How long does a company need to raise its yearly dividend payment until you’re convinced its dividend growth is practically bulletproof? Twenty years? Maybe 30? Would 70 years do the trick?

As outrageous as that sounds, a handful of companies have actually done it (and are still doing so). And one of these few names is a top prospect right now following the stock’s 14% pullback from its February peak. That’s Procter & Gamble (PG 0.72%).

Here’s a closer look at why it may belong in your portfolio, particularly right now.

Image source: Getty Images.

Procter & Gamble is more than you might realize

You’ve almost certainly heard of the company, but are you aware of just how wide and entrenched its product portfolio is?

Procter & Gamble is the name behind brands like Tide laundry detergent, Gillette razors, Dawn dishwashing liquid, Crest toothpaste, Pampers diapers, and Bounty paper towels, among others. Most of its products are leaders of their respective categories, if only because they’ve been around forever and have had plenty of time to become the preferred, out-of-habit purchase. That’s also why the company’s the biggest name in the consumer goods business, driving sales of $84.3 billion last fiscal year and turning $16.1 billion of that into net income.

Today’s Change

(-0.72%) $-1.03

Current Price

$141.68

Key Data Points

Market Cap

$330B

Day’s Range

$141.20 – $143.72

52wk Range

$137.62 – $170.99

Volume

302K

Avg Vol

10M

Gross Margin

50.88%

Dividend Yield

3.01%

Oh, its net growth was modest, to be clear, as is usually the case for this giant, multifaceted company. There’s only so much progress to be made in the well-saturated consumer staples business.

Investors don’t own a stake in P&G first and foremost for growth, however. While they’ll certainly get some if they hang on to it long enough, this stock’s dividend pedigree is its chief selling feature.

As noted, P&G’s per-share payout has now been increased for 70 consecutive years and is still going. And by more than a little. The annual increase announced in April was a 3% improvement on the prior payout, capping off a 10-year streak where the dividend payment grew at an average yearly rate of 4.8%.

But there’s a much deeper, philosophical argument for buying and holding a position in Procter here.

Built tough

This isn’t to suggest the company can simply breeze through any challenges. Things get tough for it, too. For instance, since inflation became regularly unwieldy beginning in 2022, more than once has the company reported disappointing quarterly revenue resulting from price hikes it had little choice but to impose.

It responded as it should, with everything from job cuts to more aggressive innovation. But some of its challenges are largely out of its control. High oil prices, for example, could shave as much as $1 billion off this year’s bottom line.

In the grand scheme of things, though, Procter & Gamble enjoys an arguably unfair advantage over its rivals. That’s its sheer size.

This size-based advantage manifests in several ways. Perhaps the most important one, however, is that P&G is simply able to spend more on marketing and advertising than rivals like Clorox and Colgate-Palmolive.

For perspective, Procter spent $9.2 billion on advertising last fiscal year, versus Colgate-Palmolive’s $2.7 billion and Clorox’s typical $800 million. In a business where the repetition of a marketing message matters, Procter & Gamble’s competitors just can’t afford to keep up.

Procter’s size also helps in another often-overlooked way. That’s the fact that its product lineup is so important to retailers. Not only are P&G’s quality products relatively easy to sell to consumers, but retailers know Procter & Gamble will promote its own goods, driving foot traffic to stores where consumers are apt to buy something else while there. This gives the company significant leverage when negotiating wholesale pricing or placement on a store’s shelves.

In other words, Procter & Gamble’s got true staying power.

Not right for everyone, but a perfect option for some

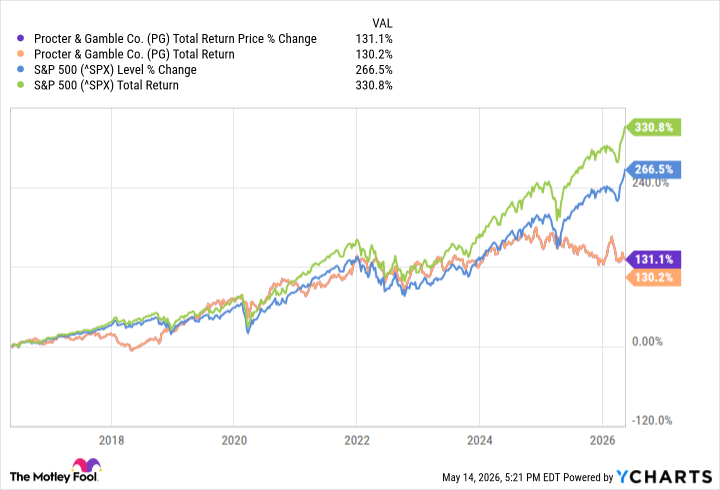

Again, it’s not a growth stock by any means. P&G shares have underperformed the S&P 500 (^GSPC 1.24%) for the better part of the past 10 years, in fact, with or without reinvested dividends.

PG Total Return Price data by YCharts

Still, Procter’s done its job as an income-producing holding. It’s dished out in the order of $14.00 worth of growing per-share dividends during this stretch, maintaining a respectable yield of between 2.3% and 3.2% for most of this time.

Perhaps more noteworthy right now — under the dark clouds of what seemingly could turn into more pronounced economic weakness — notice on the chart that PG shares tend to perform better when the overall market doesn’t. If, for some reason, investors start worrying about AI stocks’ wild valuations and suddenly seek safety, a well-proven Procter & Gamble is one of the first names they’ll likely turn to.

Bottom line? Don’t make it complicated. It’s not a sexy stock to own. However, P&G is certainly a reliable one — especially for income-seeking investors. You can plug into it while its forward-looking dividend yield is a solid 3%.