According to data compiled by the Gasgoo Automotive Research Institute, in 2025, China’s automotive intelligent components market further intensified its concentration and localization trends, with technology iteration and ecosystem integration becoming increasingly prominent. Traditional Tier-1 suppliers, tech companies, automakers’ in-house R&D, and emerging supply chain players competed across multiple dimensions and scenarios, driving the industry toward a clearer tiered structure, deeper ecosystem coupling, and differentiated innovation. This evolution strengthens the foundation for long-term growth in the smart cockpit sector while making the market ecosystem more dynamic and diverse.

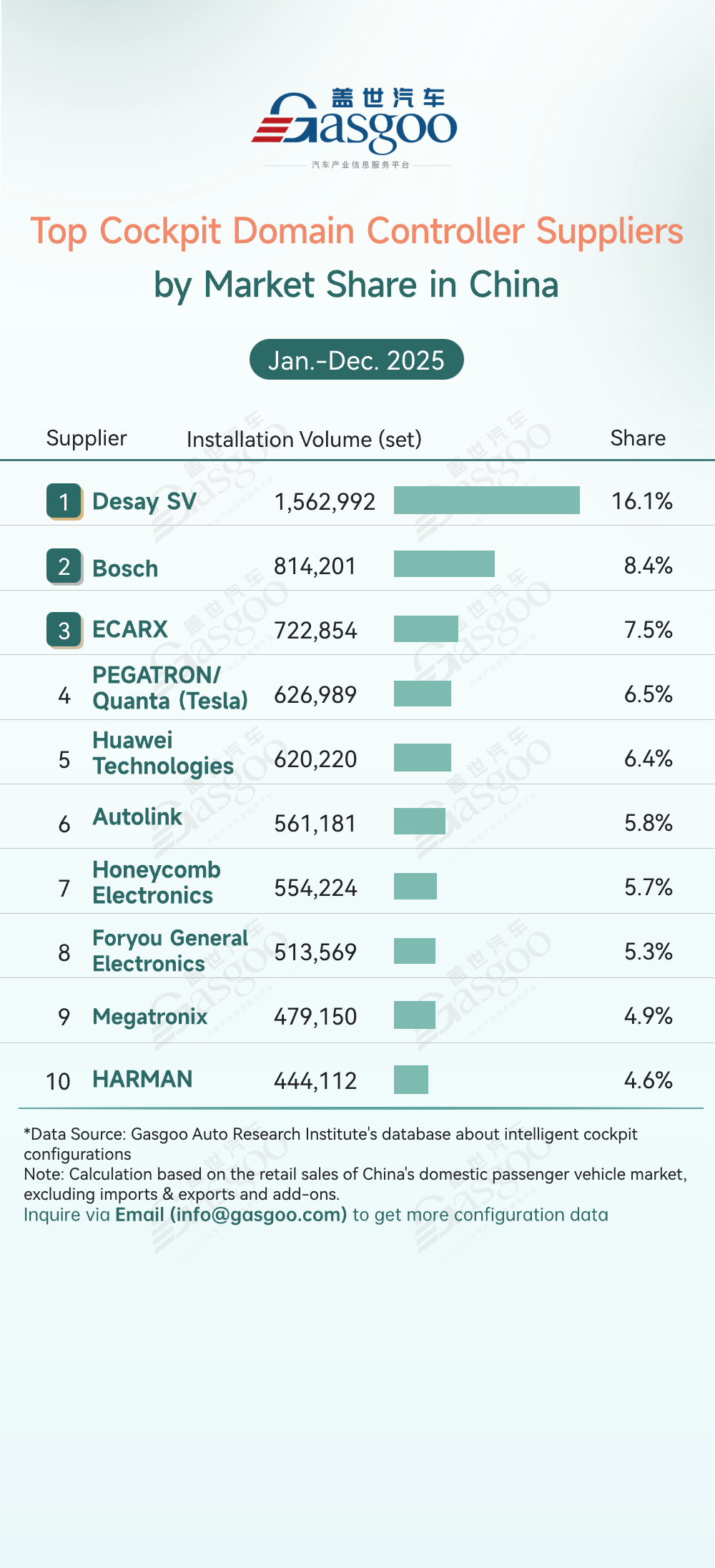

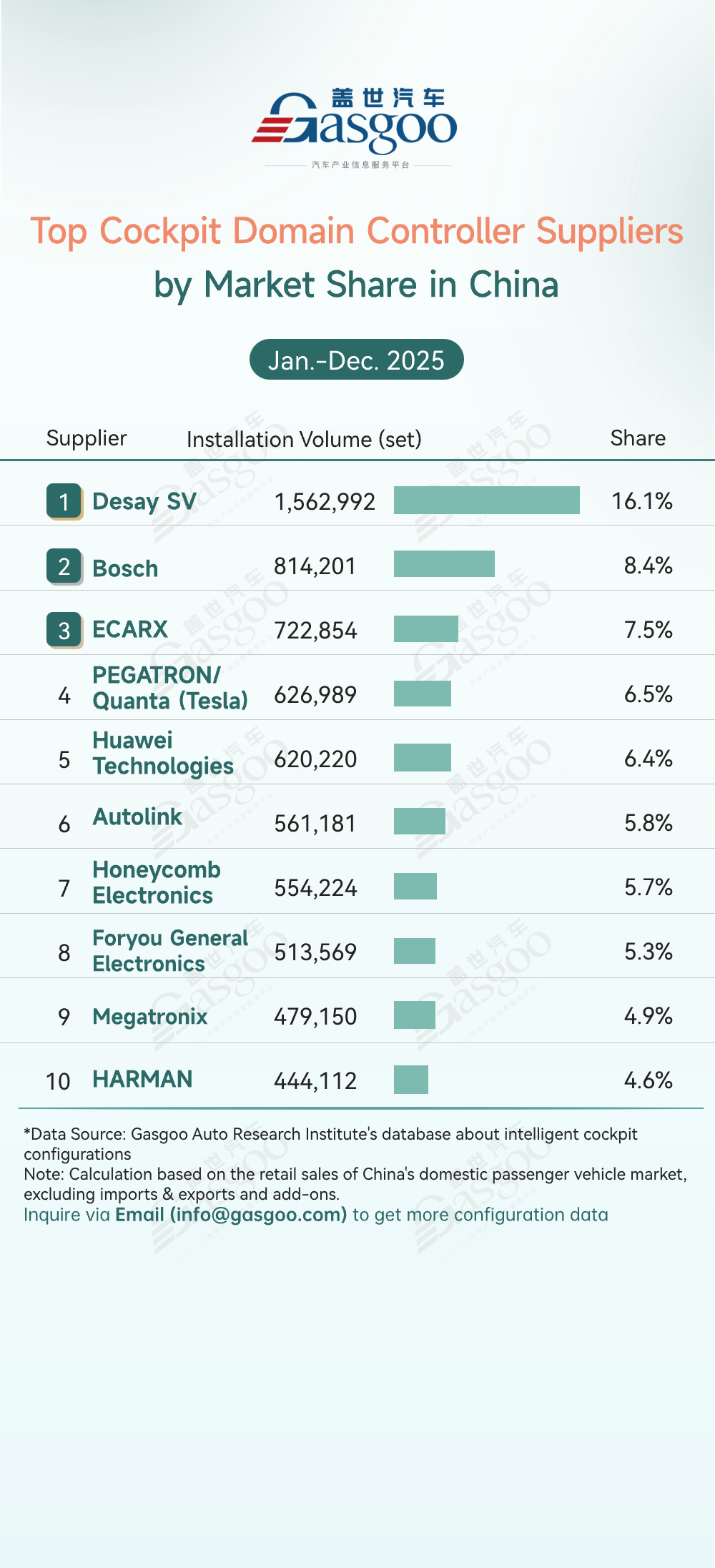

Top cockpit domain controller suppliers

Desay SV: 1,562,992 sets installed, 16.1% share

Bosch: 814,201 sets installed, 8.4% share

ECARX: 722,854 sets installed, 7.5% share

PEGATRON/Quanta (Tesla): 626,989 sets installed, 6.5% share

Huawei Technologies: 620,220 sets installed, 6.4% share

Autolink: 561,181 sets installed, 5.8% share

Honeycomb Electronics: 554,224 sets installed, 5.7% share

Foryou General Electronics: 513,569 sets installed, 5.3% share

Megatronix: 479,150 sets installed, 4.9% share

HARMAN: 444,112 sets installed, 4.6% share

In 2025, the cockpit domain controller market accelerated its growth, with domestic suppliers further consolidating their leading position. Desay SV took the lead strongly with over 1.56 million sets installed (16.1% share), further expanding its top-tier advantage. Bosch followed with an 8.4% share, together forming the market’s first tier. ECARX, PEGATRON/Quanta (Tesla), and Huawei Technologies maintained stable performance, each holding 6–8% market share. The involvement of PEGATRON and Quanta in Tesla’s supply chain, combined with tech players like Huawei, further diversified market competition. Autolink, Honeycomb Electronics, Foryou General Electronics, Megatronix, and HARMAN ranked sixth to tenth, with shares concentrated between 4.6% and 5.8%, reflecting intense competition at this tier.

