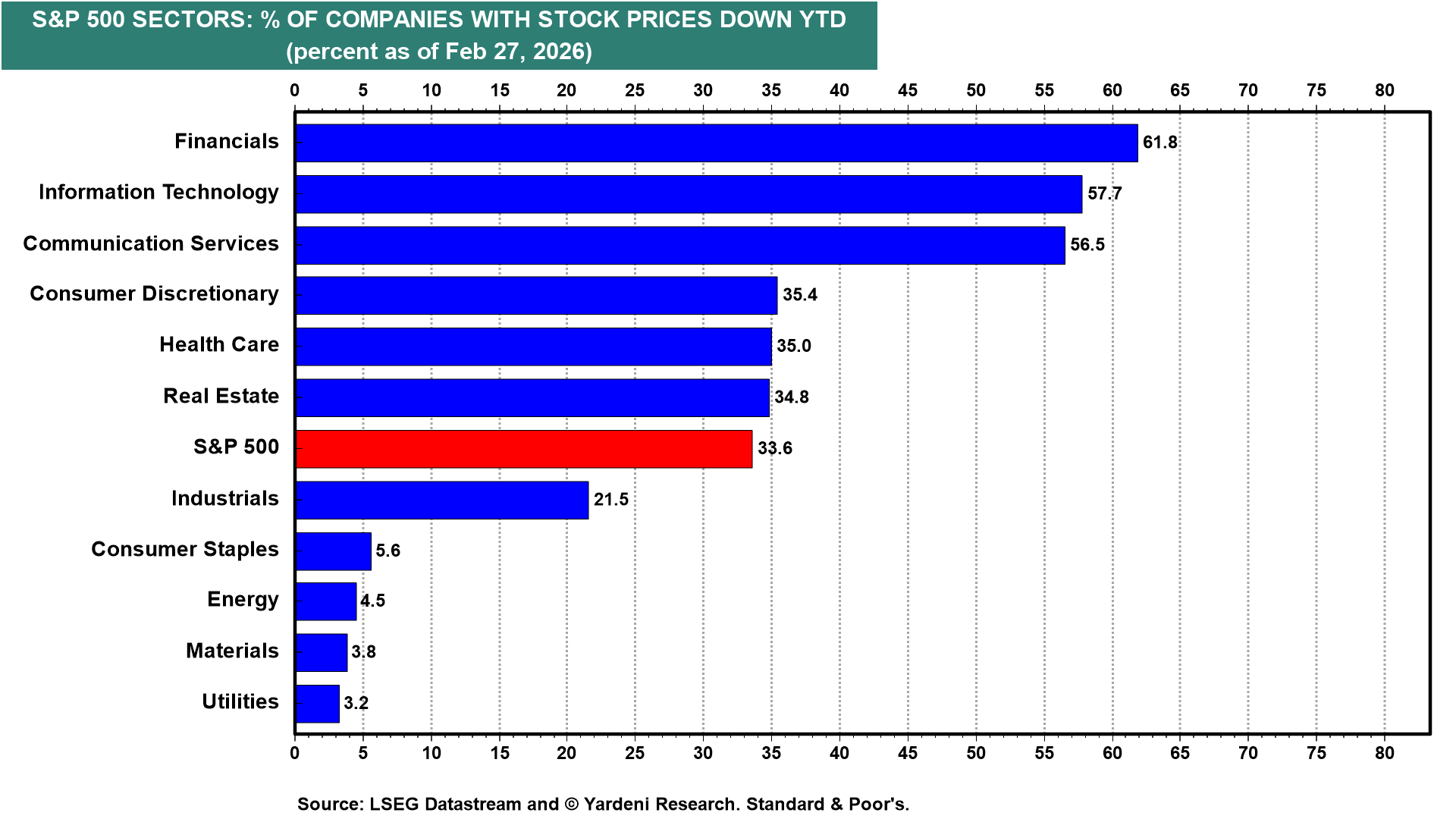

Not surprisingly, the worst (best) performing S&P 500 sectors so far this year have the highest (lowest) percentages of stock prices down ytd (chart).

