Markets breathed a sigh of relief on Monday after Iran’s military declared its first wave of attacks against Israel complete, helping Brent crude retreat from above $98 to below $95. Yet the pullback in oil may be telling only part of the story. While investors rushed back into risk assets, crude prices remain firmly above $90, suggesting traders are still demanding a substantial geopolitical risk premium.

The improvement in sentiment followed comments from Iran indicating that its latest military operation had concluded, while also warning that attacks could resume if Israel continued military actions in Lebanon. The absence of immediate escalation helped stabilize financial markets after a volatile start to the session. Commodity-linked currencies such as New Zealand Dollar and Australian Dollar outperformed, while safe havens including Dollar gave back some recent gains.

However, the broader geopolitical picture remains fragile. There has been no formal response from Israel, leaving open the possibility of further retaliation. Moreover, Iran’s description of its operation as the “first wave” was notable. The wording appeared designed to signal that military capabilities remain intact and that additional strikes remain an option if circumstances change. Equally important, the current ceasefire framework is highly conditional rather than comprehensive, linking future restraint directly to developments in Lebanon.

For oil markets, these unresolved risks remain significant. If traders genuinely believed a durable de-escalation was underway, Brent would likely have surrendered a much larger portion of its recent gains. Instead, prices remain elevated above $90, indicating continued concerns over supply disruptions and regional instability. The retreat from $98 therefore looks more consistent with short-term profit taking than a wholesale removal of geopolitical risk premium. After all, the US and Iran are no closer to a peace deal than President Donald Trump claimed.

The implications extend well beyond energy markets. Elevated oil prices increase the likelihood that inflation pressures will continue filtering through the global economy over coming months. That dynamic has become increasingly important following last week’s stronger-than-expected US nonfarm payrolls report, which reinforced the view that Fed has room to focus on inflation rather than labor market weakness.

As a result, investors are paying close attention to Wednesday’s US CPI report. A further acceleration in inflation, particularly in the core measure, would strengthen expectations that Fed may need to tighten policy again later this year. Such an outcome could push Treasury yields and Dollar higher while renewing pressure on risk assets.

For now, market sentiment has stabilized. Yet the recovery rests on fragile foundations. Geopolitical tensions remain unresolved, oil prices remain elevated, and inflation risks continue to build. If US CPI surprises to the upside, the market’s relief rally may prove as temporary as the latest ceasefire arrangement.

Eurozone Sentix Confidence Extends Recovery, but Inflation Concerns Stay Elevated

Eurozone investor confidence improved for a second consecutive month in June as concerns over a sharp economic slowdown continued to fade. Yet while global growth prospects have brightened, higher energy prices are keeping inflation pressures elevated, reinforcing expectations that ECB will maintain a vigilant stance at this week’s meeting. Read More.

Gold’s Downside Acceleration Points to Crucial $4,000 Battle Zone

Gold’s selloff has accelerated as strong US economic data and rising oil-driven inflation risks push investors toward Dollar and Treasury markets. The next major battleground lies near $4,000, a level that could determine whether Gold remains in a bull market or enters a more significant downturn. Read More.

US CPI Leads High-Stakes Week as Fed Hike Expectations Build

Markets enter the week with one question dominating the outlook: has the oil shock become large enough to force central banks into a more aggressive stance? US CPI, ECB forecasts and the Bank of Canada decision could provide the answer, with major implications for rates, currencies and risk assets. Read More.

Japan Growth Downgraded to 1.8% as Capital Spending Weakens

Japan’s economy grew more slowly than first reported in the first quarter as business investment unexpectedly contracted. While consumer spending, housing activity and exports were revised higher, the downgrade in capital expenditure suggests corporate confidence may not be keeping pace with broader economic recovery. The figures offer a mixed signal for markets assessing Japan’s growth outlook and Bank of Japan normalization prospects. Read More.

