The results of the February 2026 quarterly adjustment for the MSCI China Index will take effect after the market close on February 27, 2026. As a key benchmark tracked by global passive funds, newly included stocks are expected to see inflows of passive capital around the effective date of February 27.

On February 11, MSCI, the international index compiler, announced the results of its February 2026 quarterly index review, including updates to the widely followed MSCI China and MSCI China Small Cap Indices. All changes will officially take effect after the market close on February 27, 2026.

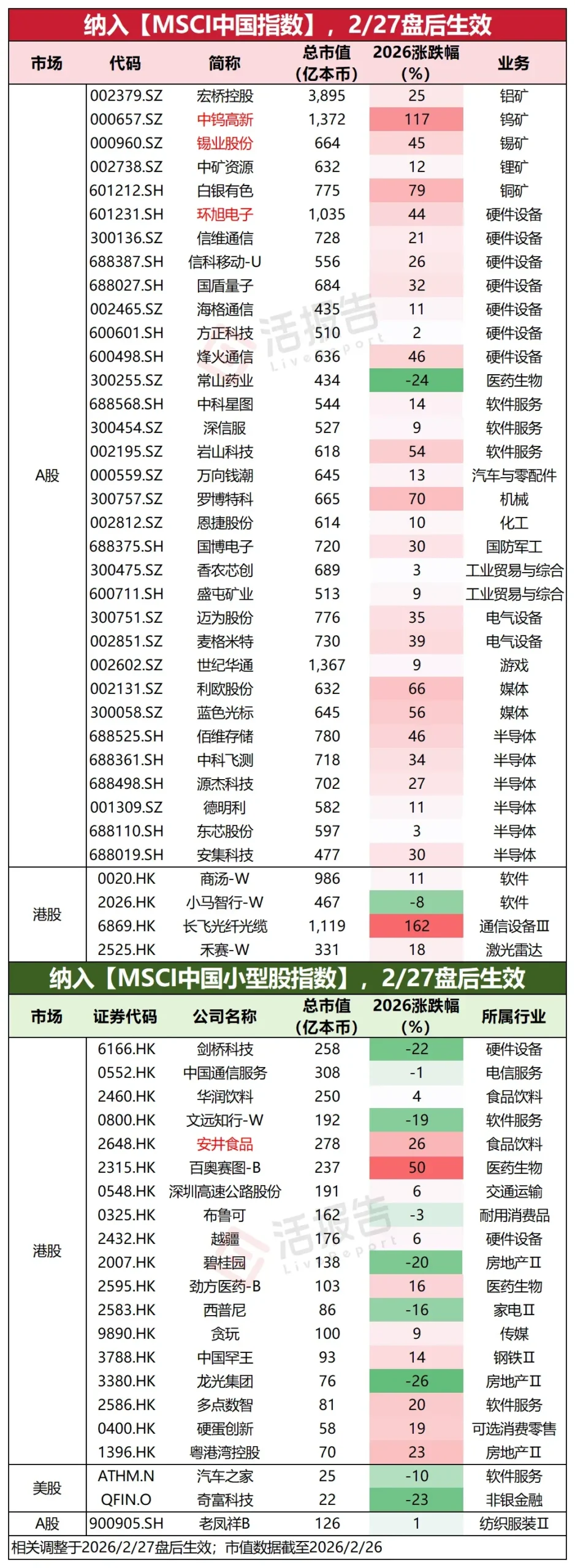

According to the full list published by MSCI, this adjustment adds 37 new constituents to the MSCI China Index, including four Hong Kong-listed stocks and 33 A-shares.

Specifically,$SENSETIME-W (00020.HK)$、$PONY-W (02026.HK)$、$YOFC (06869.HK)$、$HESAI-W (02525.HK)$Four Hong Kong-listed stocks have been included in the MSCI China Index. As of this writing, these four stocks showed strong performance in early trading on February 27. This adjustment clearly reflects international capital’s recognition of China’s strategic investments and growth in emerging technology sectors such as artificial intelligence, autonomous driving supply chains, and new infrastructure.