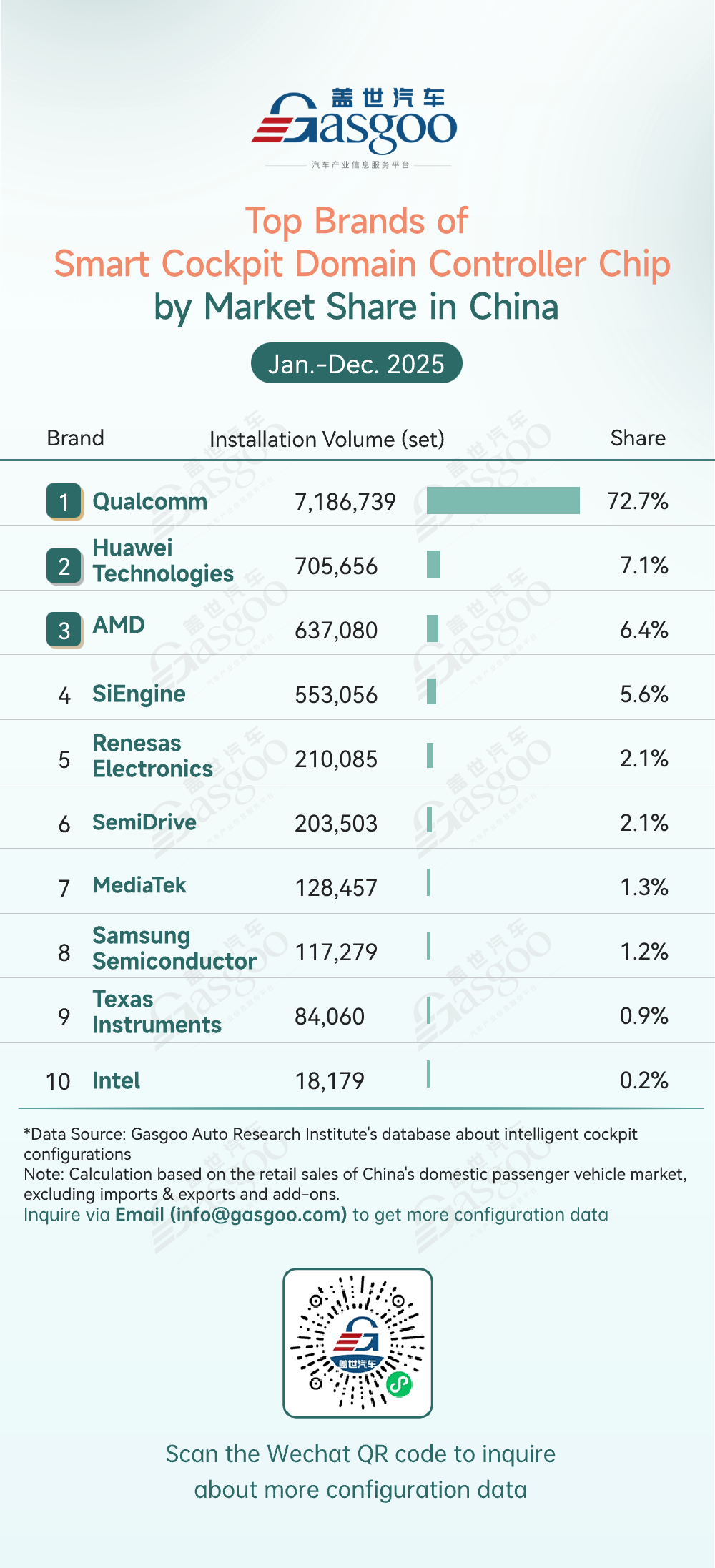

Top brands of smart cockpit domain controller chip

Qualcomm: 7,186,739 units installed, 72.7% share

Huawei Technologies: 705,656 units installed, 7.1% share

AMD: 637,080 units installed, 6.4% share

SiEngine: 553,056 units installed, 5.6% share

Renesas Electronics: 210,085 units installed, 2.1% share

SemiDrive: 203,503 units installed, 2.1% share

MediaTek: 128,457 units installed, 1.3% share

Samsung Semiconductor: 117,279 units installed, 1.2% share

Texas Instruments: 84,060 units installed, 0.9% share

Intel: 18,179 units installed, 0.2% share

In 2025, the cockpit domain controller chip market continued to be highly concentrated, with China’s local chipmakers steadily increasing their share. Qualcomm remained first with over 7.18 million units installed (72.7% share), maintaining clear advantages in technology maturity and supply chain scale. Meanwhile, China’s local players continued to gain momentum: Huawei Technologies held 7.1% as the second-largest supplier, while SiEngine and SemiDrive achieved growth in both installation volume and market share, highlighting China’s chipmakers’ technological breakthroughs and commercial deployment capabilities in the in-vehicle domain controller chip sector.

