The market narrative is shifting from chasing the risk rally to waiting for confirmation. After a sustained push higher driven by optimism around US-Iran negotiations, investors are becoming more cautious ahead of a critical weekend. The rally remains intact, but the willingness to extend positions without new information is fading.

US equities pushed to fresh record highs overnight, with the S&P 500 and NASDAQ extending gains overnight. But the lack of follow-through elsewhere suggests that conviction is fading temporarily. This hesitation is most visible in Asia. Japan’s Nikkei has pulled back from its own record highs, trimming gains as traders lock in profits ahead of the weekend. Oil markets are sending a similar signal. Prices are holding in a tight range just below the $100 mark.

That caution is justified given evolving expectations for the US-Iran negotiations. Reports indicate that both the US and Iran are scaling back ambitions from a comprehensive agreement toward a more achievable interim framework. The focus is shifting toward a temporary memorandum that would prevent renewed conflict rather than deliver a full resolution. Back-channel diplomacy appears to be playing a key role. Lower-level discussions have reportedly made progress in narrowing differences, raising the possibility of an agreement in principle. However, significant technical details are likely to be deferred.

US President Donald Trump has maintained an upbeat tone, saying the US is “very close to making a deal with Iran” and even hinting he could travel to Islamabad for a signing. Such rhetoric is supporting underlying optimism, but markets are turning cautious about taking it at face value without concrete outcomes.

At the same time, geopolitical efforts are expanding beyond the core US-Iran channel. The UK and France are set to chair a meeting of around 40 countries to coordinate efforts to keep the Strait of Hormuz open once hostilities ease. The proposed mission could involve intelligence sharing, mine-clearing operations, and military escorts to secure shipping lanes. Even if tensions ease, the need for a transitional security framework suggests that normalization will not be immediate.

In the currency markets, Yen has overtaken Dollar’s place as the worst performer of the week so far, while Sterling is the third. Aussie continues to lead at the top, followed by Loonie, and then Kiwi. Euro and Swiss Franc are positioning in the middle.

In Asia, Nikkei fell -1.13%. Hong Kong HSI is down -1.15%. China Shanghai SSE is down -0.06%. Singapore Strait Times is down -0.27%. Japan 10-year JGB yield rose 0.015 to 2.421. Overnight, DOW rose 0.24%. S&P 500 rose 0.26%. NASDAQ rose 0.36%. 10-year yield rose 0.027 to 4.309.

NASDAQ Hits Record High as AI Trade Revives, Eyes 26k+ if Oil Normalizes to $80

NASDAQ has surged to record highs as the AI trade revives The next move toward 26k depends on whether oil prices fall back toward $80 and ease inflation pressure. Read more.

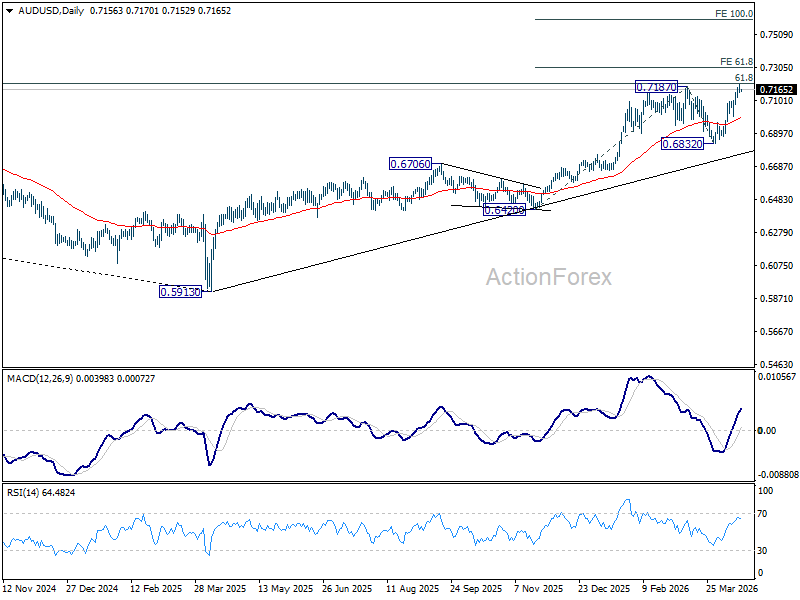

AUD/USD Daily Report

Daily Pivots: (S1) 0.7144; (P) 0.7171; (R1) 0.7190; More…

Intraday bias in AUD/USD is turned neutral with current retreat and some consolidations would be seen below 0.7197 temporary top first. Further rally is expected as long as 0.7000 support holds. Above 0.7917 will resume larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. Decisive break there could prompt upside acceleration to 100% projection at 0.7599.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.