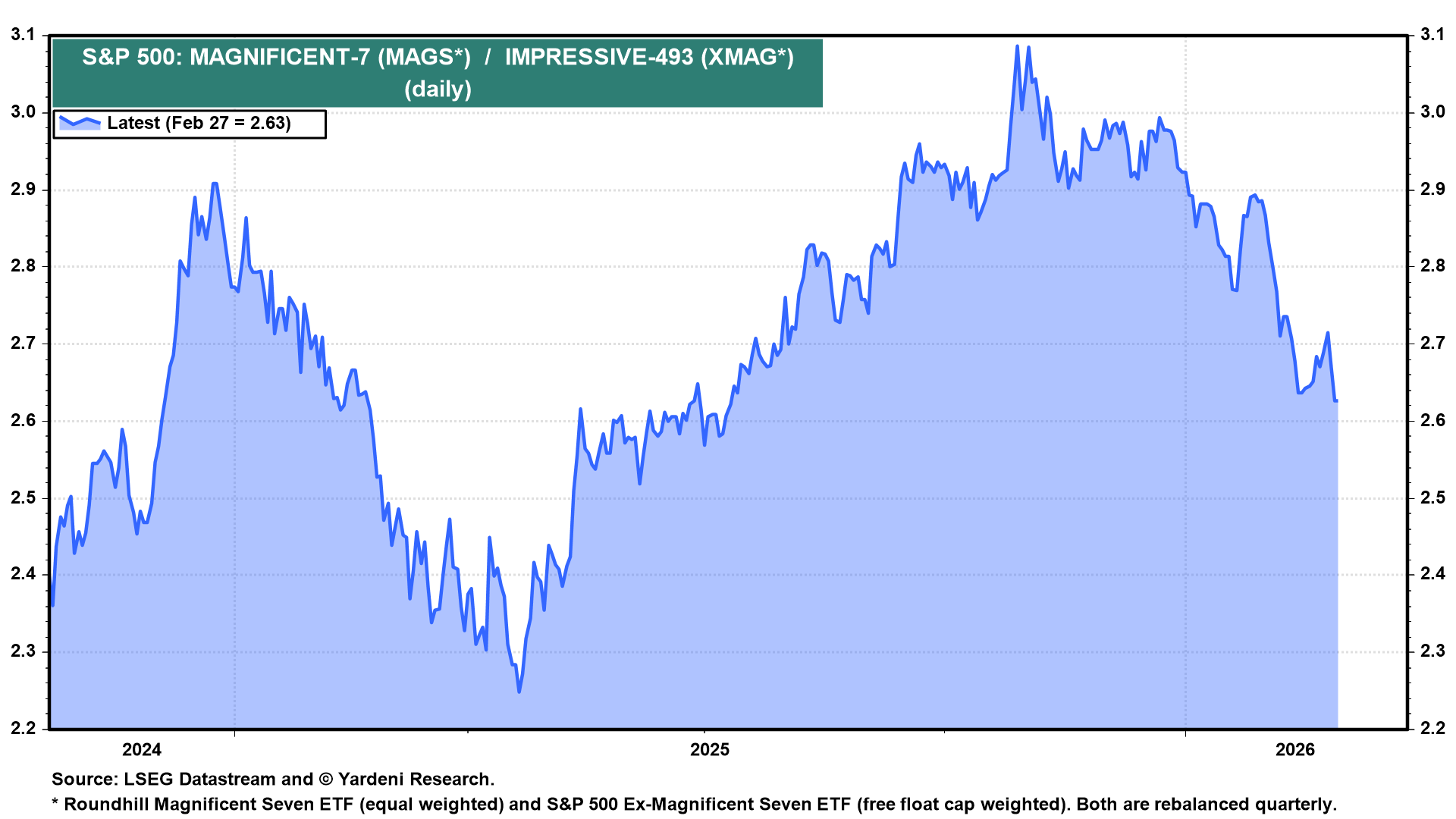

The Magnificent-7 continue to underperform the Impressive-493, as they have since late October 2025 (chart).

