- Elusive US-Iran deal keeps inflation fears alive amid resilient risk appetite.

- US jobs data to take spotlight as hawkish Fed soundbites grow.

- Eurozone flash CPI to be eyed too as ECB preps for June rate hike.

- But will the yen steal the show as it re-enters 160 zone?

US-Iran Drama Keeps Traders Gripped

It’s been seven weeks since the US and Iran agreed to a ceasefire and engage in talks aimed at negotiating a permanent deal that not just ends the hostilities and reopens the Hormuz Strait but also resolves the long-standing nuclear issue.

Under any circumstances, reaching such a deal would be quite a feat. Hence, it shouldn’t come as too much of a surprise that negotiations are ongoing and there are still significant differences that need to be bridged. However, investors were led to believe that a deal was imminent.

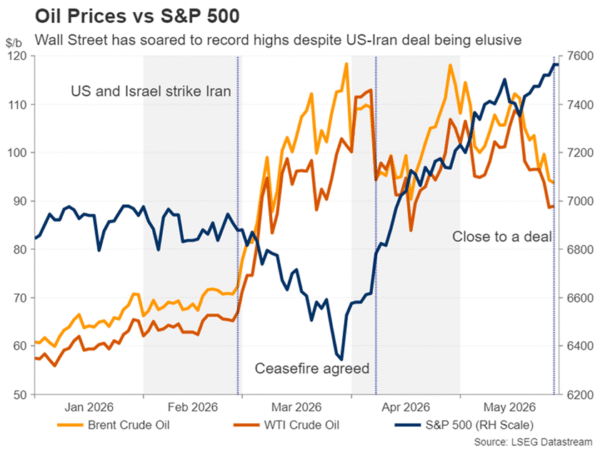

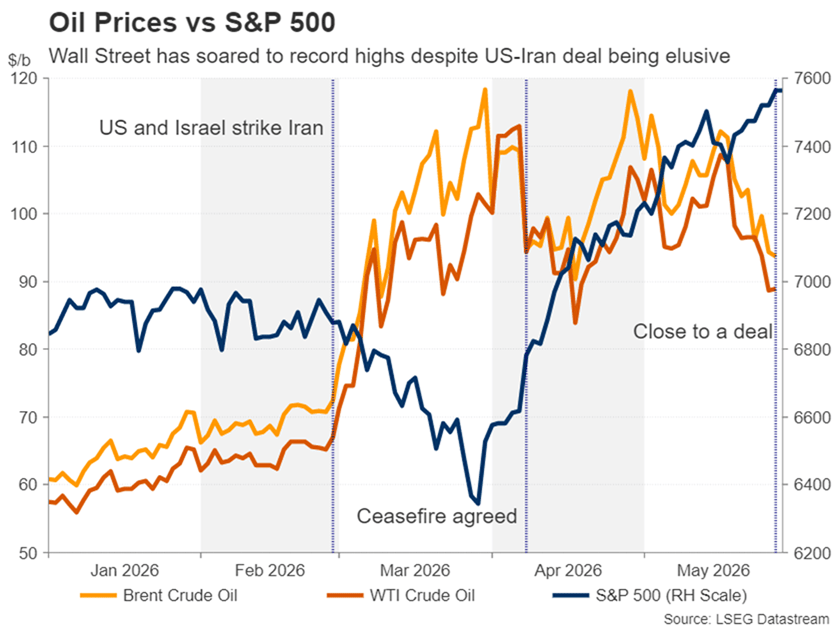

That hasn’t turned out to be the case, and instead, the barrage of missile and drone attacks has switched to a barrage of headlines about the diplomatic push. What’s most unusual, though, is that aside from oil prices, market volatility has been steadily declining during this time, even as traders grapple with making sense of Trump’s daily commentary and conflicting reports from various Iranian sources about where the talks stand.

Yet, the most critical issue for the global economy – the Strait of Hormuz – remains at a stalemate, therefore, there’s been no downgrading of the severity of the ensuing energy crisis. It’s somewhat unnerving that markets even seem to enjoy the US-Iran drama. Surely, a Netflix limited series where the finale has already been recorded would have been the preferable scenario to what seems to be a never-ending soap opera.