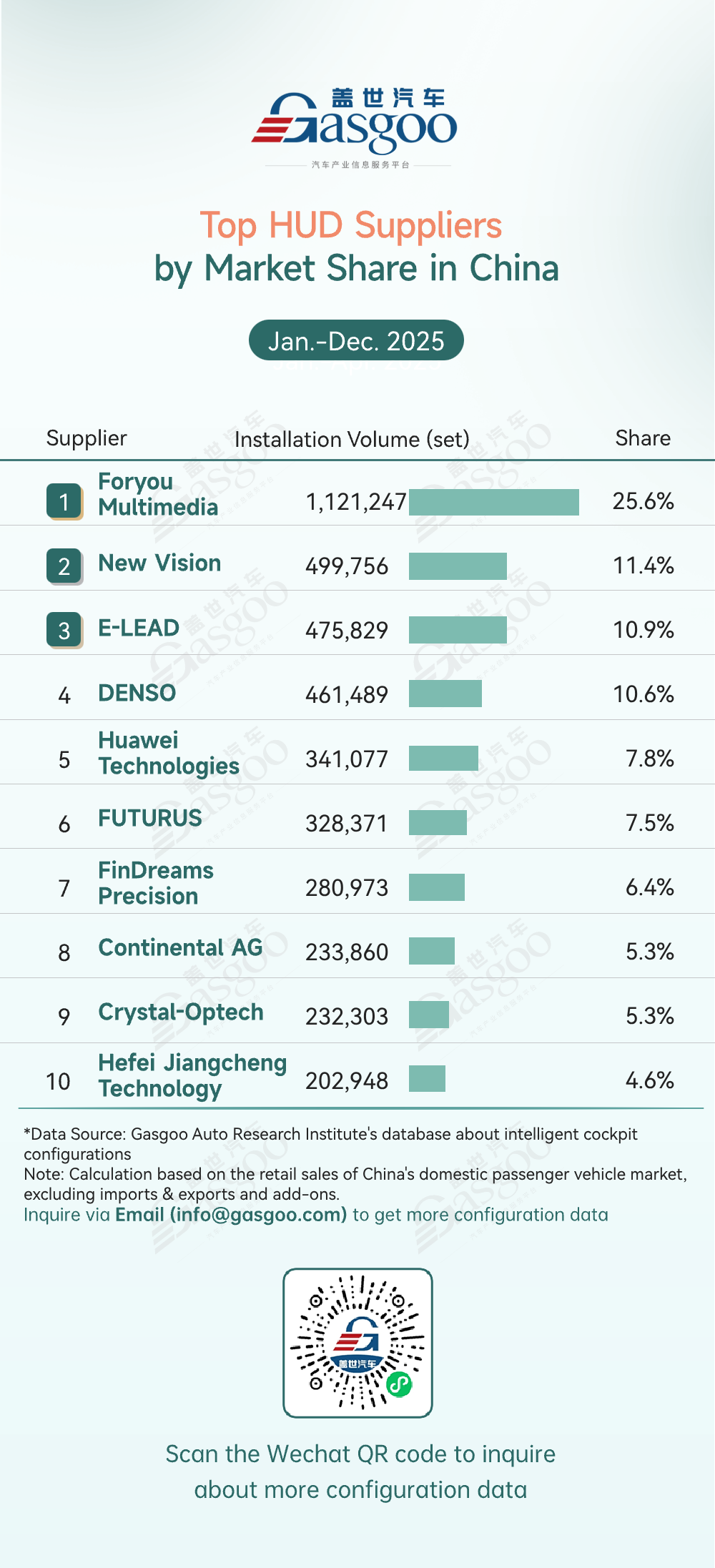

Top HUD suppliers

Foryou Multimedia: 1,121,247 sets installed, 25.6% share

New Vision: 499,756 sets installed, 11.4% share

E-LEAD: 475,829 sets installed, 10.9% share

DENSO: 461,489 sets installed, 10.6% share

Huawei Technologies: 341,077 sets installed, 7.8% share

FUTURUS: 328,371 sets installed, 7.5% share

FinDreams Precision: 280,973 sets installed, 6.4% share

Continental AG: 233,860 sets installed, 5.3% share

Crystal-Optech: 232,303 sets installed, 5.3% share

Hefei Jiangcheng Technology: 202,948 sets installed, 4.6% share

In 2025, HUD adoption expanded the in-vehicle display market, led by domestic suppliers. Foryou Multimedia topped the market with over 1.12 million sets installed (25.6% share). New Vision, E-LEAD, and DENSO followed with 10–11% share. Huawei Technologies, FUTURUS, and FinDreams Precision competed alongside international Tier-1s like Continental AG, showing the market’s diverse makeup. HUD suppliers must continue advancing AR-HUD technology, vehicle integration, and scalable delivery.