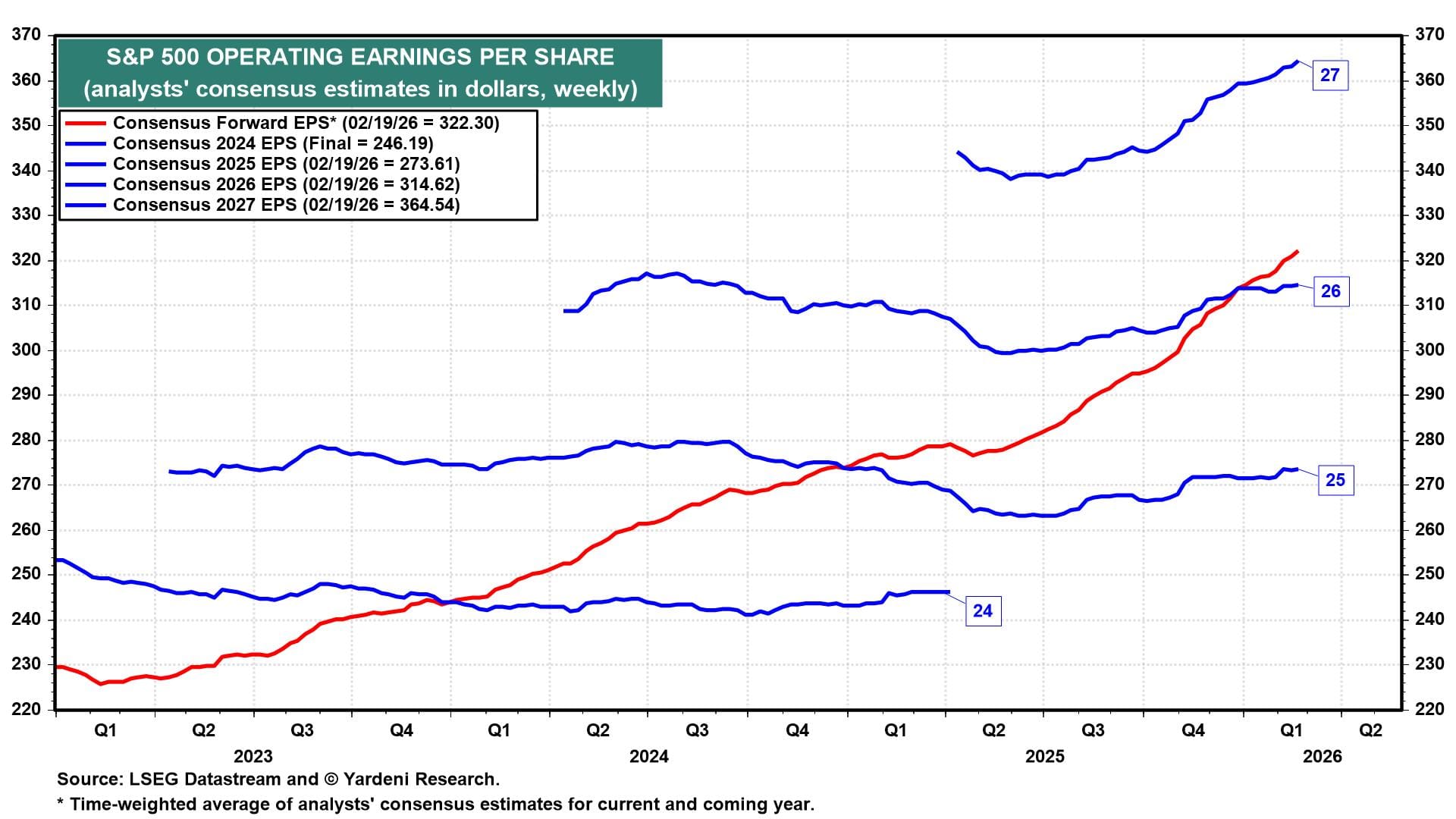

(2) Earnings. We remain bullish on the S&P 500 with our target of 7700 by the end of this year because we remain bullish on the outlook for S&P 500 earnings. Industry analysts are bullish, too. They are currently expecting earnings per share to rise to $314.62 this year (from a projected $273.61 last year) and leap to $364.54 next year (chart). We are still at $310 and $350 for this year and next, but will likely raise our targets soon after we get the final results for Q4-2025.