Are investors being fooled into believing that a deal is around the corner? Is there a risk of a reality check? Probably, but there would have to be a very big escalation for markets to sit up and take notice, as the recent days’ skirmishes have barely lifted an eyelid, at least in equity markets, where the AI boom has driven Wall Street to new record highs. Perhaps that would change if the incoming economic data continues to bolster rate hike expectations for the Fed and other major central banks.

Will NFP and ISM PMIs Spark Much Reaction?

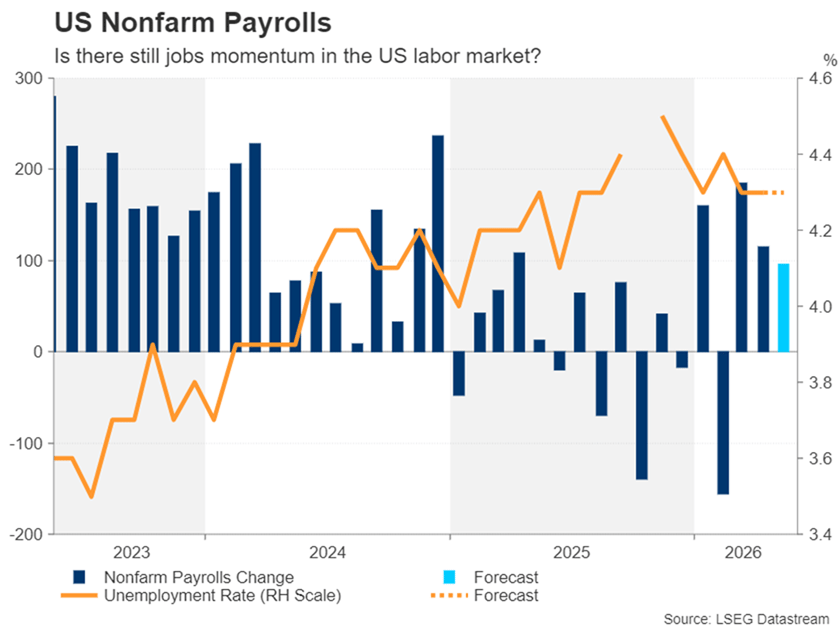

Certainly, next Friday’s nonfarm payrolls report has the capacity to shift market expectations, as a softish labour market is the Fed’s only excuse to still keep the option of a rate cut on the table. Recent NFP data have been mixed, as either contrasting jobless rate readings or revisions to prior figures have offset the initial reaction to the headline payrolls prints.

For May, analysts expect jobs gains of 96k versus 115k in April. The unemployment rate is forecast to have stayed unchanged at 4.3%, while average hourly earnings growth likely accelerated slightly on a month-on-month basis to 0.3%.

Ahead of the jobs report, the ISM manufacturing and services PMIs will be watched closely on Monday and Wednesday, respectively. Any uptick in the price indices could stoke inflation fears. But of course, the impact would be limited if the employment indices moved in the opposite direction.

Other US releases include the JOLTS job openings for April on Tuesday, factory orders and the ADP employment report on Wednesday, and the Challenger Layoffs for May on Thursday.

A broadly strong set of numbers would weaken the case for the Fed to maintain its easing bias at its June 16-17 gathering, likely creating a dilemma for new chair Kevin Warsh’s first meeting.

For the dollar, however, investors will continue to balance geopolitical risks with rate hike bets, which have moderated slightly on the hope that a US-Iran agreement is near.

