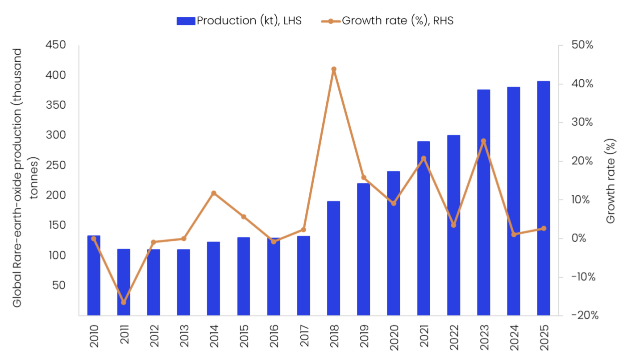

Global rare earths production is estimated to have increased by a modest 2.6% in 2025 over 2024 to 390,000 tonnes of rare-earth oxide (REO), supported by stable supply chains and sustained output from China. China retains its dominant position in the global rare earths market, accounting for 69.2% of global rare earths output in 2025. China’s dominance extends beyond mining, with the country processing nearly 90% of global rare earths, strengthening its control across the value chain.

The US and Australia are the world’s second-largest and third-largest producers, accounting for 13.1% and 7.4% of global production in 2025, respectively.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The US reinforced its position as the world’s second-largest rare earths producer in 2025, with output reaching 51,000t. This was supported by federal initiatives such as the Defense Production Act (DPA), which helped mobilise funding and long-term offtake arrangements to expand the Mountain Pass mine and build out domestic separation capacity. However, despite rapid gains in mining, the US remains at an early stage in developing commercial-scale refining capability, leaving it short of the end-to-end capacity needed for full supply-chain independence.

Meanwhile, Australia produced 29,000t and is increasingly focusing on downstream processing and magnet supply chains through government-backed critical minerals programs and partnerships with the US and Japan.

Myanmar contributed 22,000t, rebounding from earlier disruptions caused by armed conflicts and logistical issues. However, production remains volatile due to regulatory uncertainty, environmental scrutiny and intermittent border controls, keeping Myanmar a high-risk but essential supplier.

While Thailand is not a major player, it has a niche role in the industry, particularly in downstream processing (and mainly relies on imports from China). While it has limited domestic reserves, it functions as a processing hub for refining rare earths. Thailand has a developed downstream processing industry for REEs that includes the production of rare earth magnets and other high-value products. The country’s mine output doubled from 2,100t in 2024 to 4,800t in 2025, underpinned by intensified domestic mining due to the presence of reserves in the Northeastern region (particularly Nakhon Ratchasima (Korat) and Buriram region).

Nigeria’s rare earths output is estimated to have declined significantly from 7,200t in 2023 to 1,500t in 2025, due to the lack of extensive geological surveys, along with the technical challenges of extracting rare earth elements, which have limited progress. The country is planning to develop its rare earths sector through collaborations with other countries, the most recent one being the memorandum of understanding (MoU) with France in December 2024 to secure supply chains for rare earths by leveraging France’s technological expertise.

While emerging producers such as Nigeria and Thailand are adding incremental volumes, global supply will remain structurally dominated by China, with secondary contributions from the US, Australia and Myanmar.

Over the coming years, rare earth market dynamics are expected to shift from just mining to processing, refining and magnet manufacturing facilities. While China is expected to retain its leading position in producing the magnets and components, Western and ASEAN countries are starting to build their own local supply chains—a move that will keep the market tight and highly competitive for years to come.