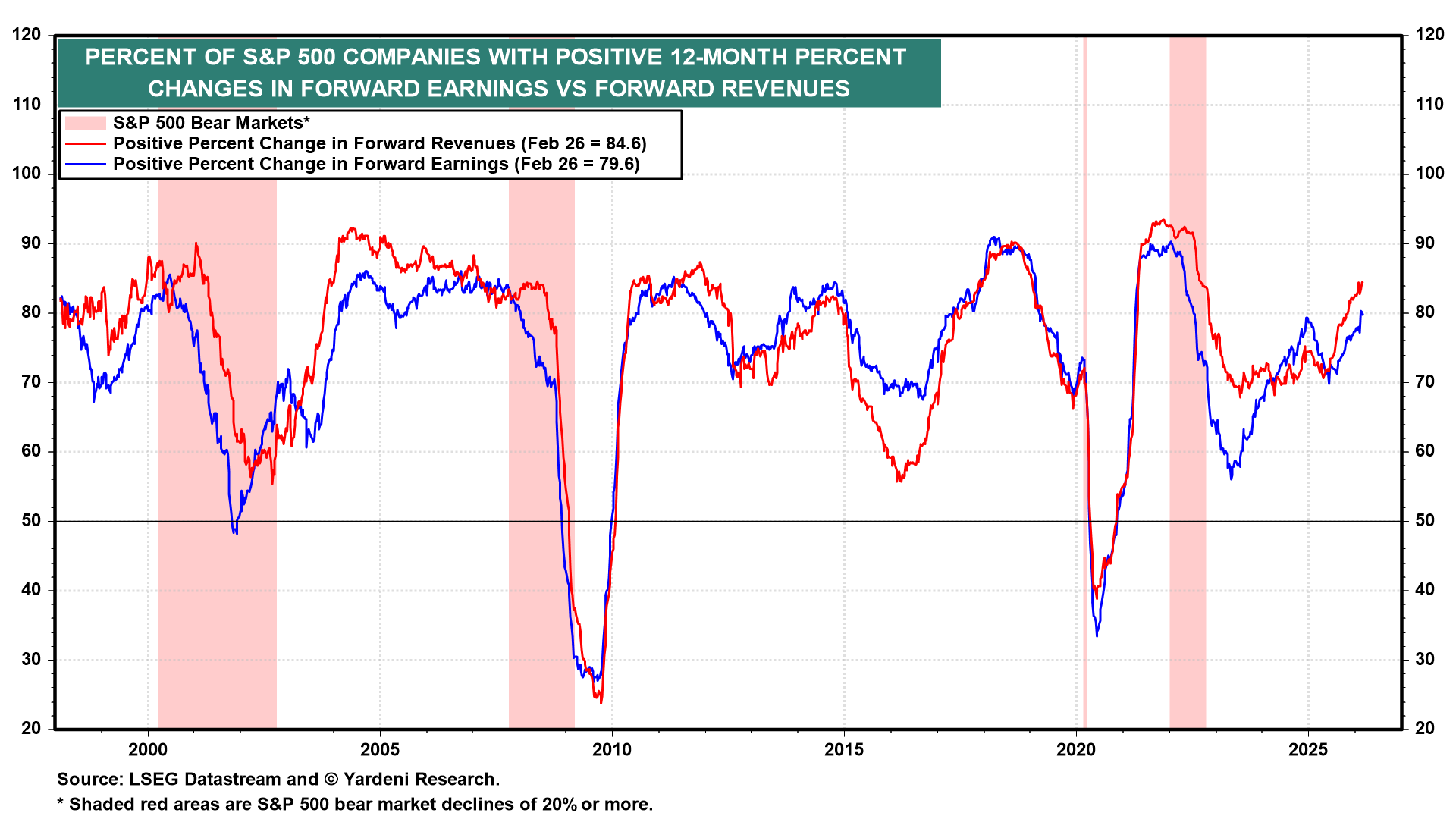

The breadth of positive 12-month percent changes in both S&P 500 forward revenues and forward earnings continues to improve (chart).