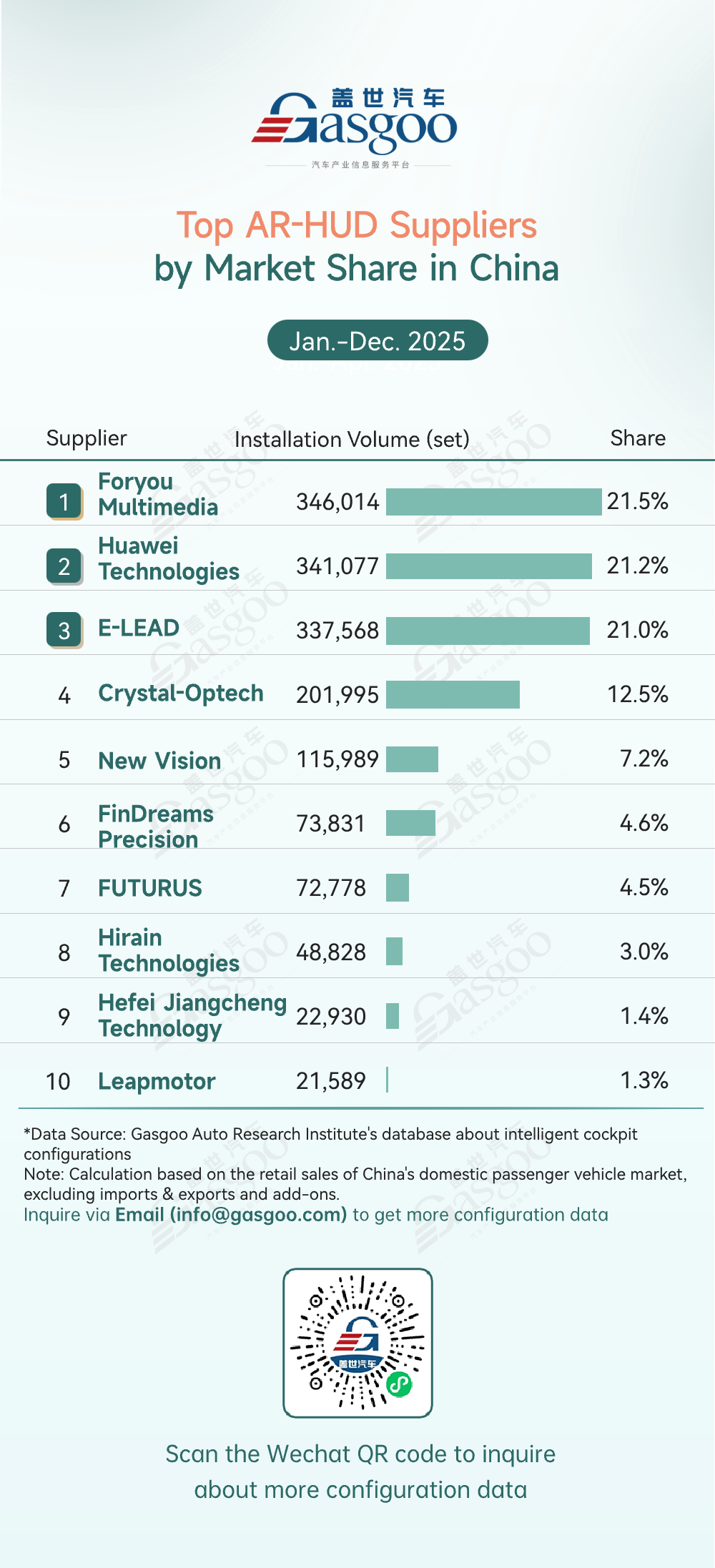

Top AR-HUD suppliers

Foryou Multimedia: 346,014 sets installed, 21.5% share

Huawei Technologies: 341,077 sets installed, 21.2% share

E-LEAD: 337,568 sets installed, 21.0% share

Crystal-Optech: 201,995 sets installed, 12.5% share

New Vision: 115,989 sets installed, 7.2% share

FinDreams Precision: 73,831 sets installed, 4.6% share

FUTURUS: 72,778 sets installed, 4.5% share

Hirain Technologies: 48,828 sets installed, 3.0% share

Hefei Jiangcheng Technology: 22,930 sets installed, 1.4% share

Leapmotor: 21,589 sets installed, 1.3% share

In 2025, China’s local suppliers continued to deepen their presence in the AR-HUD segment, driving rapid technology adoption. Foryou Multimedia led the pack with 346,014 sets installed (21.5% share), followed closely by Huawei Technologies (21.2%) and E-LEAD (21.0%), together capturing over 63% of the market. This highlights Chinese players’ strength in mass production and market expansion, making them key drivers of AR-HUD adoption. Crystal-Optech ranked fourth with 12.5% share, while New Vision and FinDreams Precision focused on niche applications and ecosystem integration. The entry of Leapmotor added a new dimension, further enriching competition in the AR-HUD market.