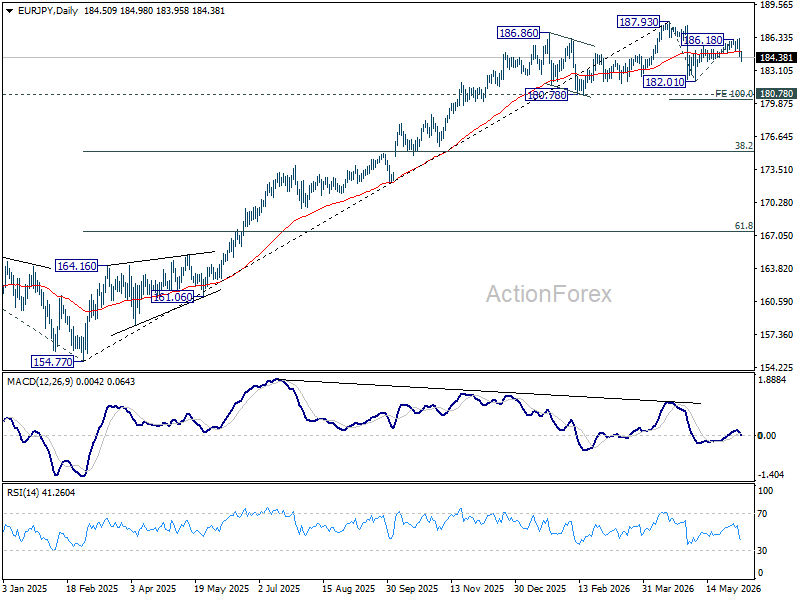

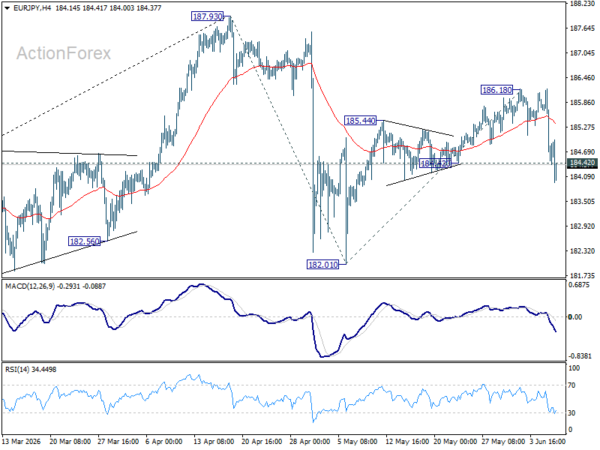

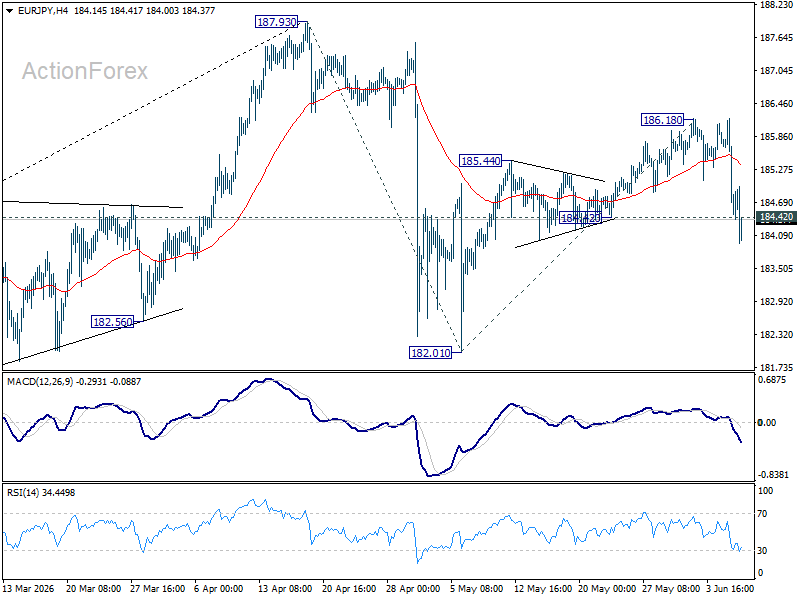

EUR/JPY Daily Outlook

EUR/JPY’s break of 184.42 support suggests that rebound from 182.01 has completed with three waves up to 186.18. Fall from there is seen as the third leg of the pattern from 187.93. Intraday bias is back on the downside for 182.01 support next. For now, risk will stay on the downside as long as 186.18 holds, in case of recovery.

In the bigger picture, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.95) will argue that it’s already in a medium term down trend to 175.41 resistance turned support and below.