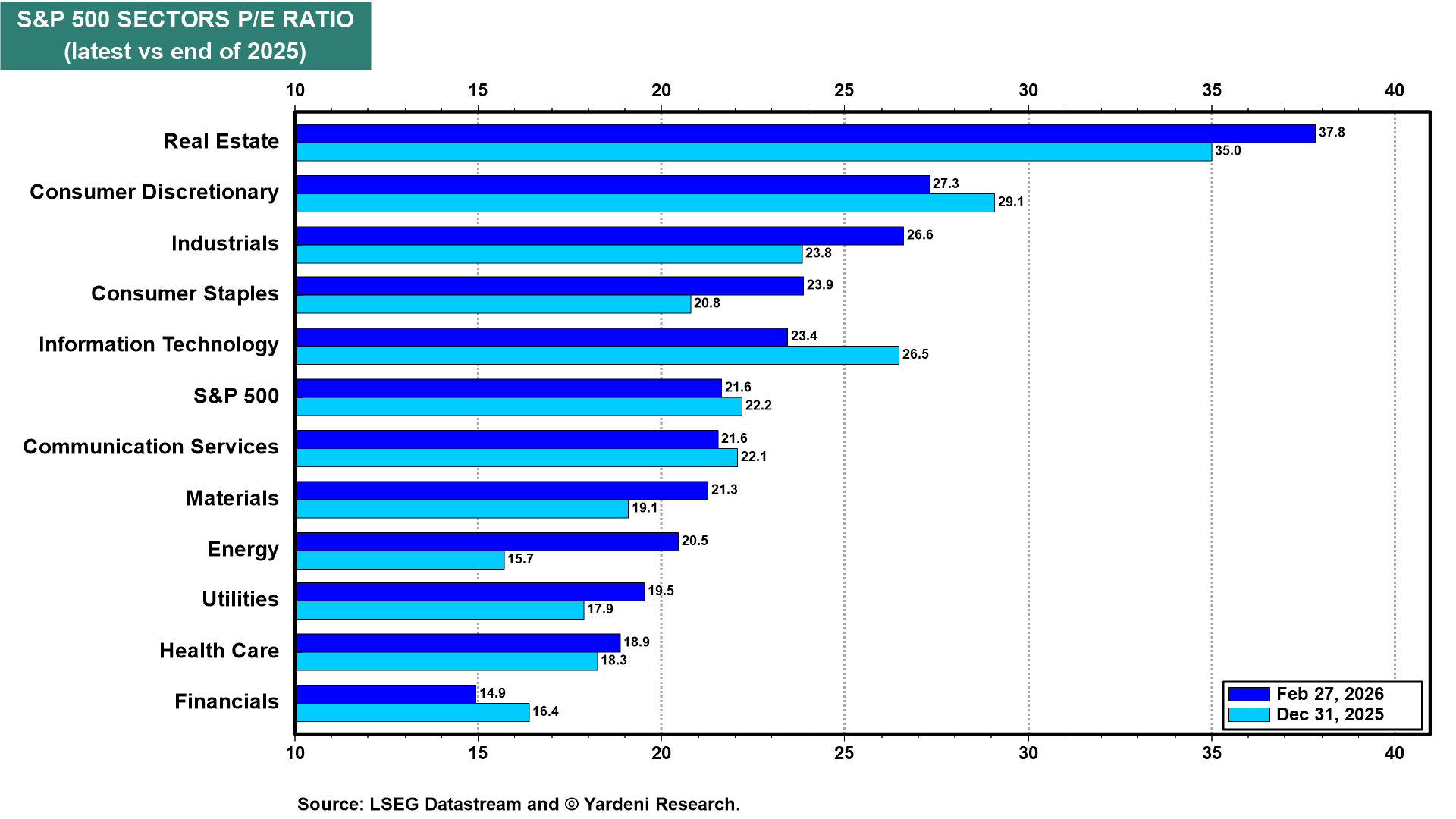

(3) Valuation. The Great Rotation of the Roaring 2020s started late last year, just as we predicted on December 7. That’s clearly visible by comparing the forward P/Es of the 11 sectors of the S&P 500 now and at the end of 2025 (chart). The valuation multiples of last year’s outperformers have come down, while those of last year’s laggards have increased. As a result, the forward P/E of the S&P 500 is only down to 21.6 from 22.2.

