Maybe you’ve noticed: stocks have been red-hot over the last few months.

Even accounting for some recent volatility in hot trades like memory stocks, since the March 30 low, the S&P 500 is up 18%. Soaring semiconductor stocks have led the way, with the iShares Semiconductor ETF rising as much as 106% from its recent trough.

But the run-up has triggered a concerning signal, says Philip Straehl, the chief investment officer for Morningstar Wealth.

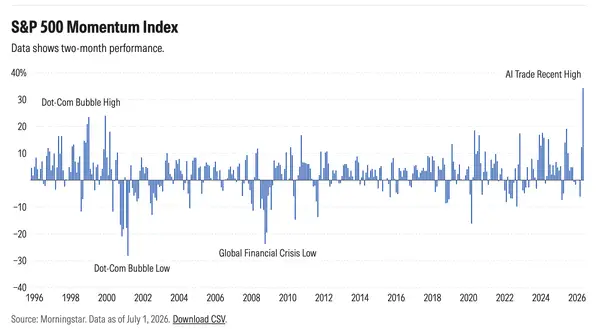

In April and May, the S&P 500 Momentum Index had its best two-month period going back to at least 1995, returning 34%. That well surpassed highs reached around the dot-com peak in 1999 and 2000. The index holds the 100 stocks in the S&P 500 that have performed best in recent months.

Morningstar

“I think it’s one signal that there might be excessive optimism in the market today, and so I think it leaves us with a cautious outlook for markets from this point on,” Straehl told Business Insider on Tuesday.

Sentiment measures can be good contrarian indicators. The S&P 500 Momentum Index, in particular, can serve as a proxy for market FOMO. When investors are overly exuberant, it can signal that stock prices are becoming detached from fundamentals, setting them up for a decline. As the old Warren Buffett adage goes: “Be fearful when others are greedy.”

The recent rapid decline in semiconductor stocks since the beginning of June might be a good illustration of this point.

Straehl emphasized that the momentum metric is just one of many in a “mosaic” of gauges he’s monitoring, and many other indicators are trending in a similar direction as the momentum index.

He said his market outlook can be broken down into three supporting pillars: investor sentiment, market valuations, and capital supply.

Within the sentiment pillar, zero-day options activity and leveraged ETF flows also point to heightened exuberance, alongside the momentum index’s price action.

The valuation pillar is also concerning, Straehl said. Measures like the Shiller PE ratio, price-to-book, price-to-sales, and the equity risk premium look “extreme,” he said.

On the capital supply front, however, while issuance of equity and debt are high — see: the SpaceX IPO, Google’s $85 billion secondary equity offering, and soaring M&A activity — Straehl said they are not at extremes yet. Heightened equity and debt issuance can mean firms are capitalizing on investor bullishness and elevated valuations.

“The overall reward for risk is not really good,” Straehl said of his outlook for the broader market. “Our view is that you have to be more selective in today’s environment.”