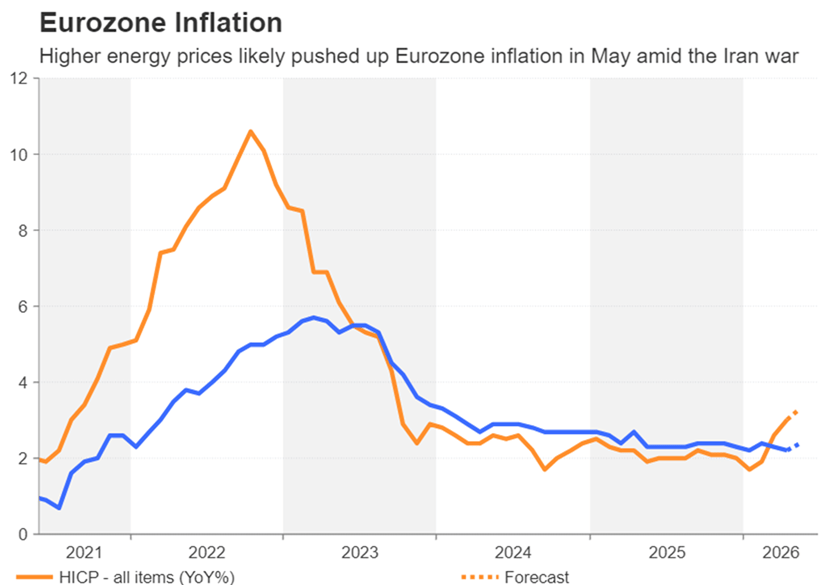

Euro Awaits CPI Data Ahead of Expected Hike

In the euro area, traders are already bracing for the first rate hike since September 2023. The signals from ECB policymakers have been getting louder and so the focus is now turning to the pace of increases thereafter rather than the June decision itself. Tuesday’s flash CPI estimates for May will be the last major update from the bloc before the meeting and therefore vital to the decision.

Headline CPI jumped to 3.0% y/y in April – the highest, coincidentally, since September 2023. The core measure that excludes food, energy, tobacco and alcohol eased slightly to 2.2% y/y. If core CPI remains near 2.0%, the European Central Bank will likely be hesitant about flagging a steep rate-hike path, potentially weighing on the euro.

However, it’s also possible the euro could gain from softer-than-expected inflation figures, as a less aggressive ECB would reduce the risk of stagflation and improve the Eurozone outlook somewhat.

In fact, the euro may be more likely to come under pressure from much hotter-than-forecast inflation readings or a major flareup in the Middle East that fuel concerns about a recession.

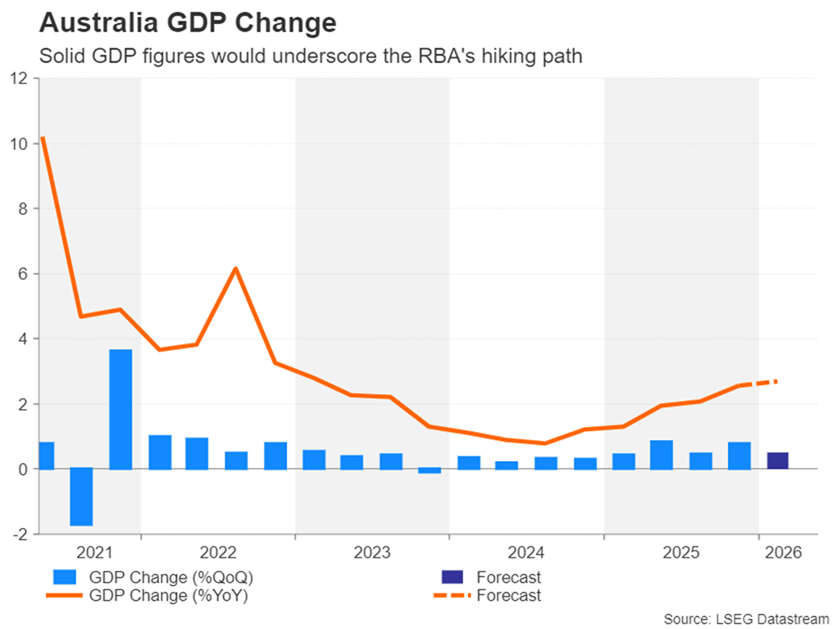

Aussie’s and Loonie’s Paths Diverge

The energy crisis has had unexpected effects on two key commodity currencies. Oil-exporting Canada has seen the loonie depreciate marginally against the US dollar, while resources-rich Australia has experienced unusual resilience in the risk-sensitive aussie.