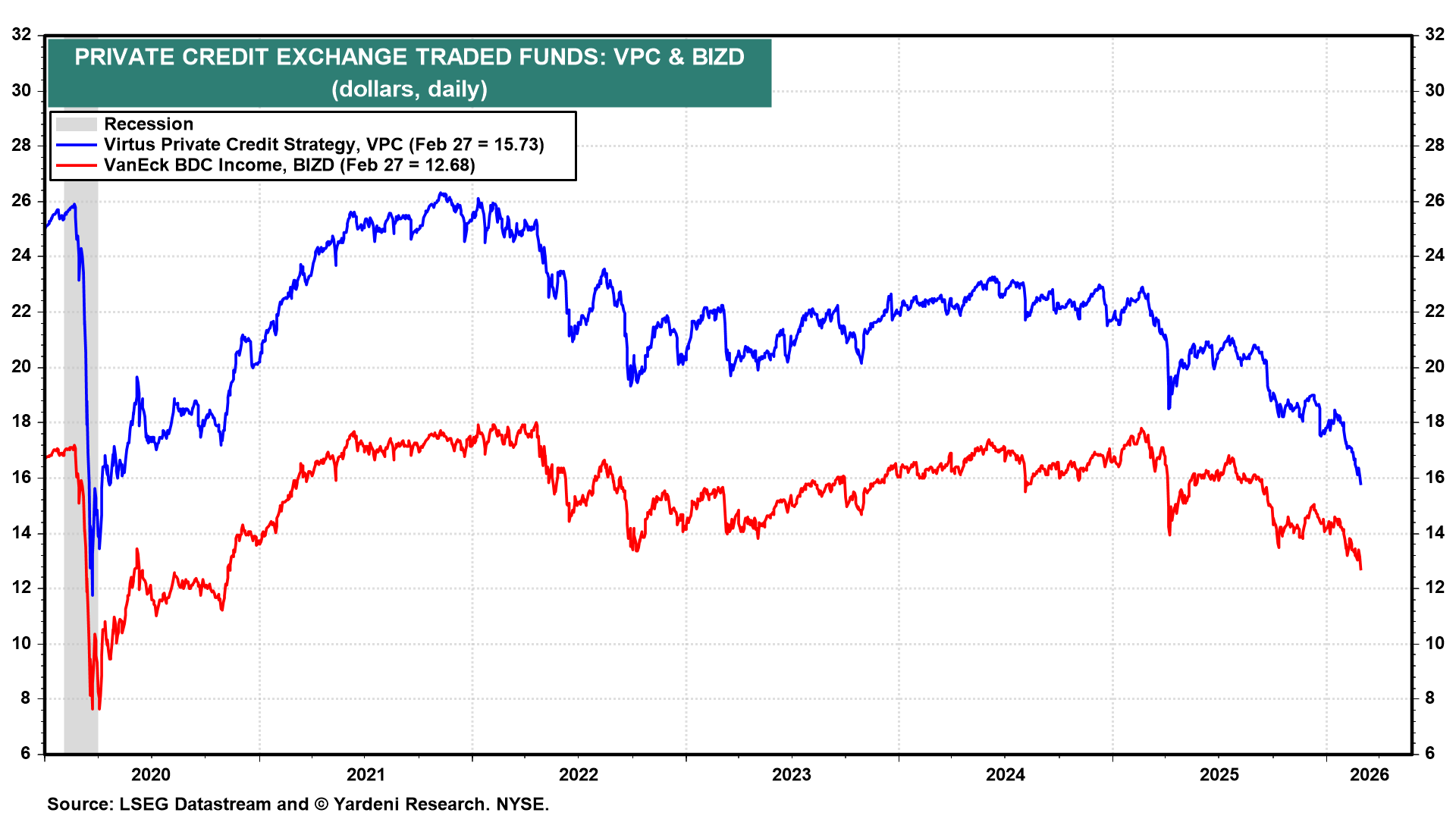

(4) Credit. The prices of private credit ETFs continue to fall (chart). This is certainly weighing on the S&P 500 Financials sector. It is a problem, but we don’t think it has the potential to cause an economy-wide credit crunch, a recession, or a bear market. But we are on guard.