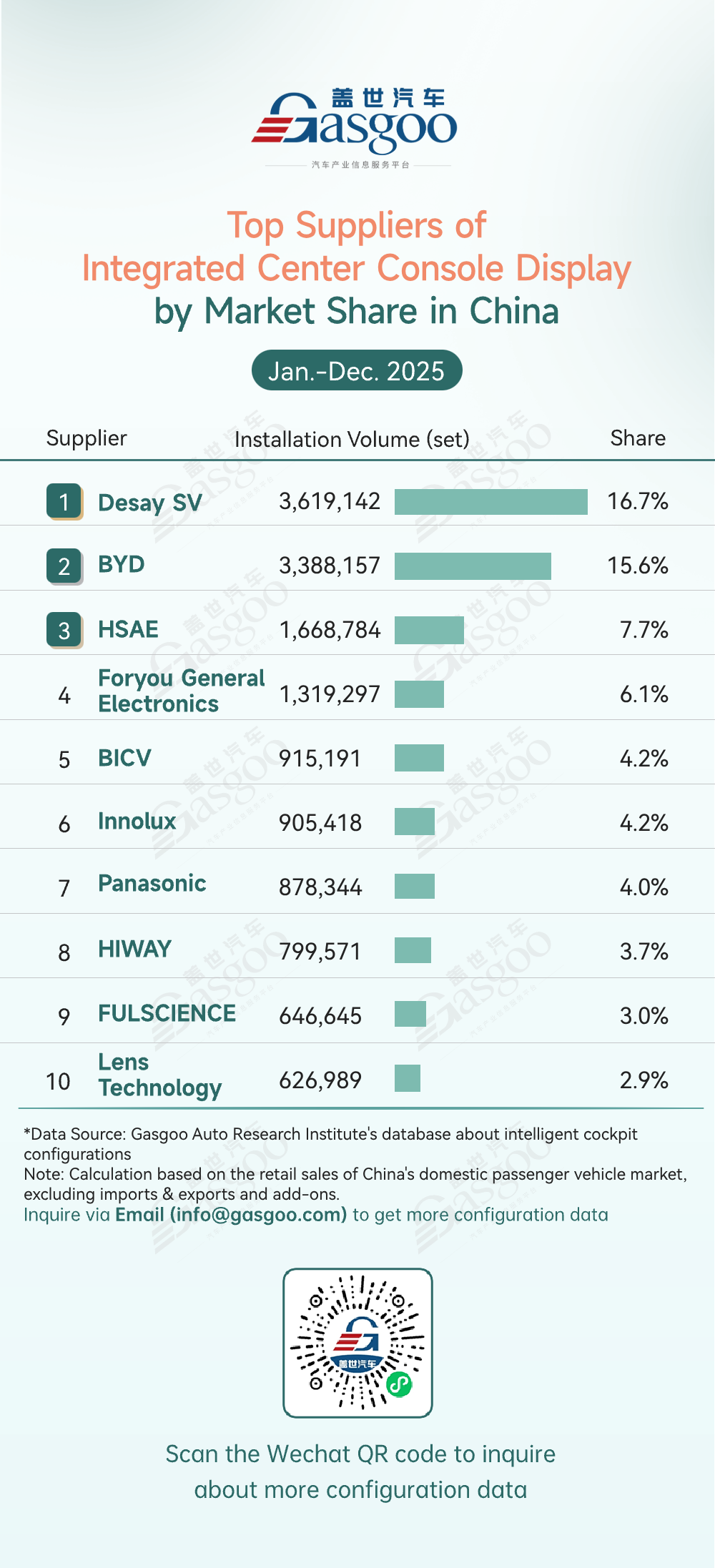

Top suppliers of integrated center console display

Desay SV: 3,619,142 sets installed, 16.7% share

BYD: 3,388,157 sets installed, 15.6% share

HSAE: 1,668,784 sets installed, 7.7% share

Foryou General Electronics: 1,319,297 sets installed, 6.1% share

BICV: 915,191 sets installed, 4.2% share

Innolux: 905,418 sets installed, 4.2% share

Panasonic: 878,344 sets installed, 4.0% share

HIWAY: 799,571 sets installed, 3.7% share

FULSCIENCE: 646,645 sets installed, 3.0% share

Lens Technology: 626,989 sets installed, 2.9% share

In 2025, the integrated center console display market was further dominated by domestic suppliers. Desay SV led the pack with over 3.61 million sets installed (16.7% share), maintaining a strong top-tier position. BYD followed closely with over 3.38 million sets (15.6% share), together capturing more than 32% of the market as the “top domestic duo” in central display integration. HSAE ranked third with 1.67 million sets (7.7% share), demonstrating solid competitiveness, while Foryou General Electronics closely trailed with 6.1%, forming the market’s second tier. BICV and Innolux each held 4.2%, reflecting intense competition.

