The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, highlighting concerns about global economic recovery. In such an environment, identifying stocks that may be trading below their estimated value can provide opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

Vulcan Two Group (AIM:VUL) |

£2.65 |

£5.25 |

49.6% |

|

Tristel (AIM:TSTL) |

£3.825 |

£7.59 |

49.6% |

|

RHI Magnesita (LSE:RHIM) |

£29.70 |

£55.89 |

46.9% |

|

Playtech (LSE:PTEC) |

£3.458 |

£6.57 |

47.3% |

|

Mitie Group (LSE:MTO) |

£1.732 |

£3.40 |

49% |

|

M&G (LSE:MNG) |

£3.153 |

£6.03 |

47.7% |

|

Man Group (LSE:EMG) |

£2.92 |

£5.82 |

49.8% |

|

Hostelworld Group (LSE:HSW) |

£1.09 |

£2.17 |

49.7% |

|

Fevertree Drinks (AIM:FEVR) |

£7.515 |

£14.94 |

49.7% |

|

BTG Consulting (AIM:BTG) |

£1.235 |

£2.44 |

49.3% |

Let’s explore several standout options from the results in the screener.

Overview: Dr. Martens plc is involved in the design, development, procurement, marketing, sale, and distribution of footwear with a market cap of approximately £696.75 million.

Operations: The company’s revenue primarily comes from its footwear segment, which generated £764.90 million.

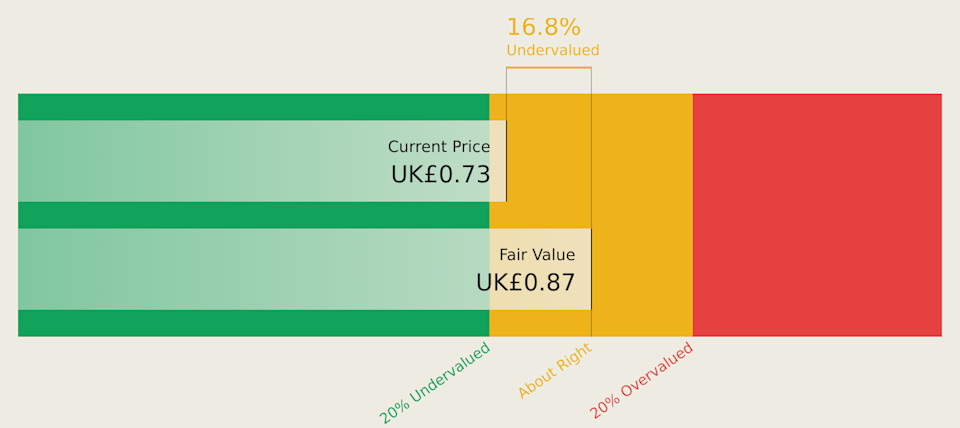

Estimated Discount To Fair Value: 16.8%

Dr. Martens is trading 16.8% below its estimated fair value and slightly undervalued based on discounted cash flow, with a trading price of £0.73 against a future cash flow value of £0.87. Despite slower revenue growth forecasts at 4.5% annually, earnings are expected to grow significantly at 29.5% per year, outpacing the UK market’s average growth rate of 11.5%. Recent earnings showed substantial improvement in net income from £4.5 million to £23.8 million year-over-year, though dividend coverage remains weak at 3.5%.

Overview: Man Group Limited is a publicly owned investment manager with a market cap of £3.26 billion, focusing on providing a range of investment strategies and solutions.

Operations: The company’s revenue from its Investment Management Business segment amounts to $1.41 billion.

Estimated Discount To Fair Value: 49.8%

Man Group is trading at £2.92, significantly below its estimated future cash flow value of £5.82, indicating substantial undervaluation based on discounted cash flow analysis. While the dividend yield of 4.37% lacks robust coverage by earnings or free cash flows, earnings are projected to grow significantly at 26.54% annually, surpassing the UK market’s average growth rate of 11.5%. Recent expansion efforts in Abu Dhabi highlight strategic global positioning and potential for increased investor engagement in the Middle East region.

Nice post. I learn something totally new and challenging on websites