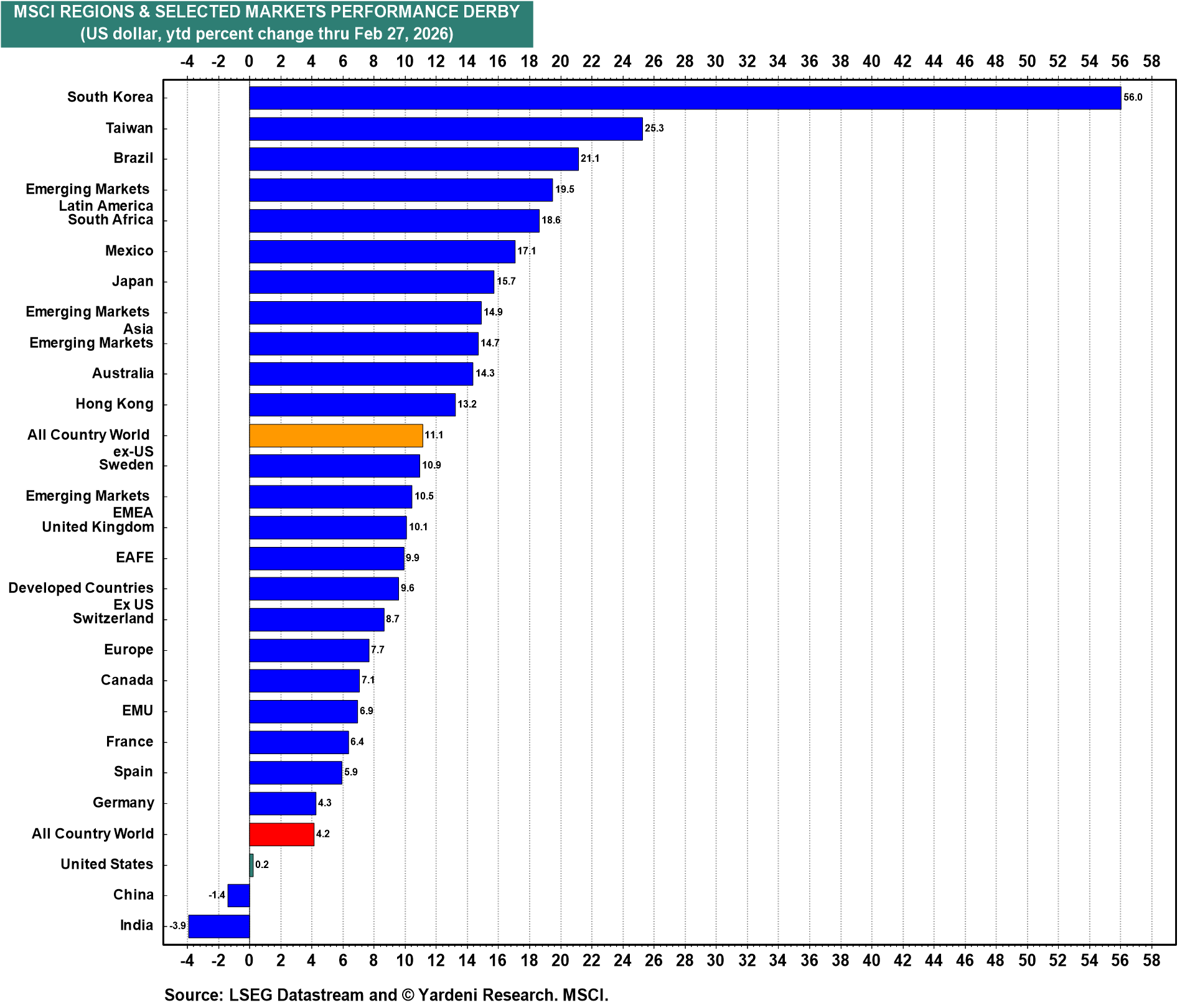

(5) Global equities. Go Global continues to outperform Stay Home so far this year as it did last year (chart).