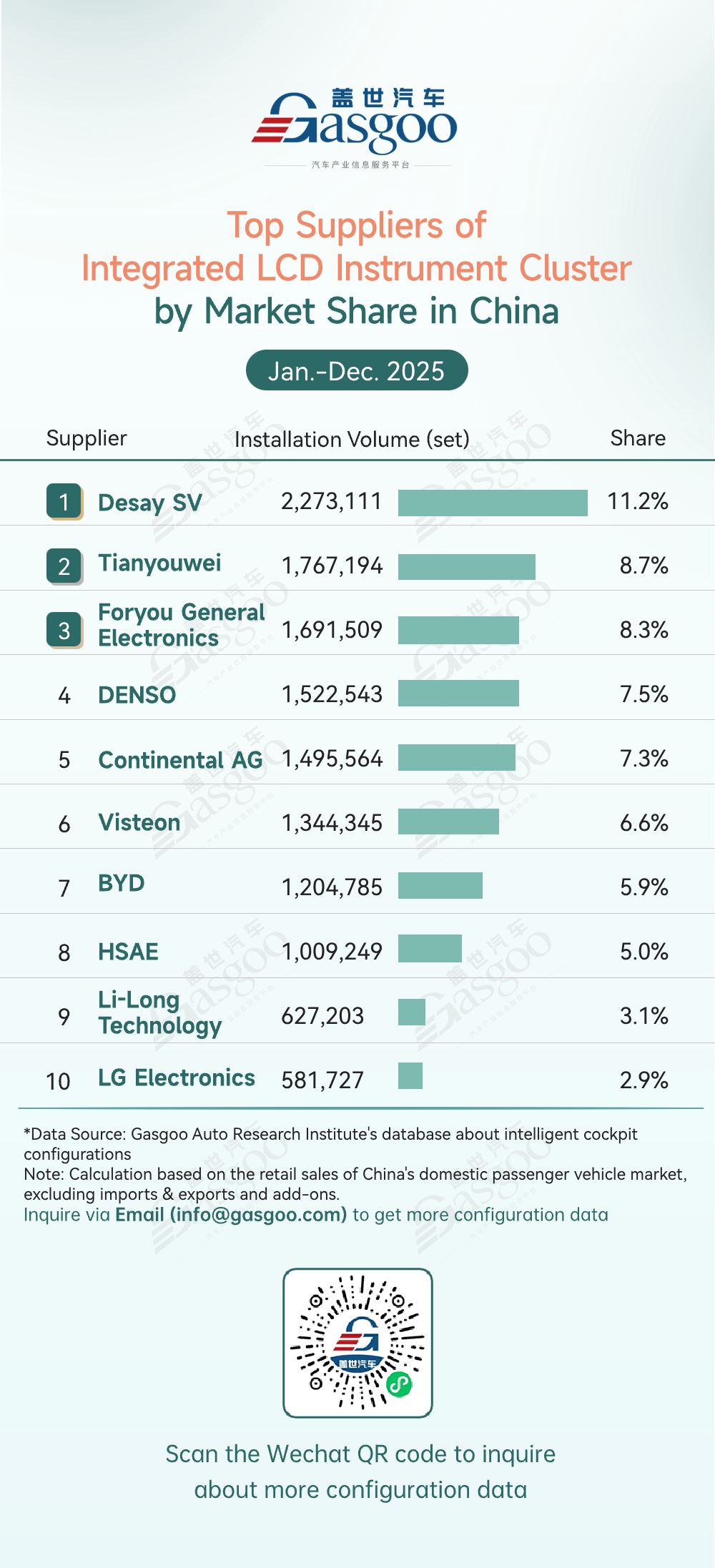

Top suppliers of integrated LCD instrument cluster

Desay SV: 2,273,111 sets installed, 11.2% share

Tianyouwei: 1,767,194 sets installed, 8.7% share

Foryou General Electronics: 1,691,509 sets installed, 8.3% share

DENSO: 1,522,543 sets installed, 7.5% share

Continental AG: 1,495,564 sets installed, 7.3% share

Visteon: 1,344,345 sets installed, 6.6% share

BYD: 1,204,785 sets installed, 5.9% share

HSAE: 1,009,249 sets installed, 5.0% share

Li-Long Technology: 627,203 sets installed, 3.1% share

LG Electronics: 581,727 sets installed, 2.9% share

In 2025, the integrated LCD instrument cluster market was highly competitive, with China’s local suppliers increasingly dominant. Desay SV led the pack with over 2.27 million sets installed (11.2% share), followed by Tianyouwei (8.7%) and Foryou General Electronics (8.3%), together showing the strength of local supply chains. International Tier-1s such as DENSO, Continental AG, and Visteon held 6.6–7.5%, leveraging technical expertise but facing pressure from Chinese competitors. Other local players, including BYD and HSAE, expanded in the sub-6% segment, while Li-Long Technology and LG Electronics also ranked in the top ten, reflecting a dynamic and diversifying market landscape.

