As global markets experience varied economic shifts, with the Hang Seng Index recently declining by 6.53%, investors are increasingly focused on small-cap stocks in Hong Kong that may offer unique opportunities amid broader market volatility. In this environment, identifying companies with strong fundamentals and potential insider confidence can be particularly compelling for those looking to navigate the complexities of current market conditions.

Top 5 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Edianyun | NA | 0.6x | 43.44% | ★★★★★☆ |

| Vesync | 7.2x | 1.1x | -3.22% | ★★★★☆☆ |

| Lion Rock Group | 5.4x | 0.4x | 49.96% | ★★★★☆☆ |

| Ferretti | 10.9x | 0.7x | 46.95% | ★★★★☆☆ |

| Gemdale Properties and Investment | NA | 0.2x | 44.12% | ★★★★☆☆ |

| China Lesso Group Holdings | 5.9x | 0.4x | -519.95% | ★★★☆☆☆ |

| Skyworth Group | 5.7x | 0.1x | -301.94% | ★★★☆☆☆ |

| Lee & Man Paper Manufacturing | 7.3x | 0.4x | -48.66% | ★★★☆☆☆ |

| Emperor International Holdings | NA | 1.0x | 20.30% | ★★★☆☆☆ |

We’ll examine a selection from our screener results.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Vesync is a company that specializes in the design, development, and sale of smart home appliances and tools, with a market capitalization of approximately HK$2.5 billion.

Operations: The company generates revenue primarily from its Appliance & Tool segment, with recent figures reaching $604.75 million. Over the analyzed period, the gross profit margin has shown an upward trend, reaching 48.46% by mid-2024. Operating expenses are notable, particularly in sales and marketing and general administrative areas.

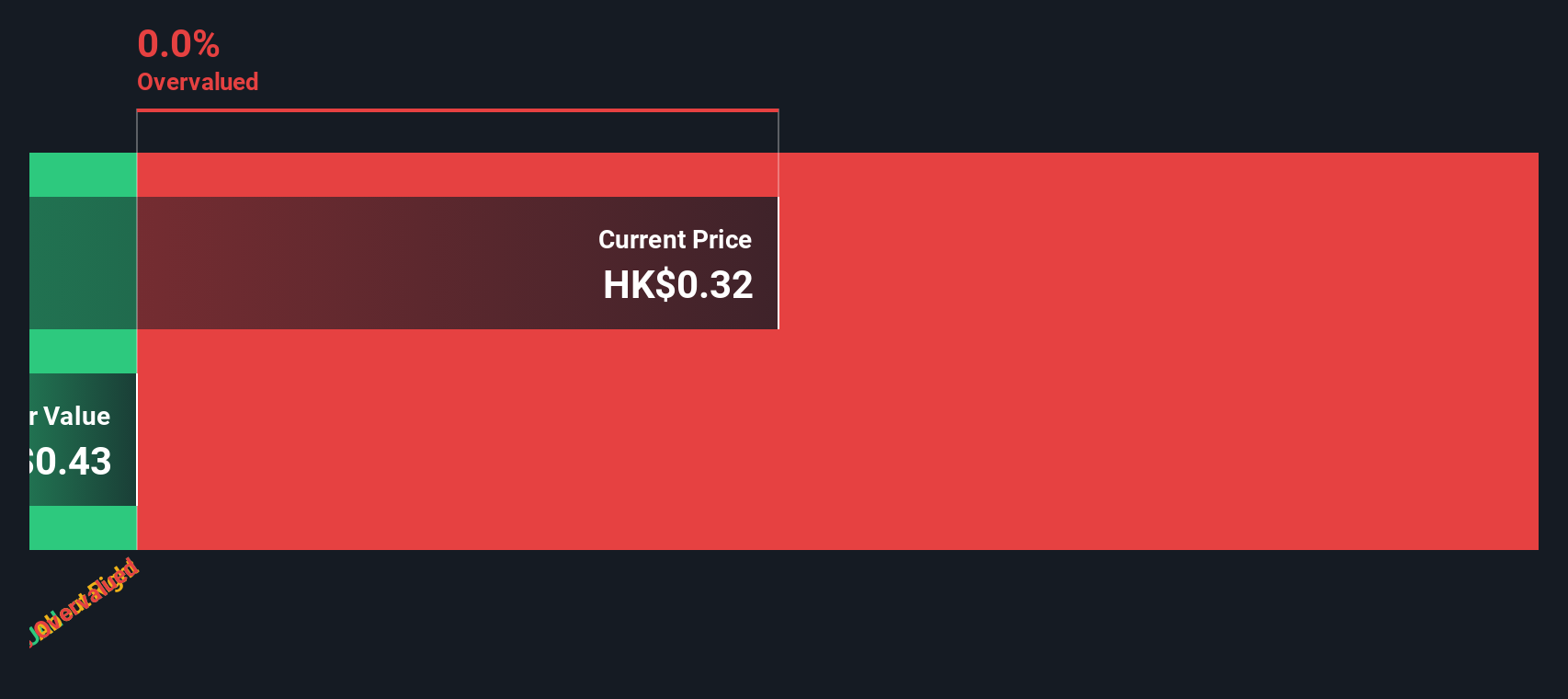

PE: 7.2x

Vesync, a Hong Kong-based company, has recently been added to the S&P Global BMI Index, signaling potential recognition in broader markets. Their sales for the first half of 2024 reached US$296 million, up from US$277 million last year, with net income climbing to US$45 million. Insider confidence is evident as Zhaojun Chen acquired 200,000 shares valued at HK$829k in early October. Despite relying on higher-risk external borrowing for funding, Vesync’s operational efficiency improvements and cost reductions have bolstered profitability.