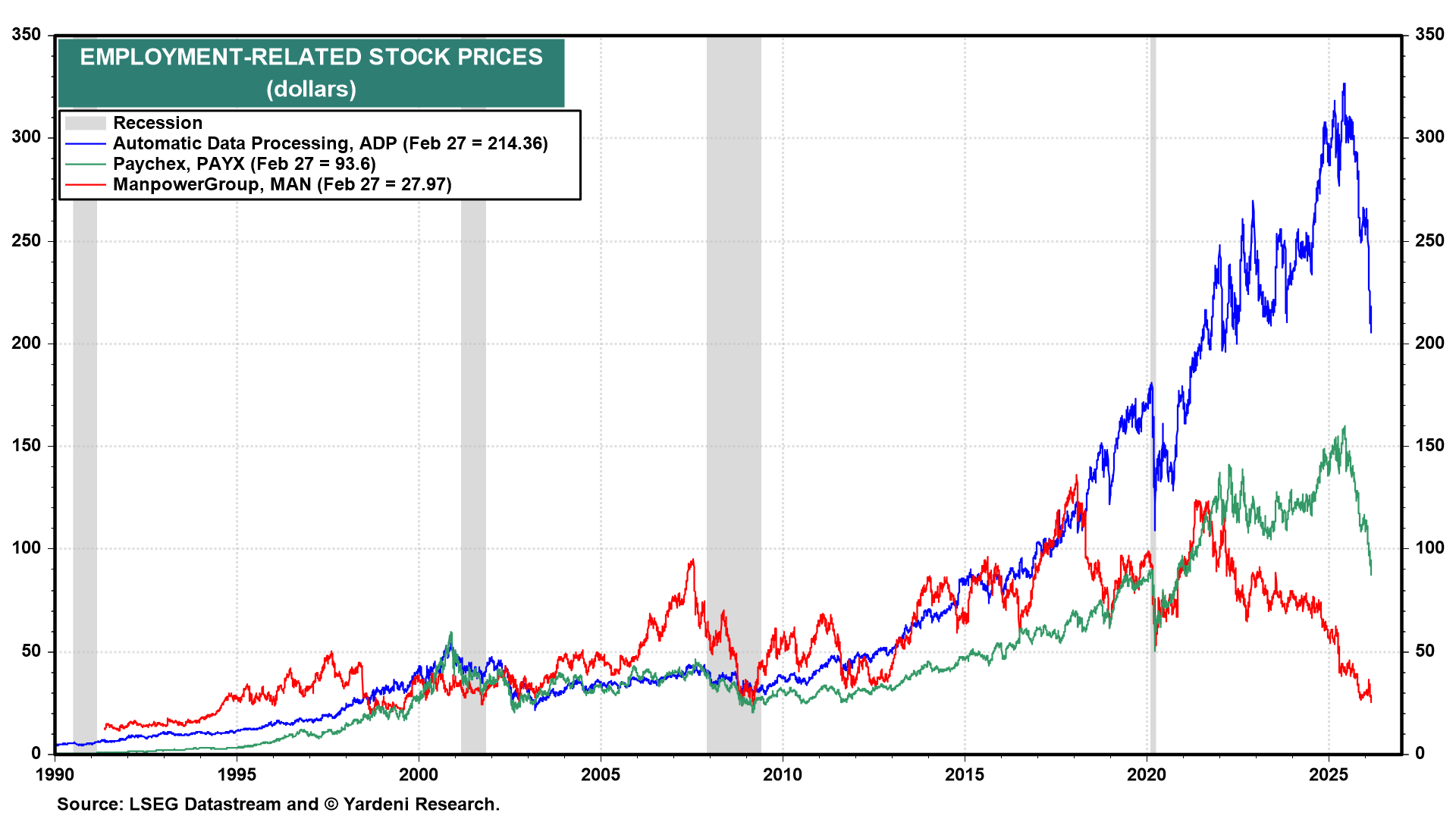

(6) Employment. In addition to private credit concerns, investors are worried that AI will destroy jobs. Friday’s stock market weakness was partly attributable to Block announcing a 4,000-worker cut (more than 40% of its workforce) due to AI. The stock prices of employment-related companies continued to plunge on the news (chart).

💡

Join the discussion with Ed below! To leave comments or questions, log in to the Yardeni QuickTakes website and post them at the end of the QuickTakes article. Paid members’ contributions may be featured in our segment, “Ed Answers Your Questions”.