Canada’s faltering jobs market and relatively lower inflation as opposed to Australia’s more robust economy and 4%+ inflation have something to do with that. Although Australia is heavily dependent on fuel imports for transportation, it doesn’t need as much for electricity generation, while its exports of resources and minerals have been benefiting from the AI boom. The Canadian economy, on the other hand, has the ongoing trade dispute with Trump and the renegotiation of USMCA hanging over its head, countering some of the effects of higher oil prices.

More to the point, the Reserve Bank of Australia is already on a rate-hiking path, but the Bank of Canada has yet to embark on one. Investors don’t anticipate the BoC to begin raising interest rates before October. If Friday’s employment numbers for May disappoint, the timing could be pushed further back into the year.

The RBA, however, is expected to resume rate hikes in August following its well-telegraphed pause in June. First quarter GDP estimates due on Wednesday are unlikely to greatly change the rate outlook but a strong performance right before the start of the Iran war would nevertheless give the RBA less reason to be cautious.

Aussie traders will also be keeping an eye out on May manufacturing PMIs for China, with both the official and S&P Global versions due on Monday.

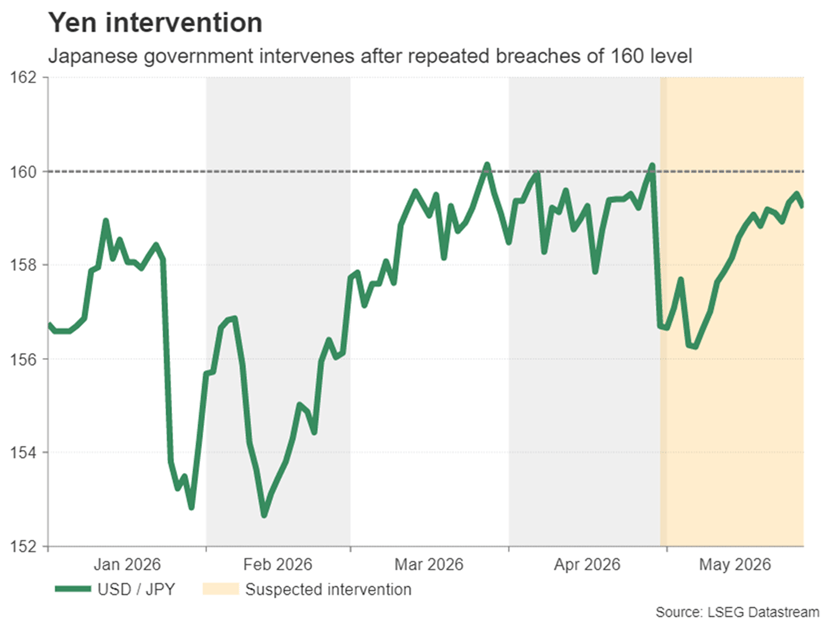

Is Fresh Yen Intervention on the Cards?

In Japan, government energy subsidies have helped to bring down inflation during the Middle East conflict, although this hasn’t stopped the Bank of Japan from acknowledging that underlying price pressures are growing, not just from the energy shock, but also from higher wage growth.

Cash earnings data out on Friday will offer an update on the BoJ’s progress in achieving sustained wage growth. Household spending data will also be watched the same day.

But it’s questionable whether any upside surprises will be able to boost the yen. The recent more hawkish rhetoric from the BoJ hasn’t been able to prevent the yen from returning to the 160-intervention zone. BoJ policymakers continue to play it safe with their forward guidance, refraining from committing to multiple rate hikes, while the ongoing geopolitical risks have exposed Japan’s overreliance on the Middle East for its energy needs.

With the dollar back above 159 yen this week, the Japanese government may be compelled to intervene again in the coming days if the 160 level is breached.