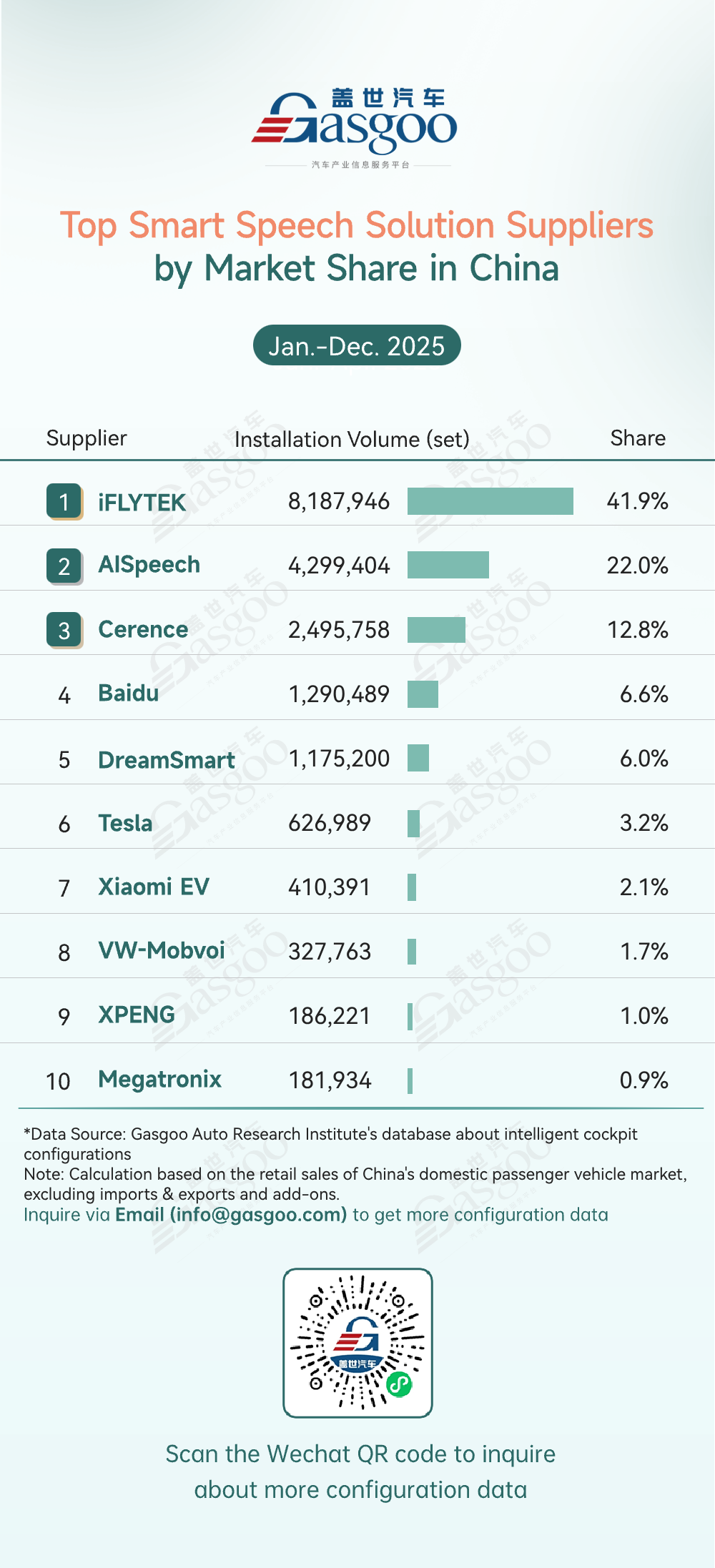

Top smart speech solution suppliers

iFLYTEK: 8,187,946 sets installed, 41.9% share

AISpeech: 4,299,404 sets installed, 22.0% share

Cerence: 2,495,758 sets installed, 12.8% share

Baidu: 1,290,489 sets installed, 6.6% share

DreamSmart: 1,175,200 sets installed, 6.0% share

Tesla: 626,989 sets installed, 3.2% share

Xiaomi EV: 410,391 sets installed, 2.1% share

VW-Mobvoi: 327,763 sets installed, 1.7% share

XPENG: 186,221 sets installed, 1.0% share

Megatronix: 181,934 sets installed, 0.9% share

In 2025, smart speech solution continued to evolve, with the market showing a clear “domestic-led, top-concentrated” pattern. iFLYTEK led the pack with 8,187,946 sets installed (41.9% share), leveraging technological expertise and ecosystem integration to establish a strong competitive edge. AISpeech followed with 4,299,404 sets (22.0% share), together capturing over 63% of the market and cementing domestic dominance. Cerence ranked third with 2,495,758 sets (12.8%), acting as an important supplement in the top tier. Baidu and DreamSmart held 6.6% and 6% respectively, with Baidu expanding voice scenarios via its internet ecosystem and DreamSmart leveraging automaker partnerships for precise deployment.

All Rights Reserved. Do not reproduce, copy and use the editorial content without permission. Contact us: autonews@gasgoo.com