Simply Wall St Value Rating: ★★★★☆☆

Overview: Gemdale Properties and Investment is engaged in property development, investment, and management, with a focus on residential and commercial real estate projects, and has a market capitalization of approximately HK$6.66 billion.

Operations: The company generates revenue primarily from Property Development and Property Investment and Management, with the former being the dominant contributor. In recent periods, gross profit margin has shown variability, reaching as high as 41.63% in December 2018 but declining to 0.09% by June 2024. Operating expenses have increased over time, impacting net income margins which have also fluctuated significantly, turning negative in March and June of 2024.

PE: -1.8x

Gemdale Properties and Investment, a smaller player in the Hong Kong market, has seen significant insider confidence with Lian Huat Loh acquiring 10 million shares valued at approximately RMB 2.6 million recently. Despite a challenging financial position marked by earnings not covering interest payments and reliance on external borrowing, the company reported substantial contracted sales of RMB 14.2 billion from January to September 2024. However, recent earnings showed a net loss of RMB 2.18 billion for the first half of the year due to increased impairment losses. These dynamics highlight both potential opportunities and risks for investors considering this stock within its sector context.

Simply Wall St Value Rating: ★★★★☆☆

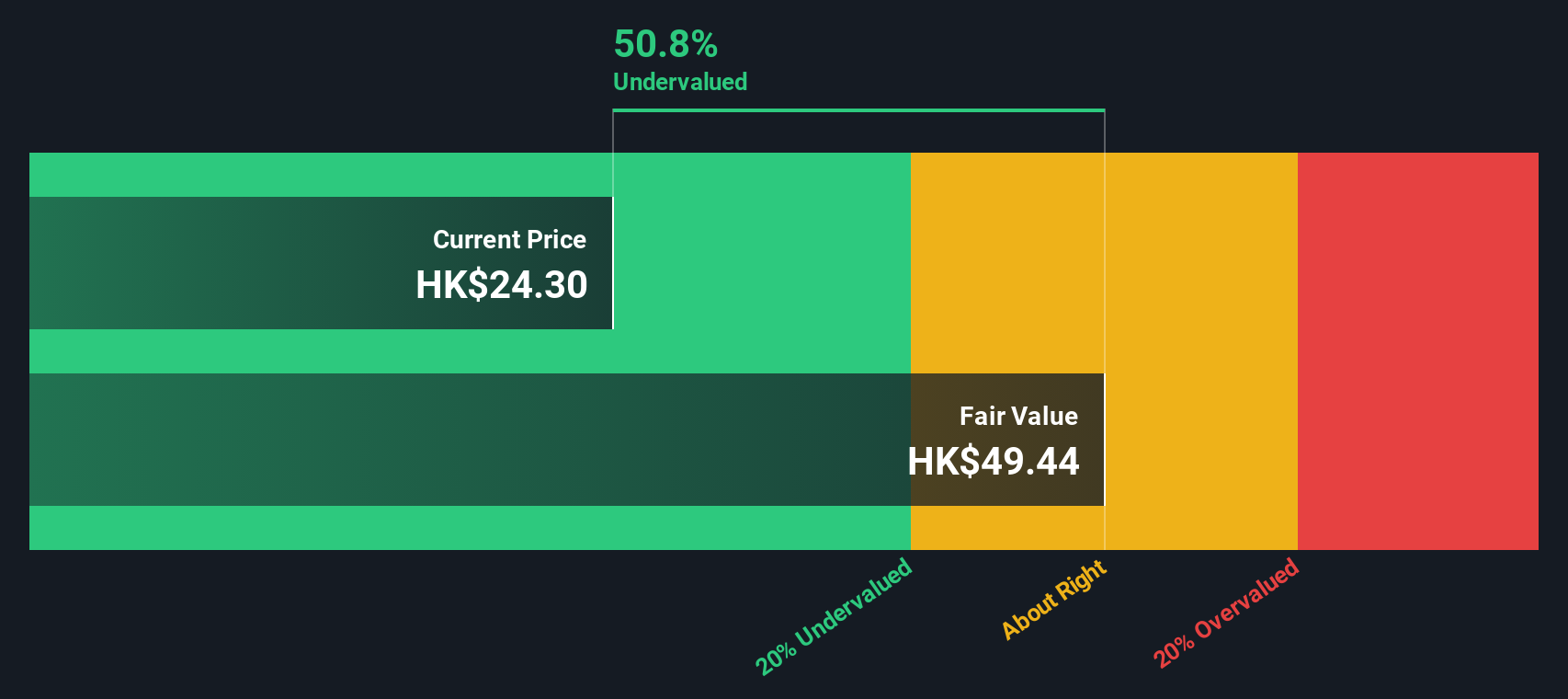

Overview: Ferretti is engaged in the design, construction, and marketing of yachts and recreational boats, with a market capitalization of HK$12.34 billion.

Operations: The company generates revenue primarily from the design, construction, and marketing of yachts and recreational boats, with a recent gross profit margin of 36.04%. Operating expenses include significant allocations to general and administrative costs.

PE: 10.9x

Ferretti, a company in the Hong Kong market, is attracting attention due to its potential for value appreciation. Despite being dropped from the S&P Global BMI Index on September 10, 2024, insider confidence remains strong with recent share purchases indicating belief in future prospects. The departure of key executives like Mr. Stefano de Vivo and Mr. Tan Xuguang hasn’t impacted operations significantly as succession plans are in place. Ferretti’s financials show positive growth with half-year sales reaching €695 million and net income at €44 million. While relying solely on external borrowing poses some risk, earnings quality remains high with forecasts predicting further growth at 12% annually.

Make It Happen

Curious About Other Options?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com