Specifically,$SENSETIME-W (00020.HK)$、$PONY-W (02026.HK)$、$YOFC (06869.HK)$、$HESAI-W (02525.HK)$Four Hong Kong-listed stocks have been included in the MSCI China Index. As of this writing, these four stocks showed strong performance in early trading on February 27. This adjustment clearly reflects international capital’s recognition of China’s strategic investments and growth in emerging technology sectors such as artificial intelligence, autonomous driving supply chains, and new infrastructure.

Regarding removals, this adjustment excludes 16 stocks, involving some traditional real estate, financial, and automotive sectors, including $ZHEJIANGEXPRESS (00576.HK)$ 、 $CHINACOMSERVICE (00552.HK)$、 $CHINA VANKE (02202.HK)$ and other Hong Kong-listed stocks.

After the adjustment, the number of constituents in the MSCI China Index increased from 560 to 581, including 408 A-shares (weight: 14.7%), 164 Hong Kong-listed stocks (weight: 81.3%), seven U.S.-listed Chinese stocks (weight: 3.9%), and two B-shares (weight: 0.1%). Hong Kong-listed stocks continue to hold an absolute weight advantage.

In addition,$CIG (06166.HK)$、$CR BEVERAGE (02460.HK)$、$WERIDE-W (00800.HK)$、$ANJOY FOOD (02648.HK)$、$BLOKS (00325.HK)$、$DOBOT (02432.HK)$、$BIOCYTOGEN-B (02315.HK)$、$HIPINE (02583.HK)$、$TANWAN (09890.HK)$、$GENFLEET-B (02595.HK)$A total of 18 Hong Kong stocks, including the aforementioned, have been included in the MSCI China Small Cap Index.

In terms of the sector distribution of companies included in the MSCI China Index, relevant firms are mainly concentrated in hardware equipment, semiconductors, software services, and non-ferrous metals. Stocks in these sectors have shown relatively strong performance over the past year.

MSCI stated that this quarterly adjustment primarily reflects changes in market dynamics and further enhances the market representation and liquidity of the MSCI China Index. The adjusted stocks span multiple industries, indicating the diversification of the MSCI China Index.

UBS Group is optimistic, predicting that the MSCI China Index could rise by 20% by 2026.

Notably, as rising inflation expectations translate into better profitability, UBS Group recently reiterated its bullish stance on the Chinese stock market in 2026, with the MSCI China Index expected to increase by 20%.

According to a UBS Group survey, an increasing number of Chinese companies plan to raise prices this year due to rising input costs, while signs of improvement in overcapacity are emerging. Strategists noted that a reflationary environment will drive valuation reassessment and stronger earnings per share growth, potentially boosting the MSCI China Index by 20%. In the context of price increases, “given the market’s low expectations for reflation and the underweight positioning of inflation-related stocks (such as consumer stocks), the potential stock price reaction is more likely to be upward.”

Moreover, driven by advancements in artificial intelligence and favorable policy measures, other international investment banks have adopted a positive outlook on the Chinese market. In early January, Goldman Sachs projected that the MSCI China Index would reach 100 points by the end of 2026, representing a 20% increase from its level at the end of 2025. The CSI 300 Index is also expected to rise by 12% in 2026, reaching 5,200 points. The bank’s strategists stated that equity returns in China in 2026 will primarily be driven by improved corporate earnings. Supported by AI development, companies expanding overseas, and anti-internal competition policies, earnings growth is expected to accelerate from 4% in 2025 to approximately 14% between 2026 and 2027.

AI Portfolio Strategist goes live!Gain comprehensive insights into your holdings, fully grasp opportunities and risks with a single click.

AI Portfolio Strategist goes live!Gain comprehensive insights into your holdings, fully grasp opportunities and risks with a single click.

Compiled from reports by Huo Report and Zhitong Finance.

Editor/Rice