A significant shift can also be observed in the sectors that have dominated global markets. Of the U.S. listed companies in 1900, nearly 80% of their value was concentrated in sectors that are now small or have disappeared, such as railroads, textiles, iron, coal, and steel. Meanwhile, 70% of today’s U.S. companies come from sectors that were small or nonexistent in 1900. By contrast, technology and healthcare were virtually absent from stock markets in 1900.

According to the report, investors often associate new technologies with “bubbles” and subsequent periods of lower returns. However, as was the case with railroads, despite being a declining sector over the study period (falling from 63% of the U.S. market in 1900 to less than 1% today), they actually delivered returns higher than both the U.S. stock market and their more recent technological competitors since 1900.

Other Lessons from the Market

Another clear conclusion from the report is that “equities are the best-performing liquid asset.” Specifically, equities have outperformed bonds, bills, and inflation since 1900: an initial investment of $1 grew to $124,854 in nominal terms by the end of 2025. Long-term bonds and Treasury bills delivered lower returns, although they outpaced inflation. Their respective index levels at the end of 2025 were $284 and $69, while the inflation index ended at $38.

“This outperformance is not unique to the United States. The Yearbook shows that equities were the best-performing asset class in all 21 countries with continuous investment histories covered in the Yearbook. Meanwhile, bonds outperformed bills in every country except Portugal. This pattern supports one of the enduring laws of finance, the risk-return trade-off, and the idea that taking risk should entail an expected reward,” explain UBS.

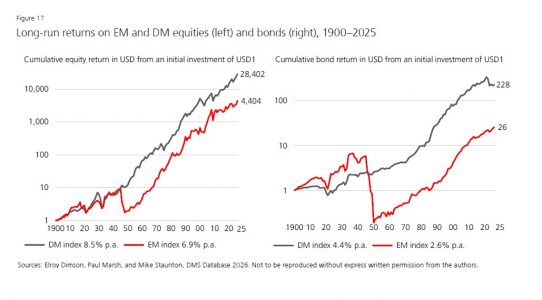

On the other hand, it is observed that developed markets have delivered better long-term results. In fact, since 1900, developed markets have recorded higher annual equity returns (8.5%) than emerging markets (6.9%). However, the report notes that “in more recent periods, emerging markets have outperformed developed ones, with an annual return of 10.9% between 1960 and 2025, compared with 9.6% for developed markets.”

Finally, the report highlights that inflation has a key impact on long-term returns. According to its analysis, although inflation in the United States has been relatively low compared with global standards—averaging 2.9% annually since 1900—its cumulative effect is highly significant: $1 in 1900 is equivalent to approximately $38 today. “Therefore, when comparing returns over time or across countries, the focus should be on real returns adjusted for inflation. In this regard, real equity returns have significantly outpaced inflation,” the report concludes.